Roundtable discusses broker partnerships, customer focus

The final few months of 2022 have been a tough time for non-banks and their broker partners.

In November, the Reserve Bank of Australia lifted interest rates for the seventh month in a row, taking the official cash rate to 2.85%, up from 0.10% in May.

Homeowners on variable rates are doing it tough, dealing not only with higher mortgage repayments but ballooning cost of living pressures due to runaway power, gas, petrol and grocery prices. The RBA is predicting inflation to hit 8% by year-end.

House prices are also falling, with CoreLogic figures showing values fell by 6% nationally in the six months to September and dropped 10.2% in Sydney. New property listings were also down 7.5% month-on-month nationally in September.

But while these factors make things challenging for the Australian economy, the nation’s non-banks are in a healthy financial position and primed for further growth. This is largely due to their strong relationships with brokers, who are increasingly turning to non-banks to help their customers, such as self-employed clients and small business owners who don’t fit the typical vanilla, prime loan profile favoured by the major banks.

The non-banks understand that the big banks have increasingly moved away from alt-doc and SME clients, choosing to focus on the high-volume prime residential home loan space. This gives non-banks the opportunity to service a sizeable portion of the population who are looking for residential or commercial finance and can’t find it anywhere else.

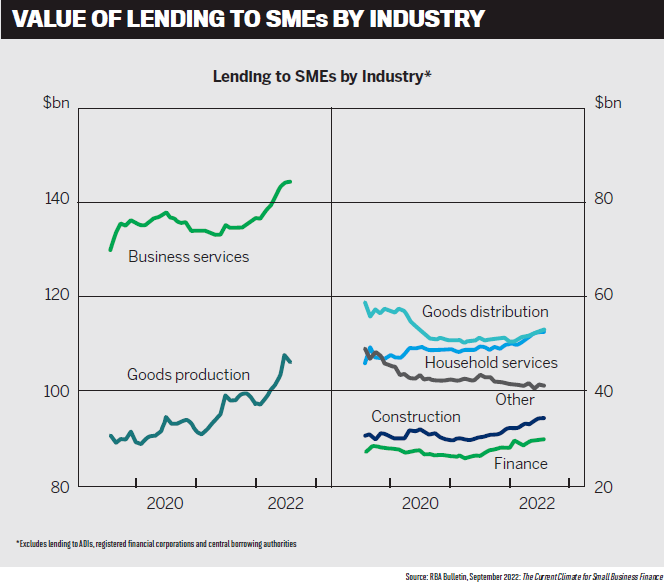

Growing numbers of mortgage brokers are turning to non-bank lenders and also writing commercial loans. The latest MFAA Industry Intelligence Service report for the six months ended 31 March 2022 revealed that 29% of all mortgage brokers had written at least one commercial loan.

MPA invited representatives from some leading non-banks as well as two brokers to attend the 2022 Non-Banks Roundtable held at Seta Sydney. Topics discussed included how non-banks service the broker channel; competition with banks; growth segments; commercial lending and more.

Participants were John Mohnacheff, group sales manager, Liberty; Cory Bannister, senior vice president and chief lending officer, La Trobe Financial; Barry Saoud, general manager mortgages and commercial lending, Pepper Money; Chris Paterson, general manager distribution, Resimac; Steve Sampson, CEO, Prime Capital; James Angus, chief customer officer APAC, Bluestone Home Loans; Lee Prior, distribution executive, ORDE Financial, and Chris Calvert, executive general manager – distribution, RedZed.

The two broker representatives were Rose Renouf, head of Zinger Finance, and Chris Straw, director and senior mortgage and finance consultant at You’re Welcome Finance.

