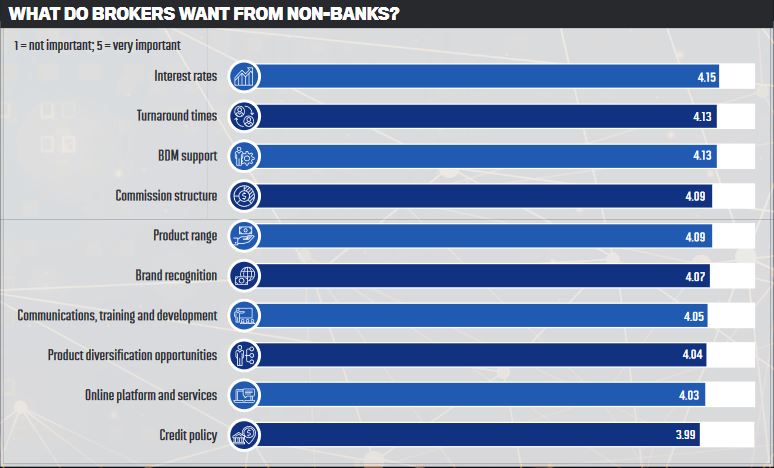

Brokers give their views on how the non-banks have fared in areas like turnaround times, interest rates, BDM support, and online platforms and services

This year has been one like no other, so it’s no surprise that the results in this survey differ so much from last year’s. Broker priorities have changed drastically for starters. Turnaround times and interest rates remain in the top positions, albeit swapped around since last year, but BDM support in joint second place has jumped from bottom of the pile.

In 2019, BDM support scored 3.50, much lower than the score of the second lowest priority on the list. But this year, this support has been crucial. Brokers have needed BDMs to help them keep up with changing appetites and policies as interest rates have moved around and borrowers look for guidance in what has been a challenging year for everyone.

It is great news then that last year’s gold medallist in this category maintained its position. As brokers required this support even more, this non-bank was there.

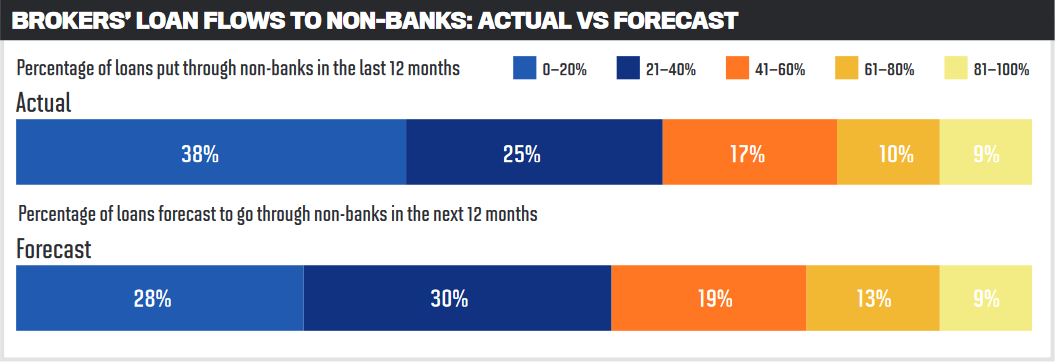

According to the MFAA’s quarterly Industry Intelligence Service research, brokers’ use of non-bank lenders has fallen in the last few quarters. The proportion of loans sent to non-banks is at its lowest level since the March 2018 quarter.

This trend looks set to continue as figures coming out of the coronavirus pandemic show new loans and refinances in 2020 are predominantly going to the major banks. Research from the NSW Land Registry in September showed that the major banks accounted for more than two thirds of all refinances in August.

In this survey, MPA asked brokers whether they had sent more loans to non-banks this year compared to the previous year. While 65% still said they had, this was a drop from 76% last year. The survey also asked brokers what the reasons were for picking a non-bank lender, and what were the barriers to using one – see those results on the following pages.

As in the last two years, the 2020 survey also asked brokers to rate their top non-bank lenders in different sectors of the market, like specialist lending, first home buyers, SMSF loans and foreign non-residents. The results showed some changes to the ranking of the non-banks, which is unsurprising given the shifts in lender appetite that the industry has seen.

