Commercial lenders and aggregator FAST gathered at MPA's annual roundtable to talk about the state of the business landscape as it continues to recover from COVID-19

Despite our best intentions and planning, this year’s Commercial Lenders Roundtable was forced online for a second year thanks to the COVID-19 outbreak in Sydney. To use one of the most popular phrases of the last 12 months: we had to adapt.

At this point of the pandemic, everyone knows the drill, and the participants were very accommodating when it came to making changes to the meeting format.

Joining the virtual roundtable this year were Anita Hyde from NAB, John Mohnacheff from Liberty, Cory Bannister from La Trobe Financial, Malcolm Withers from Pepper Money, Danny Adams from Prime Capital, Jonathan Street from Thinktank, Robynne Frost from Suncorp, and Brendan Wright from FAST.

While the format was similar to last year’s, the situation around it was not. Yes, we were back on Zoom, but there was much more confidence and certainty in terms of the commercial lending landscape. This meant that not only were more participants happy to take part, but they could provide a clearer picture of what they had experienced as well as what they expected to come.

Businesses really suffered last year. Hospitality and tourism were particularly impacted as lockdowns meant people could no longer travel or, for much of the year, even go to the pub or out to a restaurant.

Retail was also affected for a period as people were told to only leave their homes for essential items. But the commercial lenders said the retail space was in fact more positive than expected. In March 2020, retail spending had increased 8% from the month before as consumers panic-shopped; it then dropped by 17% in April to 9% lower than it was in the previous April.

In May 2020, retail spending was almost 6% higher than the year before, and by July it was 12% higher year-on-year. Spending has mostly remained above pre-COVID levels ever since.

Although businesses are continuing to be hit hard as parts of the country continue to go into lockdowns, the commercial lenders panel praised the resilience of Australian businesses, saying that they would be key to leading the country through its economic recovery.

This also opens the door to greater opportunities for mortgage brokers. As consumer and business confidence grows, businesses will be looking to expand. Whether they will need more cash flow, larger office spaces, new retail locations or new equipment, mortgage brokers are perfectly suited to helping them find the right solutions.

The panellists in the following discussion go into greater detail about the state of the commercial lending space, as well as about how they are supporting mortgage brokers who want to diversify and what the benefits are of doing so.

Q: What have been some of the standout trends for you in the commercial lending space over the last year?

The past 12 months have been full of ups and downs as Australia has continued to deal with the COVID-19 pandemic. Businesses in particular have been badly affected as lockdowns sporadically force them to close their doors and restrictions limit people’s movements.

Noting that the last year had been interesting, La Trobe Financial’s chief lending officer, Cory Bannister, said the lockdowns had impacted business owners and investors, but subsequent government initiatives had “kept the industry on life support”.

The challenges had placed extra pressure on brokers, he said, who then had to have tough conversations with borrowers to “explain the unexplainable”.

Looking at how each area of the commercial space fared over the last year, Bannister said non-discretionary retail, hospitality and tourism are yet to fully recover, but light industrial and property construction demand have seen a real surge.

Although offices were expected to suffer with the workforce mostly moving to work-from-home arrangements, he pointed to commercial real estate company JLL recently reporting almost $1bn in sales.

“That was higher than what it was pre-COVID, so it’s really interesting; the office market is still a bit of a mystery as to what’s going to happen there,” he said. “The jury is still out on the longer-term future of some of these assets and how they’re going to play out over the next two to three years. We continue to take a cautious approach but are some-what optimistic about where it’s heading.”

Calling it “an extraordinary story of resilience”, Thinktank CEO Jonathan Street agreed that the outlook for the office market was still an unknown, but retail had been much more resilient than people gave it credit for.

With around 90% of Thinktank’s customers being self-employed, customer hardships peaked at 23% and are now back to pre-COVID levels.

“The way in which business has been able to respond to the challenges of the pandemic and the shifting nature of the economy has been quite noteworthy,” Street said.