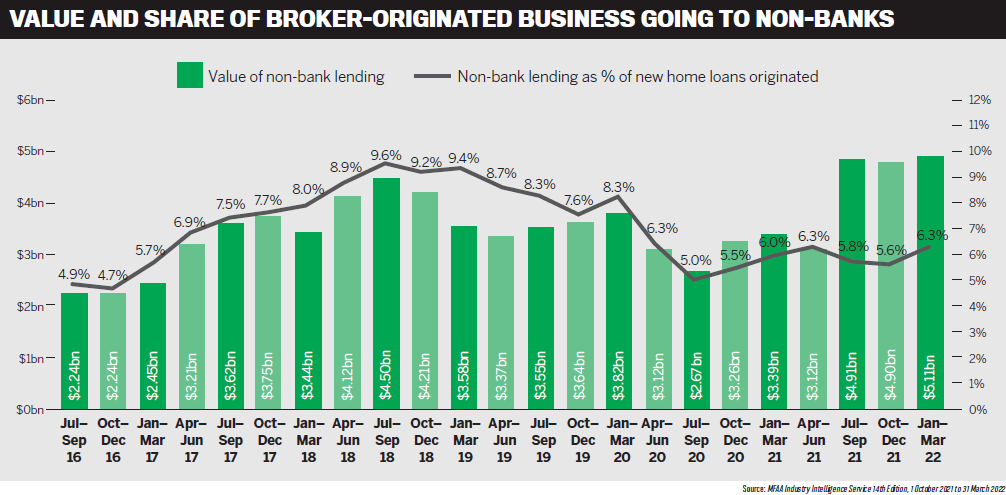

Q: The MFAA’s Industry Intelligence Service report for the six months to end September 2021 showed three consecutive quarters of growth in broker-originated loan market share for non-banks from December 2020, with a 0.5% decline to 5.8% in the September 2021 quarter. The latest report shows that this recovered in the March 2022 quarter and was up 0.7% to 6.3%. Broker-settled loans through non-banks are at a record $4.9bn [now $5.11bn]. What do your own figures show in terms of how you are performing in the market, in particular with broker-sourced loans?

Mohnacheff got the ball rolling at the roundtable, saying that as non-banks, all those attending the meeting were predominantly focused on the broker market.

“The one thing we have learned is that when things begin to get a little bit unset-tled in the marketplace – many brokers have not experienced so many rapid rate rises, and it has unsettled not only some brokers but a lot of mums and dads and mortgage holders – this is the time when the non-banks shine,” he said.

“This is when we go and make ourselves even more available to the brokers to help them navigate sometimes a very difficult situation, such as multiple debt consolidation and refinancing.”

Mohnacheff said customers were going to brokers and brokers coming to non-banks because “we have a very balanced view about how to refinance and how to restructure debt”.

“Due to that, there’s more and more trust going to a broker from the consumers and from the brokers to the non-banks. A lot of them have longstanding and long-trusted relationships with us.”

Bannister (pictured above) said the increasing number of brokers using non-banks (6.3%) was pleasing, but it was also important to recognise that there was still lots of scope for growth in this sector.

“If you look at the historical trend, it was about 8.5% to 9.5% allocation [of brokers using non-banks] over a two-year period leading up to COVID,” he said.

When the pandemic hit, the government provided stimulus funding to major banks, which was important at the time for the sector as a whole, Bannister said. This included giving banks a 0.1% interest rate for three-year fixed-rate funding.

“More and more borrowers sought out major banks, and we [non-banks] got down to 5% [market share]. So we see the return to normal allocations being 8% to 10%. Pleasingly, the sector is already seeing record volumes, with $5.1bn settled in the most recent reported quarter; there’s plenty of opportunity there.”

Bannister said the addressable market for non-banks was expanding. “There’s $2trn worth of residential mortgages in the system, about $600bn of commercial, and they turn over every four years, to the amount of approximately $650bn per annum. Going back to pre-GFC, non-banks were running almost 20% of the [loan] volume in the country. That’s $130bn, a sizeable market that would satisfy many around this table.”

Bannister said there was “a ton of opportunity”, and La Trobe Financial was certainly optimistic about the future.

At RedZed, Calvert (pictured above) said the non-bank focused on a specific segment – the self-employed sector. “My observation is that non-banks, compared to the main bank sector, a lot of them get the service model a lot better. They’re more geared up to work with customers and deliver them a better proposition and outcome.”

RedZed recently commissioned a survey of 250 self-employed people in the SME sector, which included questions about their banking activities.

“At that time, only about 16% of those people said it was easy to secure a loan through one of the main banks, relative to the non-bank sector. That just shows you how the non-bank sector has embraced that whole customer service model,” Calvert said.

“I don’t think it’s getting any easier. While some of the banks have sharpened up their respective models, it still gives this group in the non-bank sector an opportunity to grow their market share, because they provide a more customer-oriented approach.”

Sampson (pictured above) said Prime Capital dealt solely with brokers, not with the wider market, and the non-bank had performed well.

“Even during the time when the banks were handed virtually free money, we still grew our market share enormously,” he said.

“We have expanded our participation to 11 aggregator panels now, so naturally, we’re getting a growth trajectory off the back of that, and I think that’s only going to continue. We also needed to substantially increase our BDM team, so we looked for experienced, seasoned BDMs to assist us.”

Sampson said all the non-banks at the roundtable would agree that lending was starting to quieten down and the funding market was difficult at present.

