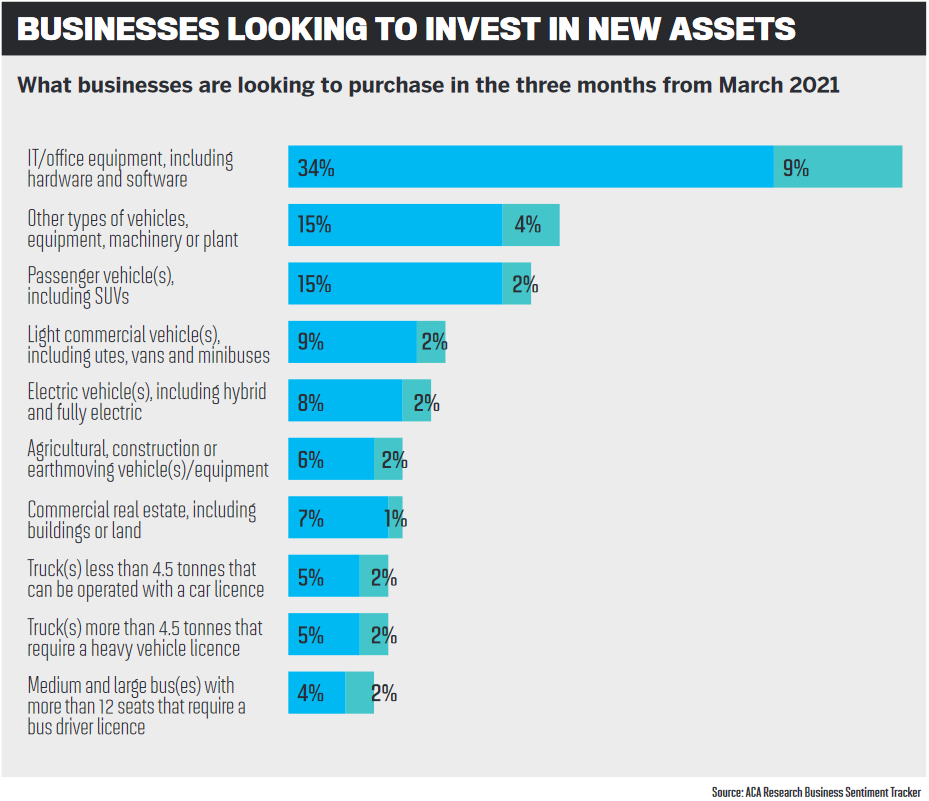

Many businesses are looking to invest in new equipment this year as they focus on growth and recovery following the challenges of 2020

If you could turn an office upside down and shake it, anything that fell out could be financed.”

That’s how someone once described asset finance to the head of aggregation at Specialist Finance Group, Blake Buchanan.

Asset finance is going to be a big opportunity in the commercial lending space this year as businesses recover from the effects of COVID-19.

According to a survey from ACA Research, 22% of businesses are looking at increasing their business spending or capital investments. Among those planning to purchase assets for their businesses, 43% are seeking to invest in IT/office equipment, including hardware and software.

Vehicles – which are often front of mind when thinking of asset finance – were the next most popular items businesses were expecting to spend money on. Seventeen per cent said they were planning to buy passenger vehicles, including SUVs; 11% were looking to purchase light commercial vehicles, including utes, vans, and minibuses; and 19% wanted to invest in other types of vehicles, equipment, machinery or plant.

Reflecting on the asset finance space in 2020, Buchanan says it was interesting to see two very different results in terms of the impact on businesses.

“Some people spoke about JobKeeper being the only thing keeping them afloat, but then others were booming, such as mortgage and finance brokers. This presented different challenges but also opportunities for each,” he says.

“Some people spoke about JobKeeper being the only thing keeping them afloat, but then others were booming, such as mortgage and finance brokers. This presented different challenges but also opportunities for each,” he says.

For those businesses that suffered a loss of trade or even had to close their doors, there was an opportunity to reflect and potentially modify the way they did business, which many did successfully.

While demand for asset finance dropped at the start of COVID, it bounced back to greater than normal levels “fairly quickly”, says Buchanan. However, the supply of assets is still delayed in many areas, depending on where they are coming from.