“It certainly was not expected as we stepped into the pandemic with the uncertainty that was in front of us. But, in particular, industrial property has remained so strong, [and] it continues to go from strength to strength.”

As business owners have needed support and clarity over the last year, brokers have provided it. FAST CEO Brendan Wright said brokers had been an accessible voice of reason and trusted advisers who have helped clients “make sense of it all”.

“Brokers being business owners them-selves can have a relevant, empathetic and differentiating conversation with a client about what it means for them,” Wright said.

“The thing that’s played out most predominantly is the role that brokers have played in helping clients get through their business challenges in the COVID environment.”

Agreeing, NAB’s head of specialised and private, commercial broker, Anita Hyde, said commercial brokers had played a “pivotal role” between the bank and the customer, explaining the nuances of borrowers’ financial positions.

Hyde said the resilience of the Australian business community had been the standout of the last year, and that commercial brokers would remain a good source of support for these businesses as they continued to grow with the opening up of the economy. She added that there were particular areas seeing more demand than others.

“We’re seeing good levels of growth across industries, especially in regional locations that haven’t seen the impacts of COVID as significantly as the CBD locations,” Hyde said. “The opportunity for commercial brokers in the regional areas, we’re really seeing that pick up, especially in equipment finance with regard to the instant asset write-off concessions.

“That demand for managing cash fl ow will only increase; there’s a real opportunity there for brokers to step in and support customers further.”

BROKER QUESTION

Q: How much training would brokers need to write commercial loans?

Brendan Wright, FAST: Working with their aggregator and industry bodies to set up a training plan is important if [brokers are] serious about it for the long run. Depending on how hard they want to go after the opportunity and build the capability in their business, yes, there is training involved and required. As has already been mentioned today, the nature of the products that have been provided by lenders now really help brokers start that journey.

Malcolm Withers, Pepper Money: With the training, it’s about helping the broker realise what are they capable of doing. At Pepper we off er training and commercial workshops on everything from understanding commercial to understanding the differences between commercial and residential, to building your capability for having a conversation. We do sessions on real-life case studies, and even a simple ‘coffee with credit’, having a coffee with our credit managers and talking about how they look at a transaction.

Cory Bannister, La Trobe Financial: I use the analogy that if someone says they want to be able to run 5k whenever they feel the urge, I would say, just do it – you don’t need to train for it. However, if someone said they wanted to run regularly, and maybe even run a marathon, I would strongly suggest they take the time to learn and train on how to do it so as not to get injured or find the experience painful. And this is the same for commercial lending: if you want to write one to two deals per month, you can get by through using non-banks like us; however, if you want to make it your core business, you will benefit from further training.

Jonathan Street, Thinktank: It’s like progressing from high school to university – if you really want to go the whole way, then you choose which path you want to go on. There’s also ‘on-the-deal training’, where our relationship manager approach allows brokers to choose how much assistance they want with a transaction. We adapt to the individual broker and the transaction at hand.

Q: We’re seeing growing numbers of mortgage brokers also writing commercial loans. Why do you think that is?