“Early next year, I think the market will change, and the banks’ margins will be depleted,” he said. “Non-banks will be in a much better position, and we’ll get some of the market share back from the banks, because there’s no doubt the banks did take the market share off us when that cheap money was available to them.”

Saoud (pictured above) said Pepper Money’s own broker market share figures reflected those of the MFAA as well as the comments made around the table.

“In the six months to June, we have had record originations. Market share was quite strong for us in the non-bank sector,” he said.

“While the home loan lending commitments have contracted recently due to the macroeconomic environment, there’s both challenges and opportunities for us to continue growing. As a non-bank industry, we’re seeing that the demographics and profiles of borrowers are changing rapidly.”

Saoud said this was where non-banks’ competitive advantage arose in terms of how they accelerated policy change and responded by providing real solutions to customers. “That’s where I think we will continue to grow market share, as opposed to the banks. They’ve got traditional and firm ways of looking at a borrower, while we’re very responsive and agile when it comes to finding a solution to suit the borrower. The more that we can continue to do that, the more we will be able to better support our brokers and customers.”

Pepper Money was also very reliant on broker-originated loans, which represented about 96% of its business, Saoud said. For non-banks the focus was investing in that channel and partnering with brokers and aggregators to “really deliver market-leading and exemplary broker and customer services”.

Paterson said he agreed with the comments made. “Our insights show that customers go to brokers for a reason. They put their trust in brokers, and in turn, it’s up to us to provide brokers with a solution. Brokers can trust that we have a broad suite of products that can cater for their customers’ needs, whether it be full-doc, alt-doc or specialist loans.”

Angus (pictured above) said Bannister had touched on something that was “worth unpicking”.

He said when the RBA provided the big banks with term funding facility money for fixed rates, that resulted in brokers writing north of 50% of their residential loan business into fixed rates.

“So when you look at those numbers in isolation, they’re interesting and they look good, but the reality is that on the resi side we’re only playing in half of the market because we just can’t compete on fixed rates.

“When you look at that growth, and I think a lot of us we’re 100%, 200%, 300% year-on-year [loan origination growth], to do that in half the market just shows the value we add to brokers and customers.”

Angus said there was some naivety about the current lending market among brokers who had only been in the industry for the last five or six years, and they were struggling to join the dots. Non-banks needed brokers and “they need us”, particularly when working with self-employed clients who don’t fit the major banks’ credit profile.

“The flexibility we all have on policy, how we can use different income documentation, even the way we service loans is going to mean that we can provide a solution to that client that nobody else can,” he said.

Angus predicted that once non-banks got through the current rocky period and things settled down, broker-originated loans would rise again.

Prior said the non-bank sector needed to keep being nimble and trusted.

“ORDE is trusted to find the deal, and in the face of uncertainty, to back the resilience of Australian borrowers, which we think can be underestimated,” he said. “When you combine these strengths with a service-first and built-for-broker mantra and highly experienced lending and management teams, we were able to establish brand presence and notable success during the pandemic.

“John [Mohnacheff] (pictured above) talked about this – we’ve got clients that have never seen a change in rate, so there’s that uncertainty there. We need to be known again as that part of the industry that provides stability, provides that education so that we can continue with our market share.”

Q: How are non-banks remaining competitive with banks in the face of higher funding costs?

Prior said that while ORDE Financial may have been the newest non-bank lender at the roundtable, specialist lending solutions were at the core of a non-bank, and “we must maintain and own the space”.

“Lenders have become a victim of their own success; the ongoing challenge at ORDE is delivering service to handle increased volumes. Our service standards are at the top end, and we must remain here,” Prior said.

Paterson (pictured above) said the answer to how non-banks competed with banks was simple: “Alternative product solutions and playing to our credit policy initiatives. The parameters, looking at what the customers’ needs are and tailoring a product to suit their needs – that’s where we can compete.”

Angus said he had worked at banks, and from his perspective, non-banks had never been rate driven. “It was always about the solution and improving cash flow. What’s immensely pleasing at the moment is the customers we’re helping today, rates are somewhat irrelevant to them.”

Debt consolidation continued to be a big factor, Angus said. While the ATO had been quite relaxed about tax debt during COVID, “now they’re starting to collect”. This meant there was a lot of tax debt that banks traditionally wouldn’t touch.

“If we just stick to our knitting, and we stay focused on the cash flow, the solution, rate becomes less important,” Angus said.

He agreed there had been a funding challenge for non-banks, which had faced “a very stiff breeze on funding”. Funding markets were pricing in today what they thought would happen in 60 to 90 days’ time.

