How the non-banks are attempting to fill the void left by the majors, while continuing to deliver on brokers’ expectations

.jpg)

How the non-banks are attempting to fill the void left behind by the majors, while continuing to deliver on brokers' and customers' diverse needs

Q: Have you seen an uplift in business as a result of the increased scrutiny of the major banks, and how is that playing out?

As traditional lenders continue to tighten their lending criteria, customers are finding themselves underserved at a time when they need banks the most, according to Mario Rehayem, Pepper’s Australia CEO.

“Market conditions today mirror those when the near prime category was first launched to accommodate demand for loans that traditional banks were unable to provide at effective rates,” he says.

Pepper says it pioneered the near prime product in 2012 and has since seen it grow exponentially.

In Pepper’s view, the ‘near prime’ borrower is defined as someone with one too many credit cards that they are finding difficult to repay, or who may be working in the gig economy and not hold standard fulltime employment or have supplementary income; they may have just changed jobs or may want to consolidate their debts; or they may have overcome a credit event and just want to move forward.

“This is real-life lending we’re talking about,” Rehayem says. “Many of these customers are on the cusp of prime and would have been willingly financed by a bank only 12 months ago.”

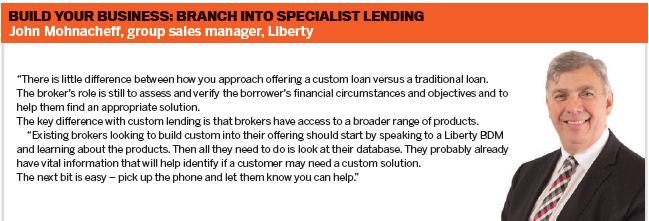

John Mohnacheff, group sales manager at Liberty, says the non-bank has also experienced consistent and sustained lending growth across the board, though he doesn’t go so far as to describe it as a ‘surge’.

What has happened is the non-banks have become more relevant “because we are the ones that are bringing opportunity to the broker market”.

“We’ve always been there, and the brokers are going to start to realise, ‘I can no longer keep dumping everything on the majors’. That is always a very easy fallback position [but] the offerings from the non-banks are now more attractive and relevant,” he says.

“We are a viable alternative and sustainable contender.”

Homeloans Group

While it’s too early to know what the impact will be of some lenders – such as CBA and Bank of Queensland – pulling out of low-doc lending, Homeloans general manager of third party distribution Daniel Carde says, “We are well placed to take on the volume if need be”.

“We have certainly seen an uplift in volumes [generally] in the last quarter of FY18, which we attribute to Homeloans’ competitive product range and expanded sales team,” he says.

Not only has the lender seen a steady increase in specialist and investor borrowers, but interestingly, it’s also received more prime customers.

“We generally find that, as brokers use our products for one type of borrower, it opens them to the rest of our product range, resulting in an increase in volume across the board,” Carde says.

“While the near prime borrower demographic has always existed, it’s becoming more pronounced and prominent in the current lending landscape,” says Royden D’Vaz, head of sales and marketing at Bluestone.

There’s now a large segment of customers who make their repayments on time and don’t have any defaults or arrears, but they may have a tax debt or be in shortterm employment or relying on workers’ compensation, and this pushes them outside the banks’ narrow lending criteria.

“Talk to any broker and they’ll say two months ago this was a deal every day, and now it’s falling outside what the banks will accept,” he says.

“Credit scoring has a lot to do with it. Where in the past if a credit score spat out a ‘no’, a human underwriter would still be able to assess it and make a decision, now they’re not allowed to do that.”

Near prime customers are deemed less ‘risky’ than a non-conforming or specialist borrower.

“They don’t deserve to pay the higher rates of someone who has defaulted or not paid their mortgage,” D’Vaz says.

Q: With this increase in business, how are you ensuring that service, turnaround time and consistency aren’t affected?

Bluestone

Brokers are all too familiar with service levels blowing out when lenders announce a new rate or campaign deal. Lenders often find themselves inundated with new applications and ill-equipped to deal with them.

“We wanted to make sure that didn’t happen,” says D’Vaz.

With the sale of Bluestone Asia Pacific to Cerberus Capital Management, the non-bank has been able to sharpen its rates and move into the near prime space, attracting a lot of attention from the broker market. While doing so, it proactively started growing its team to deal with the anticipated rise in new business.

