Rate rises and landmark negative gearing reforms are transforming how brokers approach refinancing conversations with clients - here's what the experts have to say

Australia's refinancing market is navigating one of its most consequential periods of structural change in years. The Albanese government's landmark May 2026 Federal Budget – which abolished negative gearing on established residential properties purchased after 12 May – is reshaping lender policy, compressing borrowing capacity and significantly expanding the complexity of broker workloads all at once, while prompting many investors to reassess existing lending structures and refinance strategies.

Meanwhile, the Reserve Bank of Australia has pushed through three interest rate rises this year – a worrying development for borrowers rolling off fixed-term contracts.

These head-spinning developments are having a profound impact on refinancing activity.

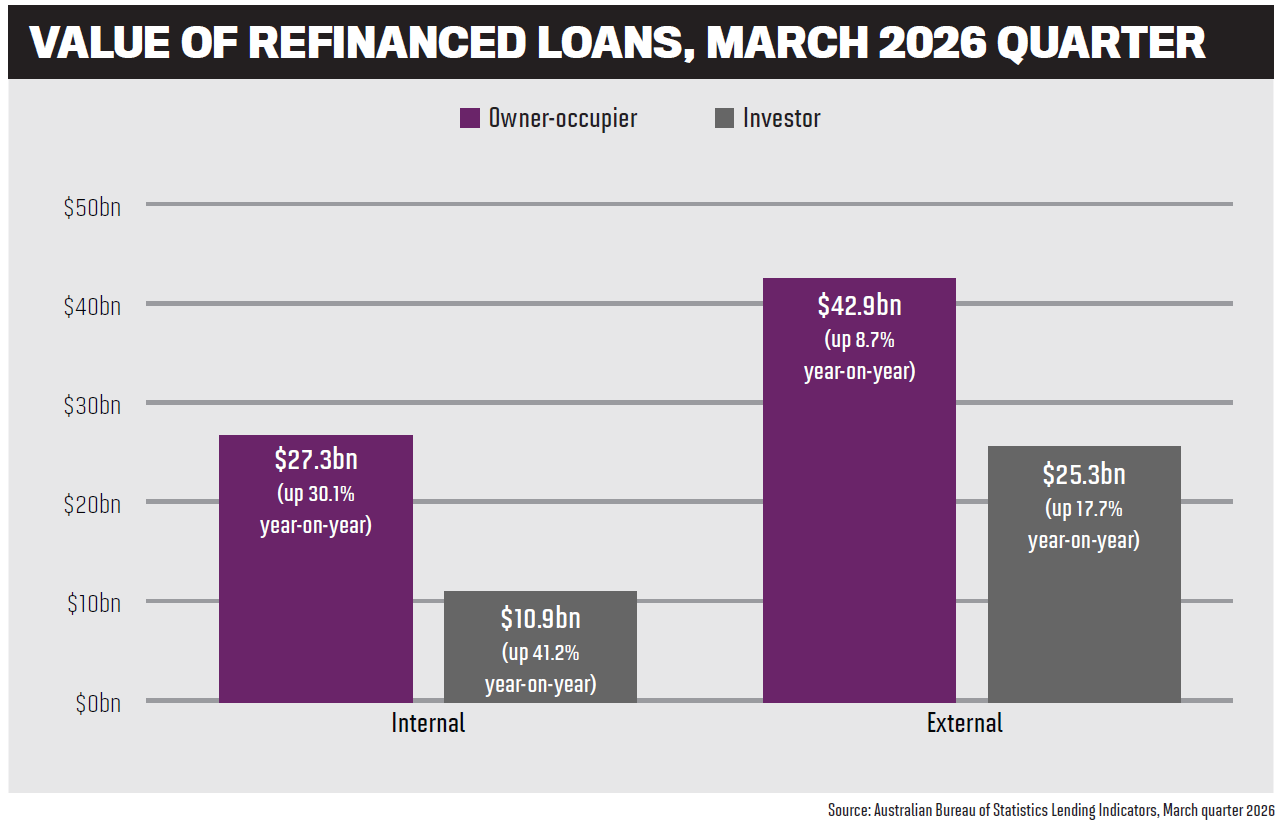

According to ING data, refinancing has risen from 47% to 50% of total broker lodgements since the Reserve Bank's 2026 rate hikes, reflecting continued refinancing demand even as the broader market softens from 2025's heady highs.

"While investor purchase demand is expected to soften, refinance activity may partially offset this decline, as brokers look to reposition existing portfolios in response to the changes," says ING national sales manager, retail broker channel, Sergio Delvescovo (pictured, right). However, he notes that "increased competition for investor refinance flows introduces a risk of margin compression in an otherwise high-return segment".

With analysts forecasting a potential further rate rise in the September quarter, ING expects refinancing to stabilise at approximately 50–52% of total lodgements – around six percentage points above pre-hike levels.

Each incremental rate rise, Delvescovo says, has had a more pronounced impact on household budgets, making them "highly stimulatory to refinance activity".

He details a twofold effect of the tightening cycle: it "stimulates refinance through increased borrower price sensitivity", but it also "suppresses purchase demand via serviceability constraints".

Together, "these dynamics increase the relative importance of refinance, making it a critical battleground for banks with ongoing pressure on margins".

Ian Rakhit (pictured, left), general manager third party at Bankwest, notes that customers are more engaged with their finances and more willing to review their current lending arrangements amid this higher-rate environment.