“If you go back to July, and you look at the disconnect between BBSW [the Bank Bill Swap Rate] and the cash rate, that was 50-plus basis points,” Angus said. “We paid for that – that was a real cost to us … but at the end of the day, if we stay focused on what we do well, and we stay focused on those principles, we’ll continue to grow and thrive.”

Bannister said non-banks didn’t target the same customers as the banks, and the opportunity in the complex prime credit space was significant.

Looking at borrower quality in that space, La Trobe Financial’s independent research via Equifax showed that its borrower credit quality was in line with that of the big four banks.

“But there’s an element of their profile that’s not easily automatable,” Bannister said. “It could be that there’s a particular structure that’s not easily done by computer. It could be that they’re high net worth and they’ve reached a debt-to-income cap or a portfolio cap with a bank; we’re seeing more and more of that now.”

Investor lending was another opportunity, Bannister said.

“James [Angus] talked about ATO debts; that’s a $33bn opportunity,” he added. “It’s just sitting there for the market to fill. So, as James rightly points out, if you stick to your knitting and you stick to your core target market, let the banks play in that automated vanilla, it’s not something we are generally too concerned about.”

Sampson said it wasn’t so much the higher funding costs but the lack of supplied funding that was the problem. “We were fortunate we raised some capital just before the rates started to move up. But we’re back in the markets, and it’s much tougher to raise capital now. But talking to our suppliers, we think that January, February, the markets will start opening up again,” he said.

A lot of funders were looking at how far down the stack they wanted to be, Sampson said, with funders even coming into the lower mezzanine facilities.

He added that the non-banks had set up product suites for loan types that the banks didn’t particularly want to fund, and non-banks had helped a lot of people through adverse times. Non-banks would really come to the fore in the next six to eight months when customers were getting knocked back for loans that were previously very bankable.

“If you have a product that is an alternative type of product for self-employed people, employed mature people in their 50s and 60s, who can’t get big cash out from a bank, I think these are the areas that need to be targeted, and non-banks can carve out their niches,” Sampson said.

Similarly, Saoud said Pepper Money was not competing for the vanilla, PAYG prime customer. “Our competitive advantage and differentiation is primarily around providing a solution to the non-traditional bank customer, whether it’s someone who is self-employed or a customer trying to consolidate their debts,” he said.

“We as an industry are able to be responsive and agile due to our smaller business structures that allow us to accelerate credit policy, product, technology, or process changes to cater and respond to those changing borrower demographics and segments.”

To round off the conversation, Mohnacheff came back to the subject of ATO debt.

“If you’ve got an ATO debt, it’s because you made a profit,” he said. “It’s the ability to look at it and say, ‘OK, what is the situation and how can we help you?’ ATO debt can be a good thing as viewed by us; it’s one prism through which you look at that individual and that business.”

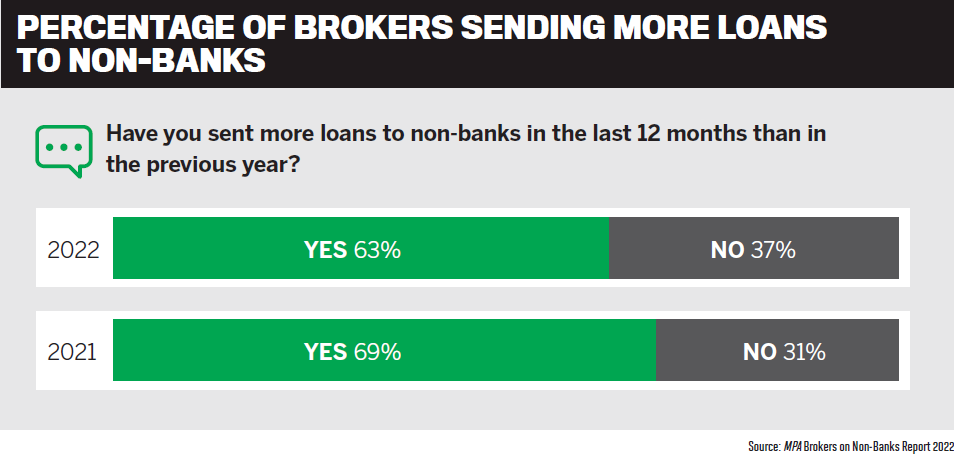

Q: The Brokers on Non-Banks 2022 survey revealed that 63% of brokers were sending more loans to non-banks in the last 12 months than in the previous year. Why are more brokers choosing non-banks, and what improvements have you made to technology and your processes to boost this channel even further?

Calvert said more brokers were choosing non-banks because of their service proposition. “Particularly in the small to medium enterprise sector where people don’t have time to wait 24 days for the approval of their applications. They want a quick response; they want product flexibility. They want to know if they make a call, it will get answered within 25 seconds. They want to know if they send an email, they will certainly receive a timely response. Turnaround times are critical.”