Why use a non-bank

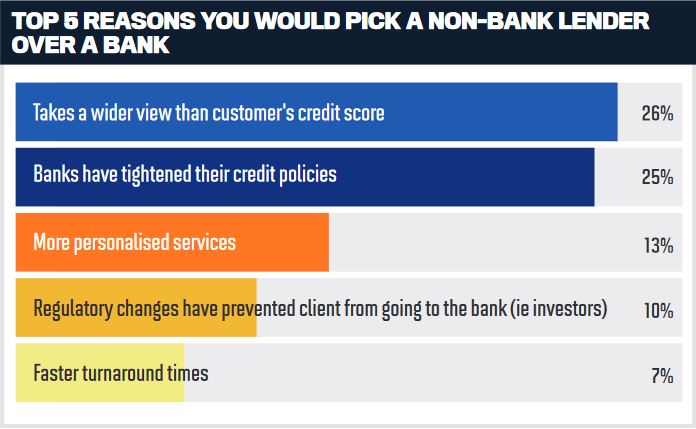

The top reason for picking a non-bank lender over a bank remains the same, as brokers look for broader views on their customers’ borrowing capacity

In a year when Australians have had their working hours reduced, or been furloughed from their jobs, or lost them completely, brokers have been working harder than ever to help their clients get by. For some borrowers this has meant repayment deferrals, and for others refinancing. But with government schemes and financial help, many younger Australians have even taken the opportunity to buy their first home.

In a year when Australians have had their working hours reduced, or been furloughed from their jobs, or lost them completely, brokers have been working harder than ever to help their clients get by. For some borrowers this has meant repayment deferrals, and for others refinancing. But with government schemes and financial help, many younger Australians have even taken the opportunity to buy their first home.

Unfortunately, however, 2020 seems to have had a troubling impact on non-bank lenders. While the majority of brokers are still sending more loans to non-banks than ever before, these dropped 7% from last year.

This does not necessarily mean brokers are sending fewer loans to non-banks, but based on other figures in the survey, it looks like they are planning to send fewer loans in the future.

The proportion of loans sent to non-banks over the past 12 months remained fairly similar to the year before, except for an increase of 5% in brokers who sent 20–40% of their business to non-banks. This meant there was a drop in the number of brokers sending 40–60% of loans to non-banks.

In terms of the proportion of loans brokers expect to send to non-banks in the next 12 months, the results showed that they plan to send slightly more to non-banks, but not as much as they predicted last year.In 2019’s survey, over 10% of brokers forecast sending 81–100% of loans to non-banks, 16% forecast sending 61–80% and almost 24% expected to send 41–60%.

In terms of the proportion of loans brokers expect to send to non-banks in the next 12 months, the results showed that they plan to send slightly more to non-banks, but not as much as they predicted last year.In 2019’s survey, over 10% of brokers forecast sending 81–100% of loans to non-banks, 16% forecast sending 61–80% and almost 24% expected to send 41–60%.

The reasons brokers would choose to use a non-bank over a bank shifted slightly compared to last year. Moving up from the second-highest reason in 2019, this year brokers said they would choose non-banks because they take a wider view of clients’ credit scores. Brokers are dealing less this year with regulatory changes and more with the changing situations of borrowers.

Turnaround times also featured in the list of reasons for using a non-bank, replacing the need for alternative documentation.

Product and pricing

The barriers to sending loans to non-bank lenders remain similar to last year, with higher rates and fees being the biggest problem for brokers

The barriers to sending loans to non-bank lenders remain similar to last year, with higher rates and fees being the biggest problem for brokers

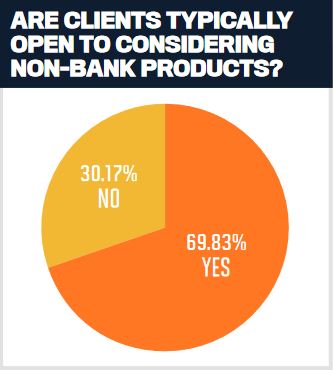

While it can be argued that more borrowers are needing to turn to non-bank lenders in 2020 as the way they work changes and credit appetites of the banks shift, the proportion of brokers who say their customers are open to using non-banks continues to drop.