Thanks to border restrictions and closures, items coming from overseas have been held up, he says, and there is also a backlog of demand for vehicle purchases in particular as many factories are in locations where hard shutdowns were put in place. This has slowed down some transactions, but business in other areas has made up for this.

Economic recovery a pathway for brokers

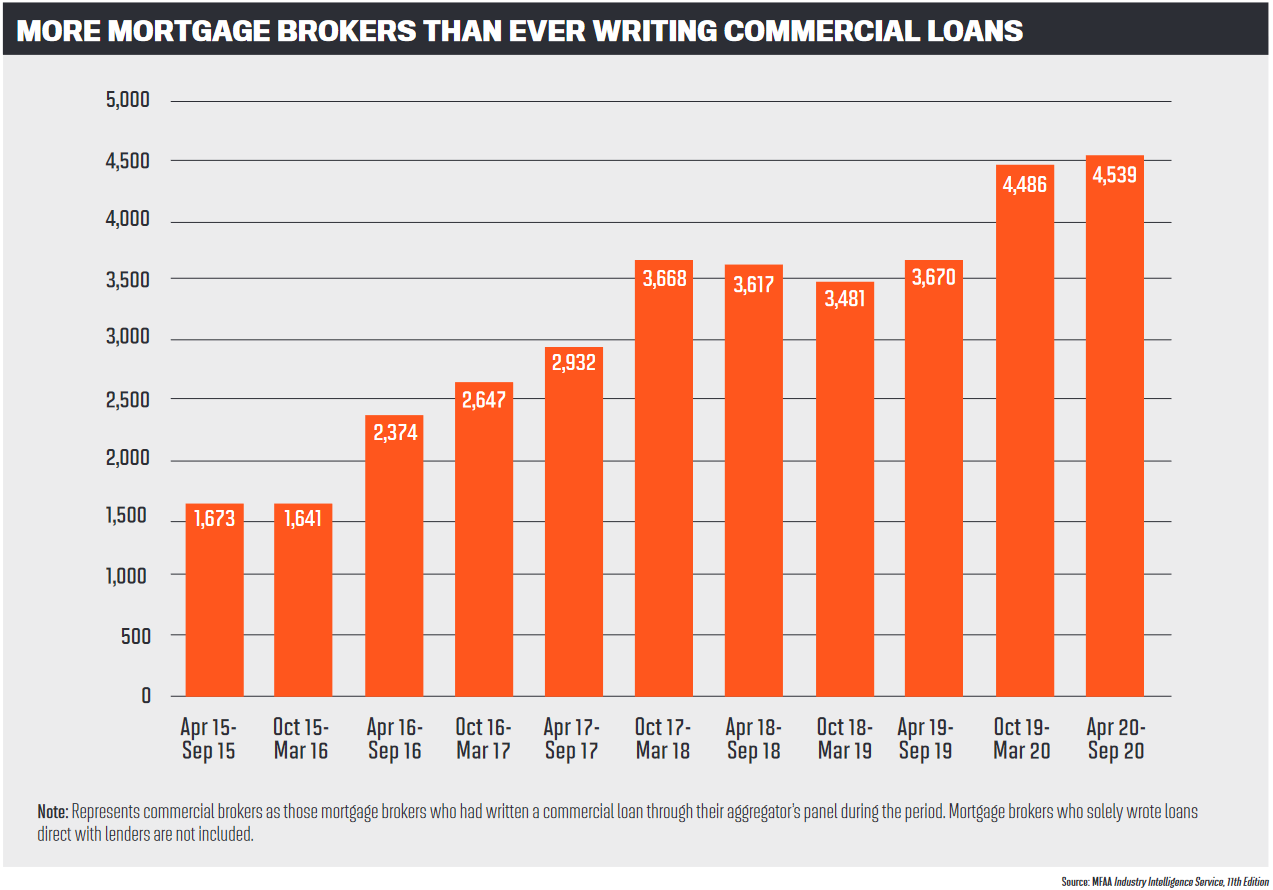

Confidence is now up, and cities like Sydney are almost as busy as pre-COVID levels; employment levels are rising, broker market share is on the rise, and demand for finance has not waned.

“This points to a stable short- to medium-term recovery but is dependent on things going well, with no more mass and lengthy shutdowns,” Buchanan says.