“We’ve increased our back-end credit team, underwriters and support staff,” D’Vaz says. The lender has also doubled its sales team.

With each BDM now backed by a dedicated support team, they can focus on getting out on the road to meet brokers face-to-face and help them package near prime deals.

And it’s a good thing the non-bank took that step – more than 250 brokers have become accredited with Bluestone in the last two months, and the business has almost tripled its volume in the past year, D’Vaz says.

Liberty

The major banks used to be the most convenient option for brokers, but now that’s changing and brokers are being forced to adjust their habits and look elsewhere, says Mohnacheff.

“Where we are unique is we have got a lot of human beings out there to help the brokers, externally and internally,” he says. “As we’ve grown, we’ve brought on new underwriters, BDMs and support staff to ensure brokers continue getting the best service and turnaround times.”

Liberty now has more than 60 BDMs across all its asset classes. It also gives brokers direct access to its underwriters so they understand how and why they came to a decision.

“Whether you turn it around in 12, 16 or 24 hours, is that the critical thing?” Mohnache asks. “Or is the critical thing about educating brokers that there is a viable alternative?”

“Our efforts are not, ‘Are we going to be cheaper or faster?’ No, we are more caring, we’re here for you, and we’ll help you build that deal. At the end of the day, that’s what really matters.”

Pepper

Despite the uplift in business, Rehayem says Pepper is continuing to offer a 24-hour turnaround for approvals.

“Seeing conditions change about nine months ago, experience told us we needed to react quickly,” he says. “We upskilled existing staff and hired more people, ensuring we had a robust and compliant onboarding process so more of our ‘can do’ people could manage that uptick in business from day one.”

Homeloans

Carde admits that while Homeloans’ turnaround times have been impacted as a result of increased volume, the lender is addressing the issue in a number of ways.

That includes investing in its team to provide them with additional resourcing, and looking at how technology can assist in providing efficiencies.

“A number of process changes have already delivered some early improvements, and once our resourcing is appropriately balanced and the technology solutions are delivered we know we will be well placed to handle these types of unforeseen volume increases in the future.”

.jpg)

Q: How should brokers handle this question from borrowers: ‘Why can non-banks approve this deal when it was rejected by a major bank?’

Homeloans

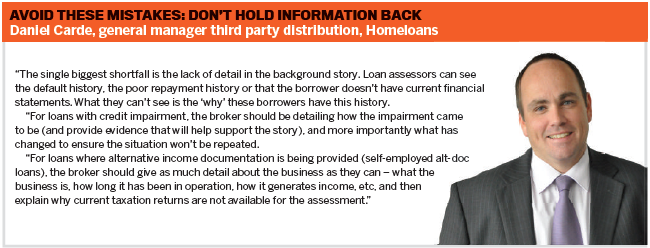

The best way to approach this is to explain that a specialist lender often caters to a much broader market than a traditional bank, as is the case with Homeloans.

“Specialist lending is really no different to traditional prime lending in terms of the basics. Loans must still pass suitability and serviceability tests. The major difference between prime and specialist is that specialist generally requires a more detailed background story to help the loan assessor in understanding the borrower’s position,” Carde explains.

In order to make a decision, the assessor will need to know why the borrower is in the situation they are in, and what has changed to show that they won’t be in that situation again with the new loan. “The only way to do this is to provide as much background detail as possible and demonstrate that the borrower is well positioned to meet the obligations of this new loan going forward.”

Pepper

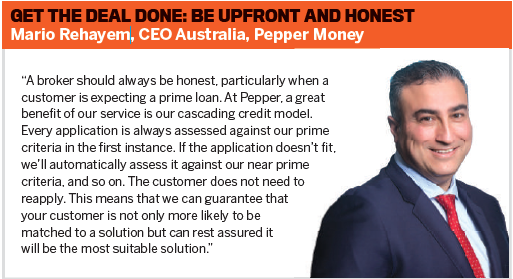

Put simply, “we can offer a solution when the banks can’t”, Rehayem says.

When recommending a non-bank loan, a broker should explain why the borrower is not eligible for a bank loan, and clearly demonstrate how a product from a non-bank matches their needs. A broker should also explain how a non-bank is different to a mainstream bank.

“Generally the only difference is that they are not an authorised deposit-taking institution (ie they don’t take deposits) and for this reason are regulated by ASIC instead of APRA. Just like the banks, non-banks must comply with responsible lending laws as set out in the National Consumer Credit Protection Act.”