Last year’s report showed a 10% decrease in brokers who said clients would consider non-banks; the number dropped again this year by almost 4%.

The barriers to putting loans through non-banks remains the same. This year, the same percentage of brokers believe that non-banks’ higher rates and fees are a problem, and just 1% fewer said a lack of brand awareness was a barrier.

Speaking of the fees, a broker from SA said, “Set-up costs are geared towards clients who don’t have mainstream options. For a client who is able to fit into the mainstream, the set-up costs through a non-bank lender can be restrictive.”

Two years ago, non-banks’ lack of brand awareness was said to be the biggest barrier, which suggests that the work done since then to raise the profile of the non-banks has been successful.

The non-banks that won medals for brand recognition have changed this year, with Pepper Money dropping from gold place to bronze. Instead, Liberty was ranked as the non-bank with the best brand recognition, followed by Resimac.

Liberty also won a gold medal for its product diversification opportunities, taking another medal from Pepper Money.

Pepper did retain a medal for its interest rates – albeit a bronze instead of a gold.

Pepper did retain a medal for its interest rates – albeit a bronze instead of a gold.

Interest rates was the top priority for brokers this year, having risen up the ranks from fourth place two years ago. Resimac took home the top prize in that area, followed by La Trobe Financial, which held its position from last year.

When asked what non-banks could do to improve their service, one broker said there could be “better interest rates for alt-doc clients” and another said there could be more “competitive rates in the investor space”.

Resimac took the gold for its product range this year, up from silver last year. Asked what products brokers thought were the best of the past 12 months, Resimac came out on top with its Prime product. Brokers said it was “easy and clear”, “flexible” and “consistent”.

Explaining why Resimac had the best options out there, one broker from NSW said, “[It’s] the lower rates for a non-bank and many options to get a deal through with common sense rather than ridiculous auto assessments by most other lenders which treat clients in a fake and impersonal way.”

Another NSW broker praised both the prime and specialist products off ered by Resimac, saying it had “Great rates, competi-tive borrowing capacity, great BDM support and assesses clients on their own merits”.

Technology, turnaround and service

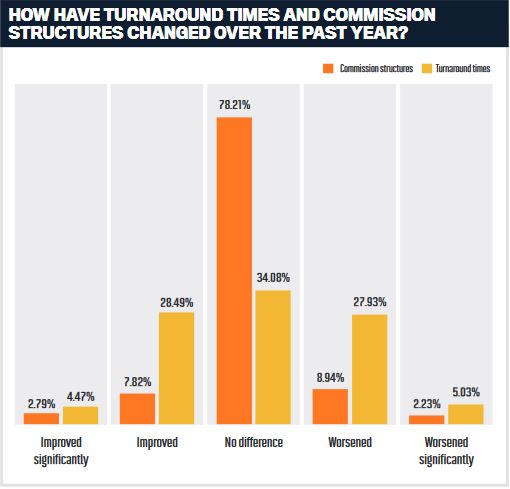

Brokers are split on whether turnaround times have improved or worsened over the last year, but they’re more certain about what non-banks need to improve on

Turnaround times were a hot topic last year as lenders received more business from brokers and increased their scrutiny of applications. Unfortunately, the events of this year mean turnaround times are still front of mind.

The category came in as the joint second highest priority for brokers, only slightly behind that of interest rates.

However, brokers were split on what turnaround times looked like this year. According to the survey, a third of brokers said turnaround times had worsened over the past 12 months. This was up 5% on the proportion of brokers who thought turnaround times had worsened last year.

Another third said turnaround times had improved, while the remaining third said there had been no difference.

“With more brokers going to non-bank lenders to meet loan turnaround times, this has caused non-bank lenders’ turnaround times to blow out,” said one broker from Western Australia.

Another broker, from NSW, disagreed, saying, “Turnaround times have never been an issue with non-bank lenders to be honest”.

Taking the gold medal for turnaround times was Liberty. A number of brokers highlighted the non-bank for its good service over the past year.

One broker from South Australia said, “I have had one situation in particular where I needed a quick turnaround time – Liberty were able to provide exceptional service in this regard, so I have to say that it has improved since last year.”