For mortgage brokers, he believes the opportunity is always there to diversify their offerings – not just in the current market. Buchanan warns, however, that it is rare that a broker can perfect their expertise across the residential, asset and commercial finance sectors. Instead, those that have excellent diversified offerings usually achieve this through partnerships or by employing experts in the field.

“The first step towards diversification of your business is education. Brokers need to be skilled to a level where they can identify opportunities to assist their clients in these areas,” Buchanan says.

“A perfect example might come up with a home loan application from a self-employed client. In their A&L there may be a vehicle under the business that is four years old. Is it likely that they will need finance for a new vehicle soon to take advantage of some tax incentives or as the vehicle depreciation schedule is at an end?

“A broker should ask these types of questions and offer to assist. There are plenty of resources and people available who can assist brokers with placing such deals.”

Buchanan also gives an example of a baker who runs out of bread every morning. Through a simple conversation, the broker can identify the problem and offer the solution of an additional oven.

“Through financing the asset, the baker doubles production and profits without having to dip into capital to fund the purchase,” he says.

Depending on the asset class, it should not be too difficult for brokers to access providers and information, Buchanan says. Nevertheless, the requirements for simple asset transactions usually involve less work than a home loan – though for different items more work is often needed.

“Purchasing a vehicle that you use to get to and from jobs is vastly different to, say, purchasing a plane or special purpose vehicle,” he says.

Funders’ changing appetite pushes SMEs to non-banks

According to another experienced commercial broker, education is key to success in this sector. Managing director of Atlas Finance Matt Atkin explains that having the ability to read and understand financials and then present the deal to the right lender takes time and is different to what most mortgage brokers do on a day-to-day basis.

From his perspective, asset and equipment finance has not changed a great deal because of COVID. While he saw a spike in clients and accountants wanting to raise capital early on, that evened out, and Atkin found that there were enough other working capital products to achieve the same thing.

The biggest change in the space was funders’ appetite for risk.

“Many pulled their streamlined products, which meant that brokers without the necessary skills struggled. It also blew out the turn-around times as funders had to change their processes and upskill their people whilst having them work remotely,” Atkin says.

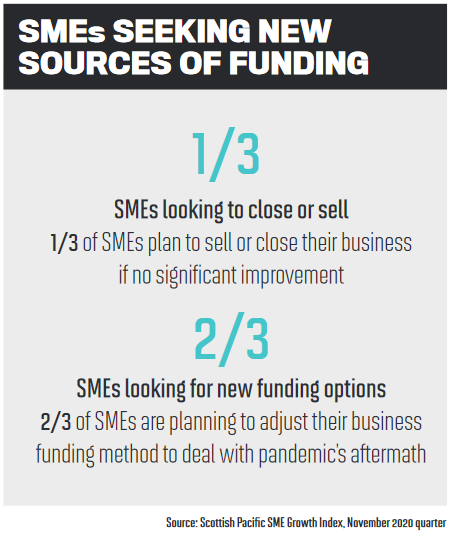

This also meant he saw a rise in non-bank lenders taking on more risk but at a higher margin. This is backed up by research from Scottish Pacific, which showed that almost a quarter of SMEs actively diversified their funding base to fund new business growth using non-banks.

“I believe this is another positive for the industry as SMEs now have access to funds across a range of lenders at fair rates,” Atkin says.

Diversified broker business broadens client base

Atkin knows first-hand how a diversified offering can benefit a broker’s business. After setting up Atlas Finance with other equipment finance specialists, the brokerage decided to expand into residential mortgages and commercial insurance.

“The diversified offering was one of the reasons our business weathered the storm in 2020. We can off er our referral partners and clients solutions and insights that most others cannot, because we have such a wide set of skills in our business,” he says.

“The broking market has many capable people, but we are trying to differentiate ourselves by building a business that has scale to be able to service a large, diversified client base. We cannot do this without a broad offering.”

Five months into 2021, Atkin remains positive about Australia’s economic recovery. Funders are lending again, but it’s expected that the challenge for many clients will be to convince funders that they can afford to service new debt when their 2020 numbers don’t support it.

“Many of the funders are saying they will be commercial where possible, but time will tell. Access to capital will play a huge part in Australia coming out of the COVID recession,” he says.