After a brief rebound, asset and equipment finance faces geopolitical shocks, shifting credit appetites and rising demand for speed and flexibility

Sometimes when things are looking up, a dip in the road to recovery emerges to mess everything up again.

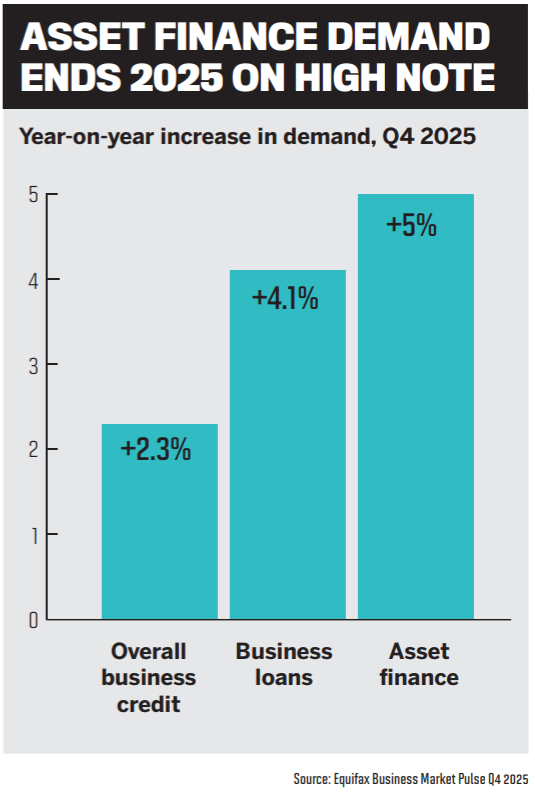

Take the current state of asset and equipment (A&E) finance. Following a rather drab 2025 potholed by high interest rates, weak consumer confidence and a slowdown in the construction sector, a turning point was up ahead. As a new year emerged on the horizon, volumes were trending higher and brokers were reporting a resurgence in enquiries.

