Individual filers by far the largest contributors to coffers, followed by super funds and companies

Newly released Australian Taxation Office (ATO) data reveals the scope of capital gains tax (CGT) paid by Australian individuals, companies and super funds, at a time when the government seeks to push through legislation to increase the annual haul even further.

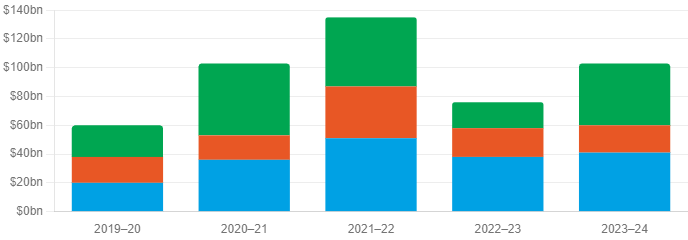

Capital gains made

Individuals alone reported $40.6 billion in net capital gains in the 2023-24 tax year — up from $37.8 billion the previous year, driven overwhelmingly by the residential and investment property market.

The top two brackets drove the bulk of the total. The $100,000–$999,999 range contributed over $15 billion from nearly 69,000 filers, while the $1 million-or-more bracket added $14 billion from less than 4,000 individuals. Real estate was the single largest source, underpinning the majority of individual capital gains.

Super funds posted the most dramatic turnaround of any entity type in 2023–24, recording $43 billion in net capital gains — a 144% surge from $18 billion in 2022–23, which had been the weakest result in the five-year dataset. The rebound reflects the strong recovery in listed equities and managed trusts, asset classes that dominate SMSF and institutional fund portfolios and that were heavily impacted by the 2022 market downturn.

Companies was the only entity type to record a decline in net capital gains in 2023–24, slipping 4% to $19 billion from $20 billion the prior year. The result continues a downward trend from the 2021–22 peak of $36 billion, which was inflated by elevated corporate asset disposals during the post-pandemic period. Unlike individuals and super funds, companies are not eligible for the CGT discount, making their gains directly taxable at the applicable corporate rate of 25–30%.

The $1 million-or-more bracket accounted for $14 billion — around 75% — of all taxable company gains, concentrated among just 1,600 large entities. A further $2 billion in gains was reported by non-taxable companies, generating no CGT revenue.

Across all three entity types, total net capital gains in 2023–24 reached $102 billion — a 37% recovery from 2022–23's $75 billion and a return to the $100 billion-plus territory last seen in 2020–21. The combined figure remains below the all-time five-year peak of $135 billion recorded in 2021–22, when an exceptional convergence of buoyant property prices, elevated company activity, and strong equity markets aligned across all three segments simultaneously.

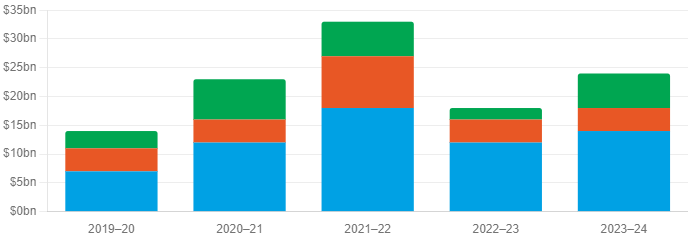

Capital gains tax paid

Individual taxpayers paid an estimated $14 billion in CGT in 2023–24 — up 15% from $12 billion in 2022–23, and notably growing at twice the rate of the underlying gain increase of 8%.

This divergence indicates a compositional shift toward gains in higher tax brackets. The top gain tier ($1 million or more) generated $6 billion in CGT from just 3,600 individuals — representing 43% of the total individual CGT bill from fewer than 0.4% of filers. Individuals remain by far the largest CGT contributor, accounting for 58% of total estimated CGT across all entities.

Super funds paid an estimated $6 billion in CGT in 2023–24 — a 160% increase from the $2 billion recorded in 2022–23, directly tracking the dramatic rebound in fund-level gains. Despite generating $43 billion in gains, funds paid only $6 billion in CGT, reflecting the concessional tax treatment applied to complying funds: a 15% rate with a one-third discount available on assets held for more than 12 months, resulting in an effective rate of approximately 10%.

Companies paid an estimated $4 billion in CGT in 2023–24, broadly flat on the prior year's $4 billion despite a marginal decline in gains.

Total estimated CGT paid across all entities in 2023–24 was $24 billion — a 30% increase on 2022–23's $19 billion and a meaningful recovery toward the five-year peak of $33 billion set in 2021–22. The $24 billion figure represents approximately 3.8% of the ATO's total tax revenue of $631 billion in 2023–24. Individuals drove 58% of the total, super funds 23%, and companies 18% — a distribution that reflects both the scale of each sector's gains and the significant differences in effective CGT rates across entity types.

How the Budget changes the game

Just weeks before this data was published, the Albanese government's Federal Budget contained the most significant overhaul of CGT settings in more than a quarter of a century — followed swiftly by a partial retreat that has left the industry digesting a policy landscape still very much in flux.

The centrepiece CGT measure scraps the existing 50% discount — introduced by the Howard government in 1999 — and replaces it with inflation-adjusted cost-base indexation from 1 July 2027. A minimum 30% tax rate on realised capital gains will apply concurrently.

The combined CGT and negative gearing reforms are expected to raise $3.6 billion over four years, per government data, and roughly $8.1 billion when combined with discretionary trust taxation changes. The New South Wales state treasury estimated the broader CGT discount — which the government did not fully scrap — has cost the federal budget approximately $23 billion annually in foregone revenue in recent years.

The Budget landed to an immediate firestorm. Labor had pledged before the 2025 federal election not to change CGT or negative gearing settings, making the announcement a lightning rod for accusations of broken promises. Opposition leader Angus Taylor condemned the measures as "toxic taxes" while Pauline Hanson's One Nation Party launched a 'Fire the Liar' campaign across social media, television, and radio.

The broking industry was among the most vocal opponents. The Mortgage and Finance Association of Australia (MFAA) made submissions to the Senate Economics Legislation Committee's inquiry, while COSBOA — the Council of Small Business Organisations Australia — launched its 'Fair Go' campaign warning the reforms "risk undermining the entrepreneurial foundations of the Australian economy." A Freshwater Strategy poll taken shortly after the Budget found 45% of respondents said the proposed changes had decreased their trust in the government.

The U-turn: small business threshold lifted

Facing mounting pressure, prime minister Anthony Albanese announced on 18 June that the CGT concession threshold for small businesses would be lifted fivefold — from $2 million to $10 million in annual turnover.

Treasurer Chalmers denied it was a backflip, describing it as "the outcome of the consultation that we flagged in the Budget papers themselves."

The revised threshold means that the overwhelming majority of Australian mortgage brokerages — which almost universally operate below $10 million in annual revenue — are now shielded from the CGT discount changes on the sale of their business.

The government also confirmed that income from all types of testamentary trusts — trusts established for genuine succession and estate planning purposes — will be exempt from the minimum tax, with implementation details subject to further consultation.