Due to the way non-banks had been set up with their staff and infrastructure, being far more responsive was important, Calvert said. “As a customer, we always want to have a quick turnaround time and real voice response and not be waiting on the phone for 20 minutes. You also don’t want an automated voice.”

He cited a very recent example of when he rang a bank trying to change credit cards for his mother. “After pressing half a dozen buttons, I was cut off and told, ‘No one’s avail-able to take your call’. That is an example of poor customer service; it creates the wrong impression and makes you think long and hard about whether you would use that bank again.”

The biggest advantage for non-banks was service, Calvert said. “Time is money for these [customers]. They’re often self-employed, a small-to-medium enterprise; they haven’t got time to sit on the phone for 20 minutes just to get a voicemail. And they’re often prepared to pay a little bit more in price for that convenience.”

Bannister said there were two drivers behind why more brokers were choosing non-banks.

Firstly, it was the “phenomenal” maturity of the sector in the past 10 years and a general acceptance that non-banks provided a genuine alternative.

“If we were sitting at a roundtable six or seven years ago, that conversation would be different,” he said.

This customer acceptance was thanks to “the great work of every player in this room”, who were responsible for “incredibly well-run, mature, responsible businesses”.

“Some of us are publicly listed, so they’re very transparent in the way that they go about things. That’s helped raise the profile of the sector generally and built a lot of trust amongst brokers,” said Bannister.

The second driver of brokers favouring non-banks was the human touch.

At the start of the pandemic, borrowers were told by banks that they would be treated as prime credits if they sought hard-ship assistance or there was variability in their income and expenditure. Bannister said that was good in theory, but it was hard to automate.

“Therefore, [these brokers and customers] generally find their way back to the non-bank sector, because it needs some level of under-standing and some level of manual intervention to do that,” he said.

“For us, it’s less about tech; it’s more driven by humans. The human element is critical to this component of what we do.”

Finding talent in the last 12 months had been hard – to find the right people, pay them, train them and get them on board in quick time, said Bannister.

Angus agreed. He said Bluestone conducted Net Promoter Score surveys once a quarter, and people were the drivers of NPS scores – BDMs and underwriters.

“We just do the simple things well. We have the time, and I think we actually understand the importance of an underwriter picking up the phone and calling a broker,” Angus said.

“All around this table, we have quality people in the field, and we have quality people underwriting loans, and they all understand or respect the role the broker plays, whereas I don’t think that’s always the case with a lot of our bank competitors.”

Saoud said, “As an industry, we care for the broker. We understand what their needs are, including the importance of speed, transparency, consistency and predictability, as well as a personalised approach to lending and relationship support.

“It’s through those touchpoints we’ve invested in to make a difference. So, whether it’s having that right BDM team, credit underwriting optimisation, evolving technology and improved business processes has been critical.”

Saoud said non-banks had also stepped up the game in terms of investing in those touchpoints to make a difference. “At Pepper Money we have continued to heavily invest in those personalised broker and customer touchpoints. Investments in next-generation technology development and delivery practices, rapidly evolving automated processes, credit underwriting optimisation and new tools such as e-signing of loan and application documents and launching NextGenID – all of which had been created with a singular focus on the broker and delivering for them and their customers.”

Prior (pictured above) said advancing technology was now set to support and dramatically improve the personal touch provided by great lending teams and so valued by brokers. “Alongside a human touch, brokers want to get a rapid yes, a dependable yes, to get back to their customers, and they want quick processes and a broader product range to service a wider variety of borrowers in the sector.”

Straw said that from a broker’s perspective he was certainly seeing the rise of non-bank lending at You’re Welcome Finance.

“You guys will look at stuff, but the major banks, they’re very tight in their ways,” he said. “You’ve got a sensible approach to borrowing capacity, so we’ll start putting more deals there to satisfy client requirements.”

Straw also echoed Angus’s comments about BDMs, praising the non-banks for having excellent, responsible BDMs with a sensible approach to credit. “They’ve just really helped us get the deals set. With an RHI issue, you guys will say, ‘why?’ we’ve asked that question; it gets treated sensibly.”

Conversely, he said the major banks can sometimes ignore the fact that they have good clients coming to them who have good income streams and assets but “may just have a life problem that just needs to be answered”.

