Banking major also enjoys uplift in SME lending book

National Australia Bank (NAB)’s strategic decision to increase its focus on proprietary lending is beginning to reshape the portfolio mix at Australia’s third-largest home lender.

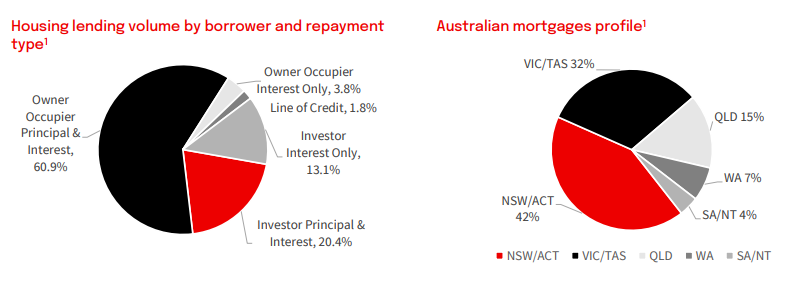

Proprietary loans comprised 47.7% of all new drawdowns in the six months to 31 March, marking a significant step up from 41.4% in the previous six-month period. In the second half of 2023, proprietary drawdowns were as low as 35.3% of all new lending.

Brokers still remain the dominant channel at NAB, accounting for 53.8% of total loans on the books as of March 2026. Despite representing a sequential decline, this is actually a slight increase from last March.

To support its proprietary lending push, NAB recruited around 270 new bankers in financial 2025 – their contribution is now starting to bear fruit.

NAB intends to “continue to grow proprietary lending with high quality bankers supported by a leading ecosystem”, while also aiming to “be the partner of choice for target brokers”.

Total household lending balances across all channels sat at $373 billion in March, representing slightly over 5% year-on-year growth. Average loan sizes surged by 7.5%, with owner-occupier lending growth outpacing investor lending growth.

Business lending remains the standout driver of growth for NAB, with continued momentum across both SME and broader commercial segments. Gross loans and advances increased by 11.5% on a year-on-year basis, with trade, manufacturing, construction and trade, and accommodation and cafes seeing double-digit growth.

The bank is also consolidating its leadership in SMEs. SME market share increased to 28.2%, up from 27.7% a year earlier, while total Australian business lending share rose to 21.9%, from 21.5%. Around 70% of SME lending sales came via the proprietary channel in the period.

“Geopolitical tensions have created a more volatile macro economic environment,” said NAB chief executive Andrew Irvine. “We enter this period in good shape and actions taken in 1H26 to bolster our balance sheet will allow us to continue to grow and support customers.”

Irvine drew attention to the $300 million increase in forward looking collective provisions to cushion the bank against future bad credit shocks. “We will continue to manage our business for the long term to deliver sustainable growth and attractive returns for shareholders,” he added.