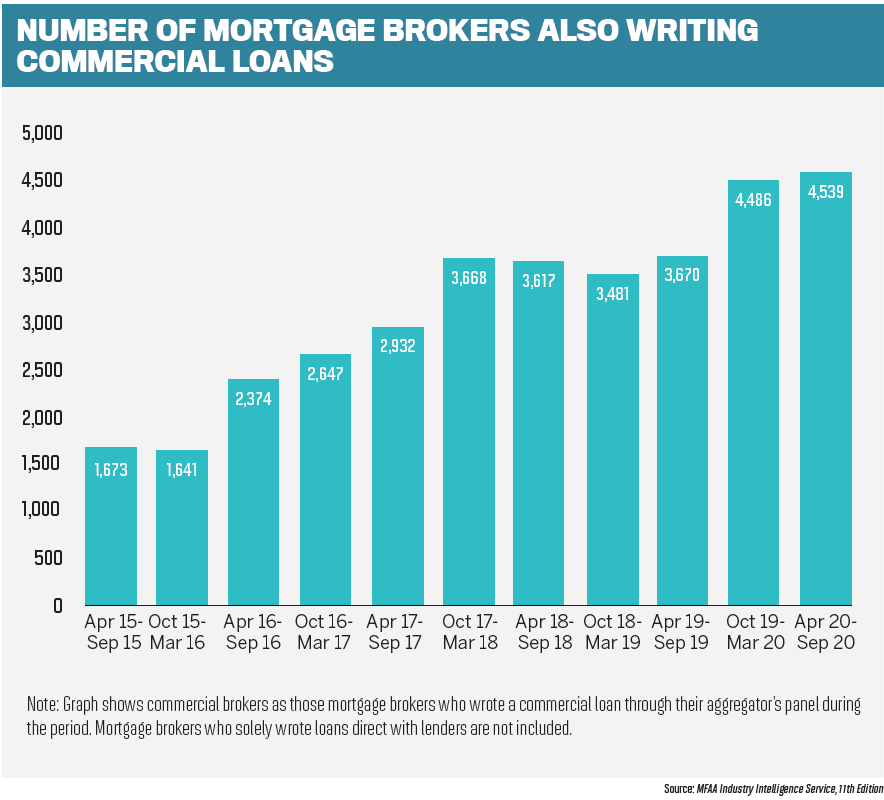

According to the twice-yearly figures from the MFAA, in the six months to September 2020 a record 4,539 mortgage brokers also wrote commercial loans. Starting off the discussion on what might account for this, Prime Capital’s chief operating officer, Danny Adams, called out the competitive residential market, along with the rising market share of brokers in the home loan space.

“There are a lot of brokers out there, so if you want to try to maintain a competitive edge, then you have to diversify,” Adams said, pointing out that the increased competition was also contributing to the growing number of mortgage brokers choosing to expand into commercial loans.

“Speaking from experience at Prime Capital, we came into existence 25 years ago to complement the large banks, with additional commercial lending products and increased options available to commercial borrowers. As more lenders and products become available, it gives borrowers more choice, but it also creates more need for a borrower to speak to a specialist to obtain a commercial loan.”

The growing numbers also suggest that brokers are overcoming the myth of how complicated commercial lending is, said Liberty group sales manager John Mohnacheff.

As more and more mortgage brokers turn to commercial lending, Mohnacheff believes word is spreading that it is not as difficult to do as people think. “In fact, it’s as simple as doing a home loan – or even simpler,” he said.

“Brokers are also realising there’s a lot of help on off er. With support from various lenders and large BDM forces who are ready to train them and assist, brokers don’t have to go it alone.”

Overcoming those barriers also provides brokers with the confidence that they are capable of stepping into the space. Pepper Money’s head of commercial, Malcolm Withers, said that if a mortgage broker could gather the information for a home loan from a self-employed customer, they would find commercial lending not that different.

Part of Pepper’s training is designed to help brokers build that capability to have the conversations with their clients and create the kind of experience for them that would mean they wouldn’t lose those customers.

Withers said it was not all about building skills but about helping brokers gain the confidence they need to ask the right questions. He did warn, however, that different areas of commercial lending have different levels of complexity.

“Certainly, there’s commercial business that is complex, and it’s tough,” Withers said. “But the vast majority of lending to small businesses, which are families, which are mums and dads – they’re really in the heart of a lot of what we’re seeing brokers step into, realising their capability levels are there so they can make the transition simply across to that commercial lending and smaller SME space.”

The market over the last year has also resulted in many mortgage brokers being simply too busy with residential mortgages, so they are putting commercial deals on the backburner.

Robynne Frost, Suncorp’s executive manager, broker partnerships, business banking, added that with the complexities of the last year brokers have needed the right skills to help businesses.