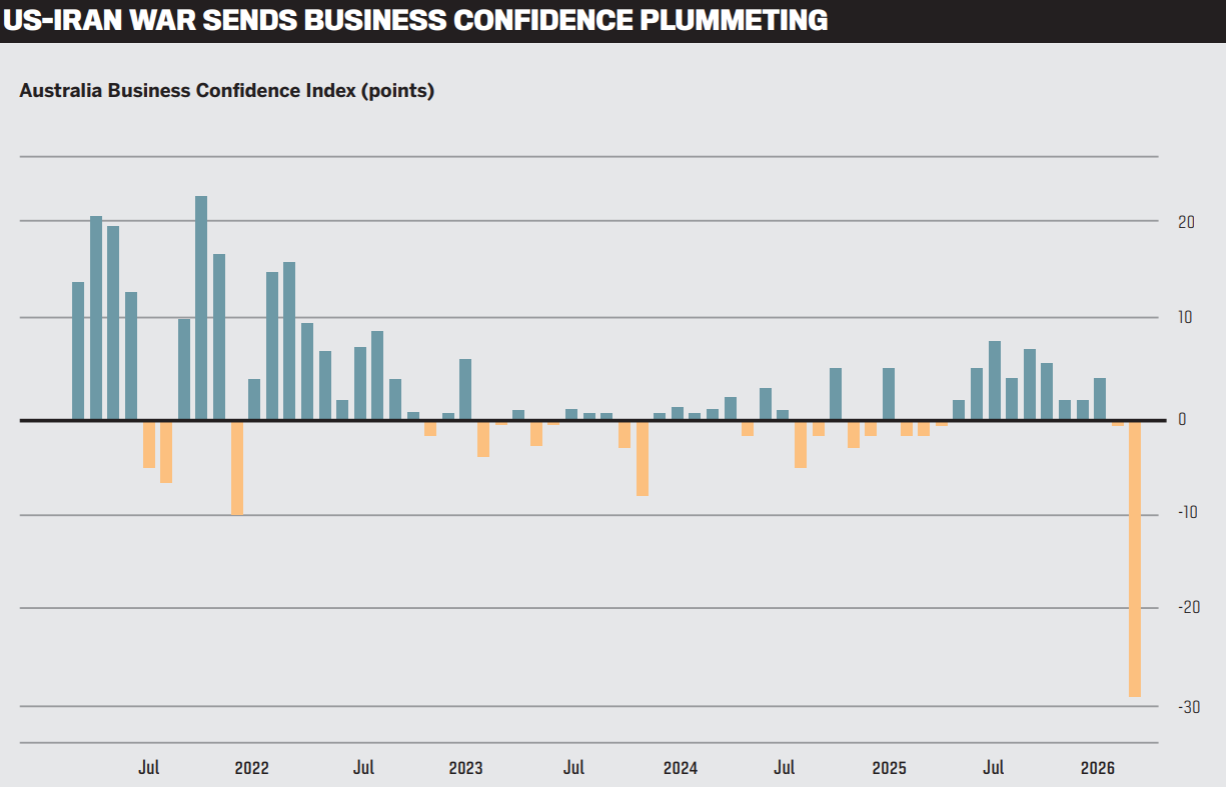

Then along came the little matter of the US‑Iran war, and A&E finance is now facing the fact that recovery was merely fleeting after all.

If this were the stock market, an analyst might call it a dead cat bounce – a rather ugly term for a false recovery in a downwardly trending market.

At the turn of the year, Blake Buchanan (pictured, right), general manager of mortgage aggregator SFG, witnessed a momentary uptick in demand from SMEs that had delayed capital expenditure decisions in 2025. But “there’s now more caution in the market again due to international affairs”, he says. “Businesses considering reinvestment in productivity and efficiency, which is a strong leading indicator for A&E demand, will pause and reassess. Prior to this it has not been a sharp rebound, but a steady, more sustainable recovery was underway.”

Amid these choppy conditions, prominent A&E finance lenders are being strategic with their financing activities.

Resimac, for instance, has kept its settlement volumes on an even kilter. “In the first half of 2026, settlements were broadly in line with the first half of 2025, which was a deliberate decision by us,” Michael Stavroulakis (pictured, left), Resimac’s head of product, asset and equipment and SBLs, tells MPA. “We prioritised higher‑quality deals over volume, and we targeted applications from more resilient sectors.”

In the current lending environment, Stavroulakis stresses the need to be clear on where Resimac stands, policy‑wise. “We price strongly on well‑documented deals, with quality assets and experienced borrowers. We’re not in the market for deals that need aggressive pricing, and while we focus on portfolio performance, we’ll always support brokers and customers where the numbers stack up.”

Stavroulakis adds, “We seek the right business for the risk we take. This means refining our credit appetite for current conditions and keeping customer outcomes front of mind.”

Lenders are also having to accommodate greater demands for flexibility, particularly for SMEs with variable cash flow. Stavroulakis highlights the popularity of balloon payments, while he is also seeing a high volume of refinancing and consolidation requests.

Need for speed

One of the biggest emerging trends – perhaps because no one really knows what tomorrow will bring these days – is the emphasis being placed on deal speed.

In A&E finance, where asset availability and business timing are critical, speed has become “a non‑negotiable”, says Buchanan. This has led to significant investments into automation and credit decisioning among the lenders, he notes, “and we’re seeing strong improvements in turnaround times as a result”.

Resimac, says Stavroulakis, knows how critical speed is for A&E customers, “and that’s why we are investing in improving the broker and customer experience, making the credit assessment more efficient to meet that expectation. We know delays in financing can cost revenue or business contracts and can also reduce productivity. That’s why time to yes matters”.

However, performance isn’t exactly uniform across the market – and brokers are making their voices heard by favouring lenders that can marry speed with consistent settlement follow‑through. “Lenders would do well to continually invest in broker CRM direct lodgements to speed up efficiencies,” says Buchanan.

