Cookie-cutter lending no longer works – and banks must adapt accordingly, says head of third party lending Baber Zaka

We all know that two borrowers rarely tell the same story. A nurse buying her first home with a 5% deposit has drastically different needs to a self-employed tradie without standardised income. A family refinancing after one income earner took parental leave needs an entirely different support system to a retiree exploring equity release.

It's because of these diverse needs of the modern Australian borrower that obtaining a home loan can sometimes feel like cramming a square peg into a round hole.

CommBank is tackling this problem head-on with its new broker value campaign under the no-nonsense banner: "When life looks different, lending should too."

This proposition reflects the reality that more customers are approaching brokers with complex or non-standard scenarios that require a tailored approach. Whether it's income drawn from multiple sources, atypical savings patterns or unique purchasing arrangements that fall outside the norm, "brokers consistently tell us they value the breadth and flexibility of our policies, the depth of credit expertise, and our practical, common-sense approach to lending", says Baber Zaka (pictured), CommBank's general manager, third party banking.

"This feedback gave us the confidence to lean into what we're ultimately known for – supporting applications that don't fit the standard mould, and recognising that as customers' lives evolve, lending needs to evolve with them."

CommBank is deliberately targeting complex scenarios with its latest broker campaign, which Zaka concedes is not a cut-and-dried concept.

“Brokers consistently tell us they value the breadth and flexibility of our policies, the depth of credit expertise, and our practical, common-sense approach to lending” - Baber Zaka, CommBank

"There isn't a single definition of a complex borrower," says Zaka. "It reflects a range of customer scenarios that fall outside a straightforward application. This can include multiple or non-standard income streams, more sophisticated asset or ownership structures, or customers requiring tailored loan structuring or policy layering to meet their needs."

Investor lending

Rather than assessing each transaction in isolation, Zaka reckons brokers must take a portfolio-led view of a customer's broader investment strategy. "We support brokers to deliver strategic lending outcomes, with a focus on getting the structure right, supporting portfolio sustainability and ensuring long-term suitability for the customer, not just the immediate purchase," he says.

Serviceability remains one of the biggest hurdles in getting an application over the line, while investors' needs are becoming more sophisticated and nuanced.

Zaka sees this complexity not just as a challenge but as a genuine opening for the well-prepared broker. "Brokers who take a more strategic, portfolio-led approach are better placed to deliver strong outcomes for their clients."

Refinancing

Refinancing is becoming more "deliberate and strategic", says Zaka, as clients "focus on preserving borrowing capacity, accessing equity efficiently and structuring for long-term sustainability in a higher-rate environment". This is putting brokers in a more demanding position.

One of the biggest challenges for brokers is balancing tighter serviceability settings with the need to deliver competitive, well-structured outcomes for clients. To support this, CommBank offers an alternative refinance assessment process, including a reduced serviceability buffer for eligible customers.

The bank recognises a broader range of income sources such as boarder income, and takes "a considered approach to commitments such as HECS, helping brokers better reflect a customer's true position".

Property valuation tool CommVal also gives brokers upfront visibility on property value, equity and borrowing capacity, "supporting more informed and confident decision-making".

Self-employed borrowers

When life looks different, lending should too – and nowhere is this more evident than in the self-employed space.

"Self-employed borrowers are often underserved because traditional lending models are built around consistent, PAYG-style income," explains Zaka. By contrast, business income comes with more variables, tends to be structured in different ways and is highly influenced by timing, reinvestment and broader commercial decisions, "making it harder to assess through a single, standard approach".

CommBank's answer is to provide a diversity of pathways to getting the best outcome for customers. "We offer multiple income assessment options, allowing brokers to align the right method to each customer's circumstances," says Zaka. This can include using the most recent financials where appropriate, supporting customers with shorter trading histories and providing alternative assessment options for eligible scenarios.

The bank also takes "a more practical view of business structures and changes over time, recognising that how a customer operates may evolve", Zaka adds.