She said that around 10% of Suncorp’s broker partners were qualified commercial brokers, and about 45% were mortgage brokers who were happy to stay in the residential space. She predicted that around 35% were already starting to diversify their offering.

“At Suncorp, 40% of our residential customers are self-employed, so we see it as a huge opportunity for brokers to transition into commercial lending by simply knowing your customer,” Frost said.

“It’s important for brokers to expand their conversations with customers to understand more about their business and needs. Start by asking what’s happening around the business. What are you looking at in terms of expansion? What are some of your challenges? As business owners they want brokers to help them navigate all of that and make the switch easy.”

While Wright agreed that for mortgage brokers it was a challenge to build a strong, consistent capability across mortgages, business lending, property investment, asset finance and so on, he said a lot of brokers were “waking up” to the idea of having a conversation about how to get those clients, and about partnering with others.

“That network of brokers works together to keep the client with that broker but gets the need fulfilled in a different way,” he said. “That’s what’s changed significantly: knowing they can partner with another broker to get the client’s needs met – or they get serious and build the capability across all those streams.”

The recent threat to broker remuneration has also been a catalyst for getting mortgage brokers to think more about diversifying. Bannister said that, with remuneration once again coming up for review, and given that a change, if any, is unlikely to impact the commercial remuneration model, brokers were again likely to turn their attention to commercial diversification.

On top of this, he said the barriers to entry into the commercial lending space had opened up with the emergence of new lenders, “whether that’s through the non-banks we see here today, but also fintechs as well, making it a lot easier to digest for brokers who haven’t written commercial before to at least get a handle on it”.

“I think that’s complementary to the banks’ offering as well, so that gets brokers into the space, gets them moving, and then they start to build out their capabilities further from there.”

BROKER QUESTION

Q: What can mortgage brokers expect in terms of remuneration in commercial lending? Is it similar to residential commissions, for example with upfront, trail, clawback?

Brendan Wright, FAST: They should alk to their aggregator. The reality is it’s pretty straightforward for lending solutions to the SME segment, as consistent as it is for mortgages. It’s circa 0.65 upfront and 0.15 on average for trail. Where it does get different, though, is when you move into large and complex solutions: for these types of deals, remuneration is negotiated on a case-by-case basis. Typically, for large deals there is a mix of mandate fee, upfront and trail – these will vary depending on the nature of the transaction, ROE for the lender and, most importantly, ensuring you deliver the right solution for the client with fair and competitive value.

Malcolm Withers, Pepper Money: The only thing I’d add is that, on average across all lenders, you tend to find a slightly higher trail than they get on mortgages. It’s on par for upfront, but it’s higher trail on average. I’d ask a different question here: can you afford to lose remuneration by giving up an existing customer to another broker who offers commercial loans?

Anita Hyde, NAB: When you get to the higher-end loans, it really comes back to how much the broker wants to be involved. Again, when you’re talking about ongoing annual reviews for some of those corporate transactions, there’s some brokers that say, I’m happy to be involved, I want to be involved in every single conversation and dialogue, and that plays a big part in what that remuneration looks like as well.

John Mohnacheff , Liberty: The wonderful thing about commercial lending is that with the remuneration there’s enormous flexibility. If you’re doing a deal and say, you know what, I don’t want the upfront or the trail, we’ll adjust the rate. You can negotiate the terms, and I believe lenders on this panel would say, we’re open to that.

Danny Adams, Prime Capital: It depends on the complexity of the transaction. With transactions that are very simple, there’s a speed element that’s needed, and so a small upfront fee is asked for, but if somebody is bringing a construction deal, they’ve helped put the feasibility together, I absolutely think that that broker should be charging a higher fee; they’ve worked very hard for it.

Q: Mortgage brokers have the perception that commercial lending is very labour and time intensive. How accurate is that?

A passionate advocate for mortgage brokers diversifying, Mohnacheff said this perception was “a myth that must be debunked”.