As more customers review their lending arrangements, the opportunity for brokers lies in both helping new customers and proactively supporting existing customers. "Refinance conversations are no longer just about rate," says Rakhit. "Customers are looking for certainty, flexibility and confidence in their loan structure. Brokers play an increasingly important role helping customers navigate their options. This places a greater focus on retention and proactively engaging existing customers in a meaningful way."

Baber Zaka (pictured, centre), general manager of third party banking at Commonwealth Bank, agrees. "Refinancing today isn't just about chasing the lowest rate. It's about getting the right structure for each customer's circumstances and making informed decisions with confidence," he says.

"Reliability and consistency are critical to giving brokers and their customers greater clarity throughout the process. That means setting clear expectations, providing dependable support and ensuring applications are assessed in a practical and timely way so brokers can progress applications effectively."

Zaka stresses the importance of speed, "particularly when a broker is managing an urgent refinance. In those situations, our priority is to work closely with the broker to understand the customer's circumstances, identify what is time-sensitive and help progress the application as efficiently as possible."

Higher rates have kept refinancing conversations "very active" at Nectar Mortgages, says head licensee and finance specialist Justine Harris.

Clients have become more aware of their repayments, their cash flow and their loan structure, with the conversation shifting from "can I get a lower rate?" to "can I afford to keep doing what I am doing?"

Harris sees that as an important shift. Echoing Rakhit's comments, she says "refinancing is no longer just a rate conversation. It's now about cash flow, loan term, lender policy, future plans and whether the current loan still suits the client's life. For brokers, that creates more work, but it also creates a stronger reason for clients to seek proper guidance."

Refi market in post-Budget flux

Following the Federal Budget, many lenders moved to update their negative gearing policies, despite the legislation not yet being codified into law.

As for ING, Delvescovo says the bank is "closely reviewing how the changes flow through to serviceability, with a focus of giving brokers greater clarity across different investor scenarios as the policy evolves". As part of this, ING is updating its serviceability treatment to reflect the Budget changes, with no change to existing properties purchased on or before 12 May 2026 or eligible newly constructed properties. For established investment properties purchased after this date, negative gearing benefits will be limited to rental income for serviceability purposes.

"As brokers work through the transition, the focus is on making it clear how different application scenarios are assessed, particularly where existing and new lending may be treated differently," adds Delvescovo.

The borrowing capacity implications of the Budget are material. Early indications from one bank's new serviceability calculator suggest that Labor's negative gearing changes could reduce investor borrowing capacity by between 8% and 12%, according to Troy Phillips, managing partner at FirstPoint Mortgage Brokers, based in Cronulla, NSW.

On a $1 million mortgage, that translates to a potential reduction of up to $120,000 in eligible borrowing. These estimates imply a borrower on a higher marginal tax rate, and Phillips suggests it could be less for borrowers on a lower marginal tax rate. This is likely to see brokers lean more heavily on refinance strategies to help customers optimise existing positions in a changing policy environment.

Harris predicts a splintering of the refinancing market if these Budget measures are codified into law.

Refinancing activity should remain strong for owner-occupiers as they continue to search for better rates, better structure or more certainty.

But for investors, "it becomes more complex". Some clients, says Harris, "may want to refinance to protect their current position, tidy up their structure or avoid being caught by future policy changes. Others may hold off because they are unsure whether to buy, sell, restructure or wait."

Regardless of the direction, "I don't think this reduces the need for brokers," continues Harris. "I think it increases the need for good broker support. The challenge is that the work becomes more advice-led, more scenario-based and more time-consuming."

Speed, reliability and the broker relationship

As each week seems to bring a fresh wave of macroeconomic uncertainty, speed and certainty have never been more important.

ING has made tangible progress on the speed front for refinances.

Following its transition to MSA National as its settlement provider, Delvescovo says ING has more than halved settlement times to around 10 days, supported by a more automated, streamlined process. The bank is now building on this with AI-driven document handling and income verification, a new credit-decision model and enhancements to valuations aimed at delivering a faster and more consistent end-to-end experience for brokers and their customers.

Rakhit says Bankwest's ambition is to improve speed and consistency across the entire refinance journey – and that achieving it requires more than technology investment alone.

"Brokers consistently tell us consistency and ease of doing business matter to them and their clients," Rakhit says. "That comes down to the value we deliver beyond pricing."

Bankwest is working towards delivering unconditional approval within 24 hours for straightforward deals, underpinned by continued investment in the Broker Portal and dedicated support teams.

But Rakhit is clear that digital efficiency and human support are not competing priorities; they are complementary ones. "While we are utilising digital solutions to make simple work faster, people remain essential for time-sensitive or complex situations," he says. "Brokers can access that support when needed."

Bankwest is also trialling broker notifications when a discharge request is received, "creating an opportunity for brokers to reconnect with their customers".

Looking forward

Rakhit expects to see greater demand for broker guidance if the Reserve Bank of Australia (RBA) decides to move rates higher as 2026 progresses. "Any period of uncertainty tends to drive demand for advice, which presents an opportunity for brokers," he says.

Since rate changes tend to introduce an increased focus on existing lending arrangements, brokers will be fundamental in letting customers understand what their options are. "We would expect a continued demand for refinancing and retention conversations," says Rakhit.

In the meantime, Harris is making sure her clients don't panic.

"As brokers, our role is to explain what has changed, what has not changed, what the lender is currently doing and what the client needs to consider next," she says. "This is where good brokers are incredibly valuable. We are not here just to lodge loans; we are here to help clients make calm, informed decisions in a market that feels uncertain."