Another broker praised Liberty’s consistency, while other banks and non-banks have varied: “[It] differs from time to time. Liberty have been really good all year through,” said the broker from Victoria.

Despite losing its gold medal and falling to fifth place, Pepper Money was still high-lighted for its performance in this category. “Pepper has kept its 24hr turnaround times whilst most other lenders were averaging five-plus days,” said a broker from NSW.

There has been no real change in brokers’ attitudes towards commission structures over the past year; just 3% more said there had been no change.

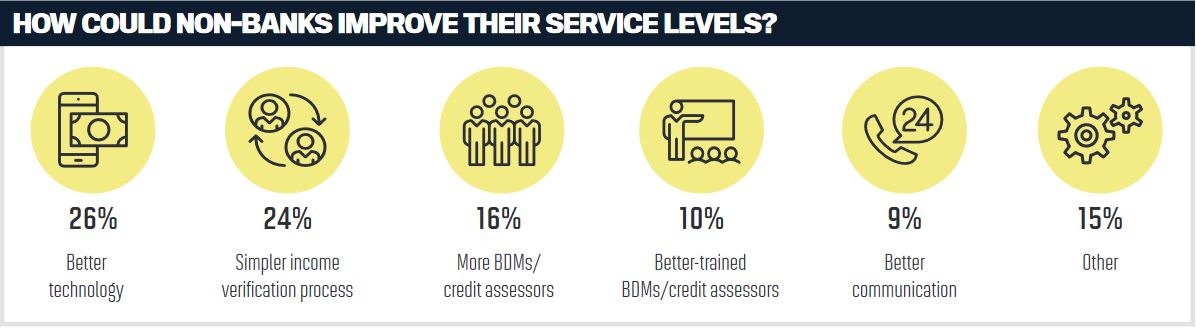

When asked how non-banks could improve their service levels, the majority said they could have better technology. This option came in joint second last year, along-side better-trained BDMs/credit assessors and behind having more BDMs/credit asses-sors. As the industry has had to rely much more on technology this year, this shift is not a surprise.

Compared to just 15% of brokers last year, in this year's survey 24% said simpler income verification processes would improve service levels. Income verification is one factor they said contributed to slower turnaround times over the last year, and lenders have been introducing new technology to make this process digital.

Brokers views on non-bank lenders’ BDMs and credit assessors seem to have improved over the last year, as the proportion of those who think they need to be improved has dropped drastically.

Fifteen per cent of brokers listed other areas that non-banks could improve in. For example, they said non-banks could improve their interest rates and flexibility beyond service calculators.