“We’re not talking about going out and tackling BHP funding or creating Rio Tinto’s international deals; we’re talking about small-to-medium enterprises,” he said, adding that anyone who could write a personal loan could write something like a car loan, and the support was there for anyone who needed it.

“It might be office space, it might be a tilt slab, it might be a piece of equipment, it might even be a simple little utility – most small businesses have to buy something, and it’s not difficult. There is so much online training, there are BDMs, there are so many systems out there now where you simply follow the bouncing ball. Complete the application form and you’re 90% of the way there.”

Having some familiarity with the mortgage broker’s point of view, Adams said he often spoke to them about writing commercial loans and saw the “fear setting in behind the eyeballs” at the prospect of having to under-stand business cash fl ow, balance sheets, and profit and loss statements.

But he agreed with Mohnacheff that commercial lending could actually be very simple. He estimated that around 5% of commercial lending was based on cash fl ow, with much more of it based on secured lending.

“Half of all of the lending in this market is secured by a residential property, which is the exact same asset class as these mortgage brokers have a lot of comfort dealing with in the first place,” Adams said.

“It can actually be a lot easier to use this asset class and obtain a commercial loan. To turn the question on its head, I meet quite a lot of commercial brokers that only deal with commercial, and they think that dealing with a residential loan would be a time-consuming and complicated process.”

Saying there was “no doubt” that myth-busting was required in this area, Wright agreed that commercial lending could be much more straightforward for a mortgage broker, particularly thanks to innovation in products, platforms and competition across lenders.

He believes there is also a lot of opportunity for brokers who do want to step it up, expand their knowledge in the commercial space and differentiate themselves in the market.

“As a broker who provides debt advice to business owners and meets their personal needs as well, that’s an enormous opportunity,” Wright said.

“The reality is, it’s easier for an SME to get hold of a broker than it is to get hold of a banker. Don’t get me wrong; we need good bankers, and we’ll continue to need those, but that’s the fact. That’s the reason the mortgage broking industry grew so much: access to someone who can help [borrowers] out.

“So, one, don’t be scared to get into it; two, there’s opportunity: build your capability to grow and do some amazing things in your business for other business owners.”

Giving an example of a mortgage broker who recently wrote a commercial loan with Pepper, Withers said they had found it so much easier dealing with a non-bank than a bank. He believes banks are often what makes brokers think commercial lending is difficult.

“Traditionally, they’ll refer it to a certain lender, and the amount of hurdles they make them jump through, the amount of running lot of time in making sure its bankers under-stand the broking industry.

“Our organisation has a deep appreciation of how valuable the broker network is for our business, and the importance of the skills and expertise they bring to customers,” Frost said.

Q: How are you supporting brokers who do want to diversify?

It’s no surprise that, as a business that actively promotes diversification, Liberty provides support for those mortgage brokers who want to expand into other areas. Mohnacheff said brokers had “an obligation” to broaden their sphere, and Liberty in turn provided education and training.

“Someone helped you start your business and trained you and invested in you and worked with you to get you to the level you are now. I think there’s an obligation to continue on your journey of discovery and to grow your business and help other small businesses grow,” he said.

“There’s a lot of people that will hold your hand all the way through. We’ve got about 17 BDMs across Australia dedicated to cash fl ow lending and commercial lending, and we’re running education and seminars at least every week.”

Education and training is something NAB is doing as well, said Hyde. In the current environment the major bank is working closely with aggregators to make sure training can be done in a COVID-safe way. The bank is also focusing on how it supports female brokers in entering the commercial space.

“We recently held a series of women in finance events and held a spotlight series on women in the commercial broking space for brokers, bankers and business leaders, just to really advocate the support network that is available for women looking to enter the commercial space,” Hyde said.

“We all know that diversity brings a different train of thought, and the more diversity we can bring to the table, the more we can deliver greater outcomes for our customers.”