At a non-bank, funding for home loans comes entirely from the wholesale money market, whereas banks rely on a mix of deposits and wholesale funding.

Bluestone

Borrowers might not immediately embrace the fact that they’ve fallen outside of the traditional lending parameters, but it’s important for them to know that this is not the broker’s fault and there are still options available to them.

D’Vaz says brokers should explain to customers why their circumstances have made them candidates for a non-bank loan instead, and should emphasise the cost of the repayments rather than dwelling on the rate difference. “

The onus is on brokers to position it as, ‘Yes, your circumstances have set you apart, but the difference in repayments is only X amount’. That should be the type of conversation they’re having.”

Liberty

“Being able to approve deals that banks can’t isn’t new to us. For 21 years we’ve operated to help as many customers as we can, and have always looked at an applicant’s full story when assessing their eligibility for a loan. That’s how we find more ways to get to ‘yes’,” Mohnacheff says.

He vehemently refutes the term ‘shadow banking’ to describe the non-bank sector.

“The media jumped on this term of shadow bank. But a shadow bank is something dodgy out of the Bahamas, or an unlisted entity somewhere in Switzerland or the Cayman Islands; they’re shadow banks. We are an Australian company – proud, true, and reputable.”

“The broker’s job is not to feed the big banks but to find the appropriate product for their consumers when they need it,” he says.

Q: How is your company dealing with increased funding costs, and do you expect to see a credit crunch in the wake of the royal commission?

Liberty

Markets by their nature fluctuate, and all lenders’ funding costs reflect those changes, Mohnacheff says. “It’s also true that recently there has been increased volatility and higher interest rates for all lenders in debt markets. In contrast, customers’ interest rates are relatively constant because they are set at the time loans are drawn down and updated infrequently.”

The royal commission, however, “will not in any way, shape or form create a credit environment”, he says.

“A credit crunch will come if capital markets close. If access to capital changes, that’s a credit crunch, like during the GFC. Credit assessment criteria might change because of that, but will it become a credit crunch? I doubt it,” Mohnacheff says.

“There is a lot of liquidity; there is a lot of capital around. Just because the banks have to vary it doesn’t mean others do; there are a lot of alternatives for funding arrangements in Australia and New Zealand, and we are one of the leading ones.”

Bluestone

“I think all the mainstream lenders are feeling the pinch right now because there’s a heightened spotlight at the moment, but who can predict what will happen in 12 months’ time?” D’Vaz says.

What he does know is that the current environment has provided a fantastic opportunity for non-banks to cater to clients that the big banks have turned away.

“It’s also an opportunity for brokers to deliver good customer outcomes and help more customers, more often. Instead of having these customers get locked into higher-rate loans, near prime gives them another option.” With specialist borrowers, lenders add an extra margin to the interest rate to deal with the higher risk of taking them on, but that’s not required with near prime borrowers.

Funding costs have risen, but credit is not constrained, he says. Doors are still open for borrowers; they just might be different ones.

Homeloans

“I wouldn’t go as far as to say that out-of-cycle interest rate movements will be a regular occurrence; however, it would certainly be safe to say that home loan interest rates, and any changes to those rates, are no longer directly linked to the official cash rate,” Carde says.

“Out-of-cycle rate movements are not new – we have seen them from almost all lenders over the past few years as changes in the global funding markets, coupled with higher regulatory compliance costs, impact the overall cost of funds for lenders.”

Homeloans’ treasury team is constantly monitoring and responding to changes in the market, ensuring it’s balancing the needs of the business and the interests of borrowers, he adds.

While Carde doesn’t expect a credit crunch, he does anticipate that there will be “more refinement” of credit policy and processes as lenders review their approaches to responsible lending.

Pepper

Rehayem says that while Pepper isn’t immune to these market conditions either, its strong reputation in the wholesale funding markets means it’s able to diversify its funding sources in a way that delivers a more efficient cost of funds.

“This allows us to offer a broker’s customer competitively priced interest rates regardless of the environment,” he says.

“Put simply, Pepper offers a more personalised service, with a human assessing each individual application rather than an anonymous decision-engine-based scoring system used by the big banks. Because we manually assess applications, we can truly understand a customer’s situation and offer a solution that is tailored to their circumstances.”