No two brokers are the same either

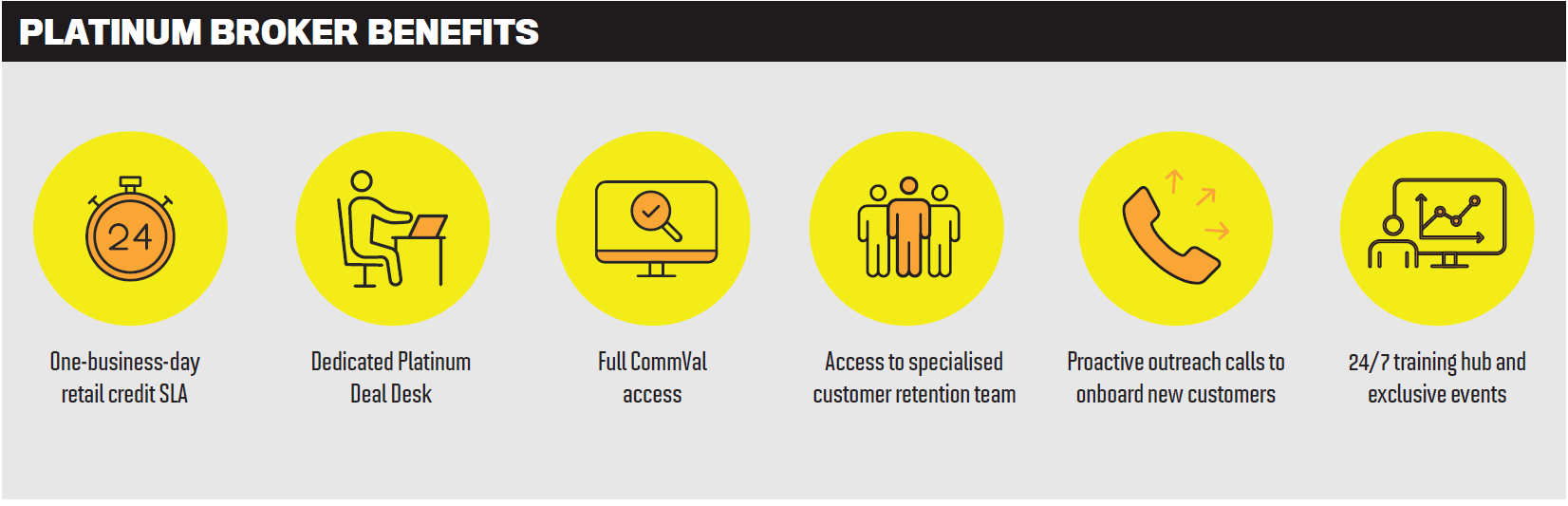

Just as every customer brings different needs to a transaction, so too does every broker. A single support model cannot serve a sole operator and a high-volume brokerage in the same way – and CommBank's Platinum Broker program reflects that thinking.

The program is built around brokers who regularly work on complex scenarios, offering faster access, greater certainty and more direct lines into the bank. A one-business-day retail credit SLA and a dedicated Platinum Deal Desk give brokers "the ability to workshop and progress complex scenarios with greater speed and confidence", Zaka explains.

Upfront property valuation tools, proactive onboarding calls to support new customers, access to specialised retention services, and 24/7 training resources all form part of the offering. For Zaka, these aren't add-ons; they are the infrastructure that lets brokers stay across a client's position well beyond settlement.

"We help brokers stay connected and continue adding value well after settlement," he says, "building long-term trust and confidence so customers feel supported not just in the decision they've made today but across the life of their loan."

That shift – from transaction to relationship – is something Zaka sees playing out across the broker channel more broadly. Brokers are no longer simply facilitating a loan. They are guiding clients through refinancing decisions, life changes and evolving financial needs.

"At CommBank, we see our role as backing brokers throughout that ongoing relationship, not just at the point of application or settlement," he says. "That means giving them the tools, insights and support to stay relevant as their customers' needs evolve, whether it's refinancing, purchasing again or reshaping their lending over time."

Applications for credit are subject to credit approval, satisfactory security and minimum deposit requirements. Conditions apply to all loan options. Full terms and conditions will be set out in the loan offer if an offer is made.