Street said the support given over time by lenders, aggregators and the principal industry bodies had contributed to the growing number of mortgage brokers writing commercial loans. Thinktank itself works closely with brokers and aggregators to provide specific training suited to the broker.

“We’re working with industry partners to deliver the right sort of training to the people who want it, rather than saying, here’s a training course, come along if you like; it’s ultimately up to the broker how far they want to go,” he said.

“We can deliver really tailored training to them that supports what they’re after and takes them to the next level, and we step up the training and follow the pattern they prefer.”

BROKER QUESTION

Q: What similarities/differences are there in the commercial lending space, for example when it comes to turnaround times, documents?

Cory Bannister, La Trobe Financial: It’s the same process for us, whether it’s residential or commercial, so brokers can expect the same turnaround time. The only exception I would say is in development finance, which takes slightly longer because largely we’re waiting for more documentation from third parties, but generally, if it’s commercial, a simple transaction probably up to $15m, for us you can expect a similar process and turnaround to residential.

Robynne Frost, Suncorp: The way Suncorp processes combination transactions for SMEs sets us apart from other lenders. Over 60% of Suncorp’s small business loans include home loan transactions, which allows us to assess these as one transaction via our SME credit assessment team. It means we can deliver a more streamlined experience for our brokers and customers.

Jonathan Street, Thinktank: The valuation process is a little bit longer than for resi. Brokers who are new to commercial often get caught out by that. When you’re on a commercial transaction, getting started early on with the valuation, or at least engaging the right parties and the lender on it relative to timing for settlement, whether it’s a purchase or a refi, is a key thing to be on top of.

Danny Adams, Prime Capital: In cases where the loan is very heavily focused on the asset-backing rather than a higher degree of servicing capacity, I’d expect the turnarounds to be significantly quicker. It’s very much market driven; I’ve yet to hear of a small business that’s said, don’t worry, I’ve got all the time in the world. They’re expecting to get decisions and answers much quicker. The other difference could be pricing, which is certainly going to be different.

Q: What are your expectations for the year ahead in the commercial space?

At last year’s roundtable, just a few months into the COVID-19 pandemic, there was a general feeling that it was too hard to predict the following 12 months. This year, the group were a little more confident.

Hyde said that after a challenging year in which businesses have had to look to innovation and new opportunities, the year ahead would see a “business-led economic recovery”. Technology and innovation would remain important, and NAB would continue to explore ways to simplify and digitalise its processes.

“I think as the economic recovery continues and the vaccine rollout gains pace, the outlook is positive, and there are plenty of reasons for us to be optimistic for the future,” Hyde said.

“We’re seeing a significant demand in new lending coming from commercial brokers, and we expect that to continue. NAB will be that banker behind the broker, so providing faster and simpler access is going to be critical to our path forward.”

As the economy recovers, Thinktank anticipates a continued resurgence in commercial lending activity, along with larger loan sizes coming through. Agreeing with Hyde, Street also expects more innovation, which should lead to faster processes and turnaround times, as well as new lenders emerging and increasing competition.

After the impacts of the pandemic, Thinktank is also preparing to see more alt-doc borrowers needing finance.

“We’re expecting a lot of alternative verification whilst full-doc is a bit challenged with some interruption to financial results because of COVID,” Street said. “Mid-doc [loans] provide borrowers a quick solution, but they can transition to full-doc later on. There’s been a big pick-up in our experience there, and we expect that to continue to play out over the next 12 to 24 months.”

Pointing to some of the challenges the industry has faced with supply and cost pressures, Frost said cash fl ow was improving. She believes the economy is showing “great signs” of business and consumer confidence, and that an area seeing particular growth is the agricultural market.

Overall, Frost is positive about the future. “We’re pretty excited about the next couple of years,” she said.

“Complementing what Jonathan said, we’re going to see some new lenders, and I think we’re all absolutely equipped to continue helping our brokers and small businesses grow in Australia.”