Asked if there were areas where the non-banks could improve, Straw (pictured above) said his biggest bugbear was that 15 years ago, they put a line in the sand: a maximum loan of $1.5m per security. Since that time, property values had quadrupled in Sydney, yet the limit had never been raised. “So I look at it and go, why can’t we have a low-LVR, high-dollar value per security? So a $4m loan against a $10m property? To me, that seems like a good deal, but I can’t get that set anywhere except for at a couple of lenders. I’d rather do one home in Vaucluse than 10 in Bankstown at 80%, but I would love to understand the reasoning behind the lack of competition in the larger full-doc, low-doc space.”

This led into Straw’s question to the non-banks represented at the roundtable.

Q: Broker question from Straw: With alt-doc loans, why is it that most lenders have a maximum loan amount of, say, $1.5m at 80% LVR, or at best $2m at 70% per security? Could it be feasible to consider higher-value loans with lower LVRs (say, 50%) with single security?

Mohnacheff said these types of loans could be done, but generally on a case-by-case basis.

“Show us the deal and let’s have a talk about it. Do we have an appetite? I think the best place to go is to ring your BDM and ask the BDM, ‘Hey, I’ve got this deal. Do you want to do it? Yes, or no?’ ”

Sampson said that due to the way non-banks were funded, there were restrictions on warehouses and the types of acceptable security for these loans.

“There are ways to be creative with that,” he said. “We certainly do them, and that’s the value of having more than a standard warehouse. So we can cater for this. A lot of brokers probably look at non-bank lenders as a kind of non-conforming alt-doc, but we have a swag of high-net-worth people that just can’t satisfy banks; they’re very asset rich.”

Sampson gave an example of customers in their 50s or 60s who wanted “a slab of cash out” but the banks refused because they were too old or lacked an acceptable exit strategy in the banks’ eyes.

Paterson said Resimac would “absolutely” consider exceptions for high-net-worth client loans. “It’s about the overall picture of the application,” he said. “If there is a low LVR, it mitigates the overall risk of the application if there is a high loan amount. And it’s something I would workshop with a BDM, and most good BDMs will be able to find a solution for you.”

Bannister said the answer to Straw’s question was clearly funding-related: “you’ve got to have funding that matches”.

He said most non-bank lenders were bank-warehouse funded, with most of their funding coming from three of the big four banks in Australia and possibly some international banks. “The eligible loan criteria, which includes loan size, and portfolio parameters that are attached to the warehouses, are all almost the same.”

The other source of alternative funding for non-banks, Bannister said, was debt capital markets, with investors relying on rating agencies such Standard and Poor’s and Moody’s to rate those tranches of loans, which were subsequently sold to investors as residential mortgage-backed securities.

However, he said La Trobe Financial also raised its own funding via its $8.5bn Credit Fund, a strong point of difference from the other funding models described, in that it allowed the lender to offer a broader set of products that went deeper in terms of loan size and flexibility.

Saoud added that a potential change to non-bank funding structures was occur-ring, and he expected it would evolve to enable non-banks to cater a lot more for the particular borrower profiles Straw described and compete better in that space.

Angus said lenders such as La Trobe Financial were not solely reliant on a traditional warehouse securitisation structure. “They’ve been quite creative around the way they fund, and I think something we all need to do is put a bit more pressure on our own treasury teams and get them to think out of the box so we can do this business.

“We’ve just put through a heap of policy changes, and some of them took over 12 months,” he said. “Some of them we put in front of funders in November last year, and here we are in October and we just put them on market.”

Angus said that because non-banks were dealing with the same major banks for funding, it was time for them to fund differently so they could be in control of their own destinies, with the ability to do the types of loan deals Straw suggested.

Asked why Zinger Finance chose to work with non-banks, and about the advantages they provided, Rose Renouf (pictured above) explained that the brokerage had a lot of investor clients, and non-banks were suitable for these borrower types.

“We probably write 130 loans a month, and 30% go to non-banks,” she said. “The reason is serviceability, and an easy [home loan] calculator. We’re quite busy, so anything that can quickly calculate – normally we choose a lender, like Pepper, for example; they’ve got an easy calculator.”

Renouf said that banks were no longer catering for investors (for example self-employed clients, where their financial statements were not available), and these clients preferred non-banks because of the way they assessed servicing. “Also, with investors, they’re not rate-conscious. It’s about who will lend them the money,” she said.

She added that investors didn’t often see the properties they were purchasing, so by choosing a non-bank they got full valuations, which helped the investor determine if the security was good.

For investors with multiple proper-ties, Renouf said cash was important; they preferred maximum LVR with a 20% deposit.

“The only thing I find difficult is if you do low-doc with Pepper Money, the cumulative borrowings are only up to 1.5 times. We need more than that,” she said.