Alternative lenders have become more prominent in the A&E space for the simple reason that their flexibility, faster credit processes and willingness to look at more complex or outside‑policy deals “make them highly competitive”, Buchanan says.

He notes that the prime space remains the forte of the big banks and traditional lenders, “but their growth is more measured due to tighter policy settings and longer turnaround times”.

Maturing broker relationships

If anything, the volatile nature of the business environment has thrown into contrast the increasingly important role brokers are playing in A&E finance.

“The relationship is becoming more advisory‑led,” says Buchanan. “Clients are no longer just asking ‘can I get finance?’; they’re asking ‘what structure makes the most sense for my business?’ ”

Stavroulakis strikes a similar tone. “Brokers are increasingly acting as an adviser for their business customers,” he says. “Their deep understanding of a client’s business allows them to offer better guidance and seek out lenders who they can work closely with.”

Clear communication and timely feedback from a lender are essential, adds Stavroulakis, as they enable brokers “to present lending options that best suit their clients’ needs, with confidence”.

“In 2026, brokers are expected to have a deeper understanding of industries, not just products. Speed still matters, but so does the ability to guide clients through increasingly complex credit and policy settings,” Buchanan continues. “The brokers who win will be those who can combine responsiveness with genuine commercial insight.”

Brokers are clearly up to the task, as their share of the A&E market goes from strength to strength.

“Broker share in the asset and equipment space is likely to keep increasing,” Stavroulakis predicts. “Customers want choice and speed, and brokers play a critical role in advising on structure and lender choice to land the right solution.”

“Customers want choice and speed, and brokers play a critical role in advising on structure and lender choice to land the right solution” - Michael Stavroulakis, Resimac

While precise figures are not readily available, Buchanan estimates that brokers originate somewhere in the vicinity of 70% of new A&E volumes, and as brokers expand their capabilities, that share is trending higher. “The complexity of deals and the need for lender choice plays strongly into the broker value proposition,” he says.

It helps that diversification in the broking industry is a trend that’s only getting stronger. More brokers – particularly those with a residential lending background – are expanding into A&E finance to diversify their business revenue and deepen client relationships. Concurrently, more A&E brokers are diversifying their businesses into residential lending.

Source: NAB

“Broker diversification is absolutely continuing, and in many ways it’s a positive development,” says Stavroulakis. “It expands market reach and brings more borrowers into the A&E space.” However, he stresses the importance of lenders educating brokers about the unique nuances of A&E finance, including deal structuring and credit expectations.

Diversification “is a positive for the industry overall, but it does raise the bar in terms of capability”, adds Buchanan. “A&E finance requires a different level of credit understanding and commercial awareness. Aggregators and lenders have a role to play in supporting brokers with education, policy clarity and deal structuring guidance to ensure quality advice remains high as participation grows.”

A&E hotspots

A clear trend is emerging in the market: demand is being driven by income‑generating assets, as both Stavroulakis and Buchanan have noted.

Commercial vehicles remain a standout, particularly in the logistics, trade and services sectors where utilisation is high. Electric and hybrid vehicle finance is also growing but from a smaller base, and it’s still influenced by cost and infrastructure considerations.

Demand is strong “where the asset is essential to day‑to‑day operations”, explains Stavroulakis. Construction, maintenance and field equipment has shown early signs of improvement after a softer period, while commercial vehicles remain relatively resilient.

“In 2026, brokers are expected to have a deeper understanding of industries, not just products. Speed still matters, but so does the ability to guide clients through increasingly complex credit and policy settings" - Blake Buchanan, SFG

“Overall, clients are prioritising assets that either directly increase revenue or reduce operating costs,” says Buchanan.

As 2026 progresses, the road is likely to remain bumpy for A&E finance, but the journey will power on regardless.

“Broker and customer experience has become more important than ever,” says Stavroulakis. “Simply providing an approval is no longer enough to stand out. What truly differentiates is clarity and speed in funding. While price remains a factor, it’s not the only consideration.”