What you're saying

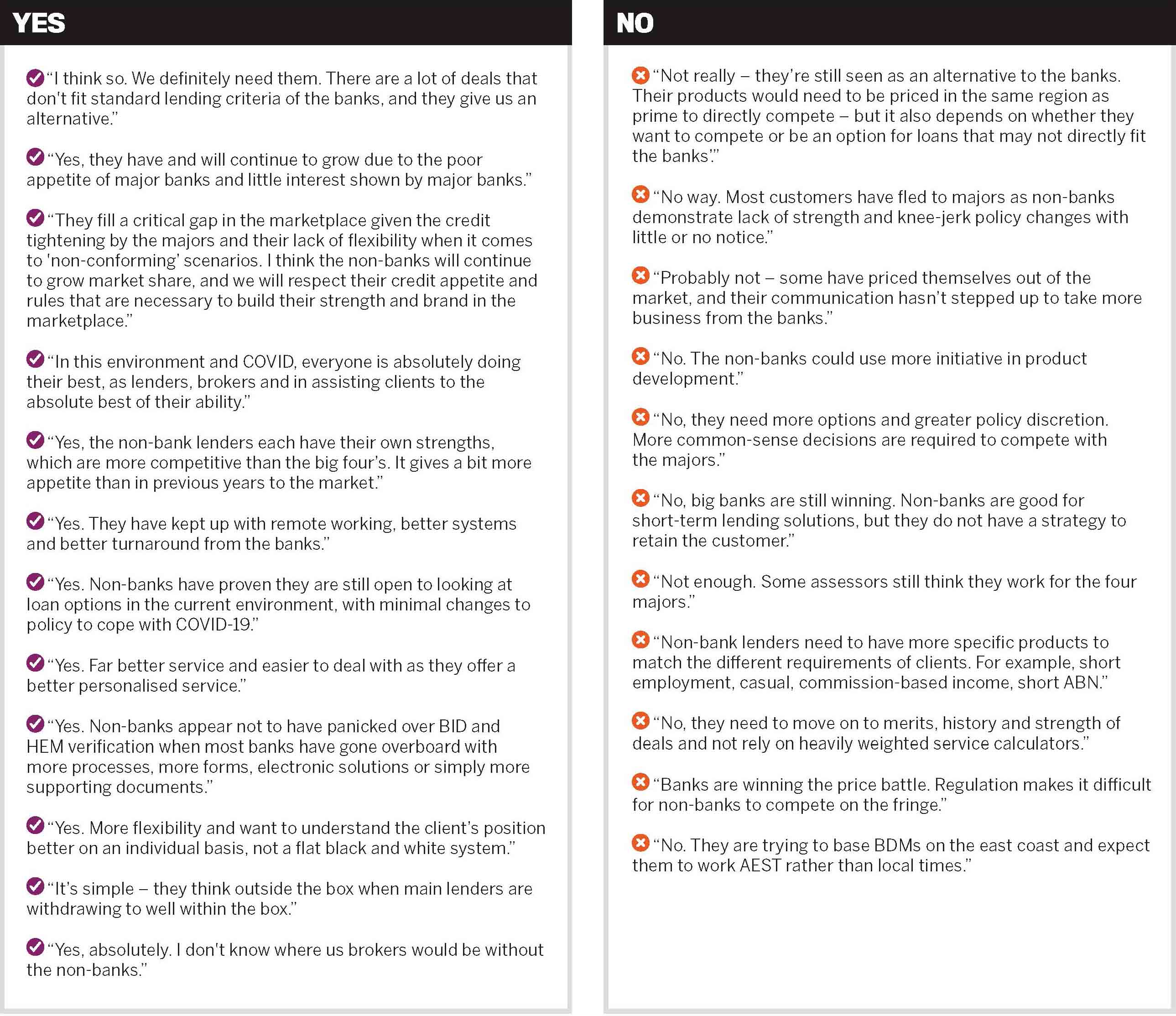

Over a tumultuous two years in lending, have the non-banks done enough to compete with the banks?

Final results

There have been several changes to the ranking of top lenders this year, and the gold medallist from the past two years has dropped to third place

1st. Liberty takes the gold

1st. Liberty takes the gold

Leapfrogging into first place in 2020, Liberty has won five out of eight medals. Group sales manager John Mohnacheff says the non-bank has worked hard with brokers over the past year

MPA: You came top in this year’s Brokers on Non-Banks survey. What do you think helped you achieve this?

John Mohnacheff, group sales manager: Our hope is that brokers have appreciated Liberty’s unwavering and consistent support, even during exceptionally difficult times. We’ve remained open for business, grown our team of BDMs and expanded our product lines to help brokers assist even more customers.

In uncertain times, we’ve focused on providing certainty about the level of service and turnaround times that brokers can expect. And they’ve responded well to the evidence of our commitment to the broker channel as we continue to write home, car, commercial, business and personal loans.

To receive this industry recognition direct from the brokers themselves is a testament to the dedication of the entire Liberty team. From our BDMs to our operations teams, underwriters and support staff, every department has come together during this time to ensure we can provide the same excellent service to brokers that they have come to expect – even in challenging circumstances.

This survey result rea firms that our free-thinking approach to lending and broker support resonates with and is acknowledged by brokers, helping them to better serve customers. Liberty is a trusted business partner they can rely on.

MPA: You came out on top for brand recognition. What have you been doing here, and why is that important to brokers?

MPA: You came out on top for brand recognition. What have you been doing here, and why is that important to brokers?

JM: We’ve continued to demonstrate that Liberty is a brand that brokers can depend on. While continuing to write business, we’ve actively promoted all the ways we can help customers during difficult times so that brokers know they are not alone.

Plus, our consistent communication with brokers through trade publications, social media and digital advertising has reiterated our dedication to the broker channel.

By expanding our product offering in recent months, we’ve shown that Liberty is even more relevant to more people. In challenging times, brokers need lenders to step up and provide the finance solutions that customers need.