“That’s the exposure for each individual, maybe not per security but per individual. Maybe it could be expanded a little bit; maybe you can go up to three, not per security but the cumulative borrowings.”

Another tool Renouf said she loved when it came to loan applications was IDYou. “I know some of you don’t use it, but for VOI, IDYou is so handy. It means so much to us when we can identify someone easily.”

Renouf then asked her question of the lenders at the roundtable.

Q: Broker question from Renouf: If a home loan borrower was experiencing hardship, unable to meet their commitments due to loss of their job, higher interest rates and the higher cost of living, how would you as a non-bank respond to this? Would you repossess the property or offer the customer a lower mortgage repayment, which could be below the required minimum repayment?

Mohnacheff took the lead on this question. He said during the GFC, nobody was thrown out of their house.

“We work tirelessly. We give holiday repayments; we will work with customers to keep them in the house. It’s much better for every-body, and throwing somebody out of their home is terrible. It’s terrible for us, terrible for the borrower, terrible for everybody. If the borrower is working with us, we will work with them.”

While there were some recalcitrant borrowers, Mohnacheff said the non-banks worked with most borrowers to protect them and the house “because we’re invested in it”.

Angus said hardship assistance had traditionally been about providing a solution where there was a temporary issue. “I think what we’ve demonstrated time and time again is the flexibility. As flexible as we are on the front end, we apply that same mindset on the back end,” he said.

“We don’t have sort of cookie-cutter rules around hardship, and a lot of the banks do … we don’t have a one-size-fits-all. It’s what’s best for the customer. How can we help you get through what you’re facing?”

Sometimes non-banks had to make difficult decisions to repossess if the client didn’t follow through or things changed, and this was something that non-banks “didn’t shy away from”, Angus said.

“I think we’ve all done enormously well in helping people when they’re on an unhappy path. We understand it, and we’ll work with them to get them back on the road.”

Repossessing a property was a no-win situation, said Calvert. “It’s clearly not a good customer experience. The challenging part of homeownership is the pride factor. Human nature is to ignore the situation and hope that it will go away. What people don’t realise is that they should approach their lender and say, ‘Look, we’ve got an issue. Can you help me?’ … We will always work with the customer to try to achieve a resolution.”

Prior said that as lenders the non-banks understood the broker market, broker businesses and the impact of a customer losing their property. “We understand that it impacts your [broker’s] business as well, and if we can help that customer through that journey, hopefully that customer stays loyal to the broker.”

Saoud also pointed out that non-banks don’t have a traditional hierarchical structure, which allows them to be flexible, scalable and nimble.

“Our point of difference is that human-touch element,” said Saoud. “From our BDM support at the forefront, to the way in which we assess credit and support the brokers throughout – it’s that personalised element; the flexibility of working with customers. This is a significant competitive advantage for all of us that we will go above and beyond to support customers where we can.”

Angus added, “Individually, we also care. I can’t count the number of times I’ve been pulled into a hardship situation to try and resolve or contribute to an outcome that’s going to help the customer. I don’t think you’d see that in other organisations.”

This was especially evident during the pandemic when Victoria brokers and their customers were in lockdown for so long.

“We all got involved in that side of things because we care. We genuinely care about our brokers and their clients,” said Angus.

Bannister said care was embedded in non-banks’ DNA. “I think about us [La Trobe Financial] – internally we don’t have an arrears division or a collections division; we have a mortgage help division.”

Renouf said the other good thing about non-banks was that they provided so many good loan products with a triple A rating, including specialist loans, meaning they “catered for everyone”.

Q: What loan segments are providing the most opportunity for growth in the next 12 months?

From Resimac’s perspective, Paterson said self-employed customers offered the most opportunity for growth.

“These are customers whose financial situation might have changed coming out of COVID, and you can look for a solution for them,” he said. “Self-employed customers who need alt-doc solutions are still considered to be good customers and good borrowers. It’s about assessing them on their income needs and what they can cater for. So, certainly for Resimac, the self-employed segment is an area we’re focusing on, particularly given how competitive we are in this space.”

Calvert said the self-employed sector was very significant for the economy, and with these clients every situation was different.

“It gets back to that difference between non-bank lenders and probably why the self-employed tend to struggle getting bank finance: their model can be unique,” he said. “For example, the customer’s business may be cyclical and characterised by inconsistent cash flow, but that doesn’t mean that their businesses aren’t performing. This is where the non-bank lenders tend to be better skilled and resourced to assess the financial capacity of this category of customer when it comes to determining loan serviceability.”

Calvert said there was an opportunity for all non-bank lenders to tap into that small business market, which he labelled the engine room of the Australian economy.

He added that the self-employed sector had been a little cautious in the last four or five months as interest rates went up. “It’s a very resilient sector, and you’re dealing with people that have got their own skin in the game. They’re very proud and hard-working, and they’ll find a way. I think it’s a sector all the non-bank lenders are pleased to be supporting.”

Sampson agreed. “I hope so,” he said, “because I just increased my BDMs team dramatically, and we’re building a growth centre for our brokers. I truly think that working capital requirements for SMEs – it’ll be the next big growth. We’ve got resilient customers that have come through a pandemic.”

He said there had been a “perfect storm” in which income was reduced and capital had baulked, but property prices had increased, so SMEs had access to working capital.

“Once the economy has settled down, interest rates settle down a bit, we’ll be targeting SMEs to help them get to the next level of their growth,” Sampson said.

Mohnacheff said there was an additional component: creating future value through SMSF lending, including long-term retirement wealth. This was a growing market, especially among self-employed people.

“More and more are starting to realise: ‘I want to control my wealth creation; I want to be in charge, but my income is very lumpy’,” Mohnacheff said. “The major funds generally don’t cater for the self-employed. With the right advice, supported by borrowings, both residential and commercial property wealth can be created.”

Saoud added to earlier comments by Renouf and Straw about serviceability being a differentiation advantage. “I think that’s probably quite important. It’s where we’ve definitely seen growth in non-traditional borrower segments, as well as investment lending and borrowers seeking to maximise their borrowing capacity,” he said.

“A key comment coming from business partners, namely brokers and aggregators, has been about diversification,” Saoud said. “Gone are the days where brokers are programmed to only deliver the lowest interest rate possible for just one asset type or mortgage. Providing a holistic service offering to a customer is a broker’s best defence against ongoing market changes and rising rates, especially in a highly competitive industry such as ours.”

Q: How are rising interest rates and inflation affecting the commercial lending space, and what opportunities are there for brokers to diversify?

Prior said non-banks were starting to increase their commercial market share, and this was due to a greater awareness of commercial lending, as well as education in the commercial space. “If we keep educating [brokers], there’s definitely an opportunity there to help with diversification. Whether rates are a key driver for a broker’s offers or not, we have to keep supporting our customers [brokers] to understand this part of the segment.”

Non-bank staff needed to be continuously educated about products and the economy, Prior said. That way the education was relevant to the industry.

Mohnacheff said he was finally seeing more brokers diversify into commercial, but it was still very slow. “About 70% of all home loans are through brokers. When we really look at it, about 10% of all commercial originations are through brokers, so it’s absolute greenfields,” he said.

Bannister said any change in funding commercial had yet to occur. Commercial investors could navigate market gyrations a little more easily and were less sensitive to rate changes. “One, because the asset profile is generally tuned to inflation itself, so when rates go up, generally rents go up. We’re seeing it in commercial at the moment. In fact, stats already show an acceleration of rents in that space.”

In terms of Sydney industrial assets, Bannister said rents were up 30% year-on-year and vacancy rates down to 0.3%. “There’s a huge demand for commercial properties, and we’re not seeing that change any time soon.”

When it came to SMSFs, he said there were opportunities in commercial, where landlords facing higher interest rates were thinking of selling, while tenants were sick of rents going up and wanted to buy the property but didn’t have the capital.

“SMSF’s a good vehicle where they’ve got that capital available,” Bannister said. “It’s not subject to the living expenses, inflationary pressures on your balance sheet. That’s a really cool and neat way that people can get into commercial property.”

He said investment lending had potential for growth next year too, because with property values coming back, investors read that as values coming back to the marketplace. “It’s not my house values going down; it’s always value coming back. Prices come back 15% to 20%. Investors see value coming back, rents are going through the roof, vacancies are low, and whilst borders are open, we haven’t seen migration levels normalise yet.”

Sampson said interest rates had gone up, inflation was high, the community was nervous, and “they probably will continue to be, but what a great opportunity for brokers”.

“My guys are at a lot of commercial PD days and seeing a lot more resi brokers wanting to learn about commercial,” he said. “The commercial lending space will continue to grow. About 28% of brokers wrote one commercial loan last year.”

As residential lending slowed down, he saw a great opportunity for brokers to diversify into commercial.

“We’re not banks; we’re not going through masses and masses of paperwork. You don’t have to be a financial analyst to do a commercial loan,” said Sampson.

“You can step into commercial lending with these less complicated loans, and then when your confidence grows, get involved in more complicated deals. Again, it’s a solution. You know, most of those around this table are here to provide solutions for clients.”