Liberty delivers on its promise of excellent service and quick turnaround times when finding free-thinking solutions for brokers, helping us to build a good brand reputation.

MPA: You achieved gold for product diversification opportunities too. What do you offer brokers in this area?

JM: At Liberty, we have an incredibly strong team of BDMs who are passionate about supporting brokers to diversify into new areas of lending. As a business, we quickly discovered the value of diversification and have expanded our product offering exponentially since we launched with home loans in 1997.

We have long touted the benefits of diversification, and it is more important than ever in this climate. We continue to encourage brokers to look beyond home loans and expand their ability to help more customers across commercial, motor, SMSF, personal loans and business finance.

We have developed a training program to give brokers the tools they need to successfully diversify. Over the years, we have continued to refine our ‘Do More’ program to help equip brokers to handle the challenges they may face in their careers. the challenges they may face in their careers.

2nd: Resimac

MPA: You have jumped from seventh place to second place this year, why do you think you’ve done so well with brokers?

Daniel Carde, general manager, distribution: We invest a lot of resources into making sure we meet the needs of our broker partners. This is an ongoing process of continual improvement that ensures we stay relevant in a time of significant change.

Our commitment to the broker channel permeates all aspects of our business operations, from the breadth of our product suite and competitive interest rates through to our industry-leading SLAs of one to two days and our end-to-end digital loan origination process.

It is also manifested in the comprehensive support ecosystem we have built for our brokers, which includes our BDMs, dedicated relationship management team, and online ‘BrokerZone’ portal.

We keep brokers regularly informed about company news, rate changes, products, promotions, appointments, and any other relevant updates in real time through our LinkedIn page and through email updates. In FY20, we sent 43 broker email communications, totalling 369,964 emails.

Our measured response to the COVID-19 crisis no doubt helped our standing with brokers as well. While many of our competitors responded with rate increases and reactive policy changes, we did neither. Instead, we decided to support our brokers by continuing to pay trailing commissions for loans on a payment moratorium, as well as provide additional support for financial hardship applications.

We are always on the lookout for ways to improve the experience for our broker partners and help set them up for success, and we’re pleased to see that our efforts are hitting the mark.

3rd: Pepper Money

MPA: You retained the gold medal this year for BDM support. What do you think accounts for that?

Aaron Milburn, general manager, mortgages and commercial lending: Pepper Money aims to build solid relationships with brokers through regular BDM visits, phone (and now video) communication, being proactive, consistent and reliable. The team’s strong focus on education shows brokers how they can grow their businesses through alternative lending.

Our goal is to help as many borrowers as possible, and our BDMs spend a significant amount of time workshopping scenarios with brokers. Whether or not Pepper can help a broker’s customer, the team are quick to respond with a “Yes” or a “No, and here’s why”.

At its peak, many BDMs were seconded to our operations team to help answer the queries from customers impacted by COVID. That experience has led to the team gaining greater empathy and a deeper understanding of customers’ needs. Through this, they also continued to check in with brokers and keep them updated on how we were supporting their customers.

The fact that we have two Pepper Money BDMs as finalists in the Australian Mortgage Awards is testament to our strategy underpinning BDM support.

4th: La Trobe Financial

MPA: Brokers said the best way non-banks could improve was with better technology, and you won the gold medal for your online platforms and services. What do you offer brokers and why are they so happy with it?

Cory Bannister, chief lending officer: Brokers come to us for instantaneous personal service and direct access to the decision-makers in our 150-strong team of credit analysts – the largest and most experienced of any non-bank in the country. To complement our personalised service model and deliver a seamless experience, we are constantly innovating our online loan delivery platforms and services, as we have done for the past seven decades.

We have offered digital VOI using IDyou and ZipID for many years, DocuSign for loan documents and DigiDocs for mortgage documents in the last 12 months. Our ApplyOnline loan lodgement portal enables brokers to lodge loan applications and supporting loan documentation with one touch through one platform. Our Valuation Hub also enables online valuation ordering to reduce wait times and verification of valuations prior to full lodgement of the loan. And finally, we have partnered with Valocity, becoming the first lender in Australia to access its custom-built Commercial Property Valuation Platform