New figures show arrears stabilising and borrowing activity resilient despite cost-of-living pressures and RBA rate rises

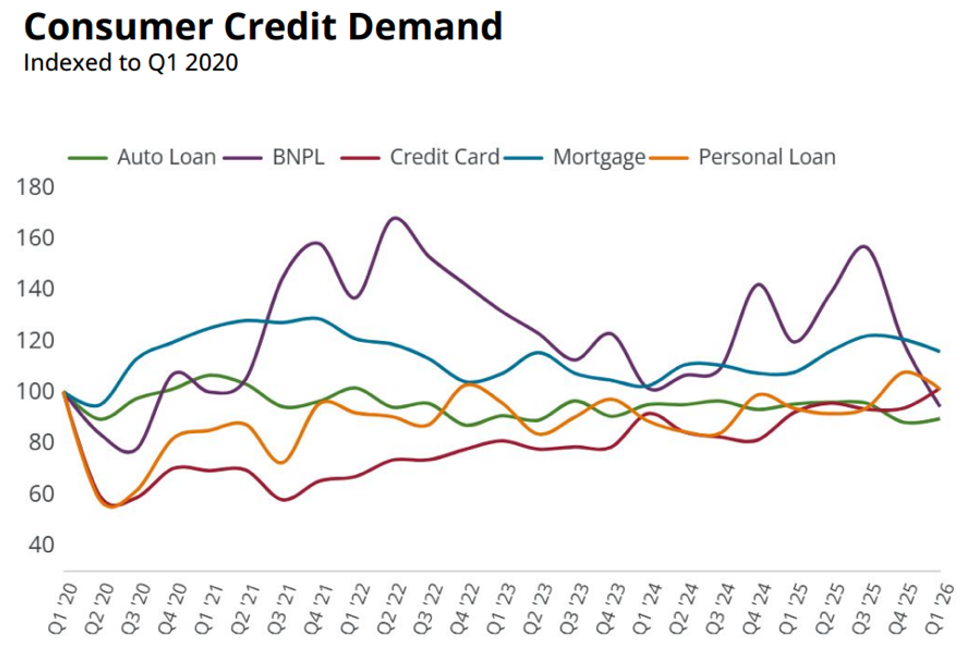

Demand for home loans rose 7.5% year-on-year in the first quarter of 2026, with arrears across major portfolios remaining near recent lows, according to Equifax’s Consumer Market Pulse for Q1 2026.

The findings point to a credit market weathering economic headwinds more robustly than many had anticipated, drawing comparisons to the resilience seen during the 2022–23 rate-tightening cycle.

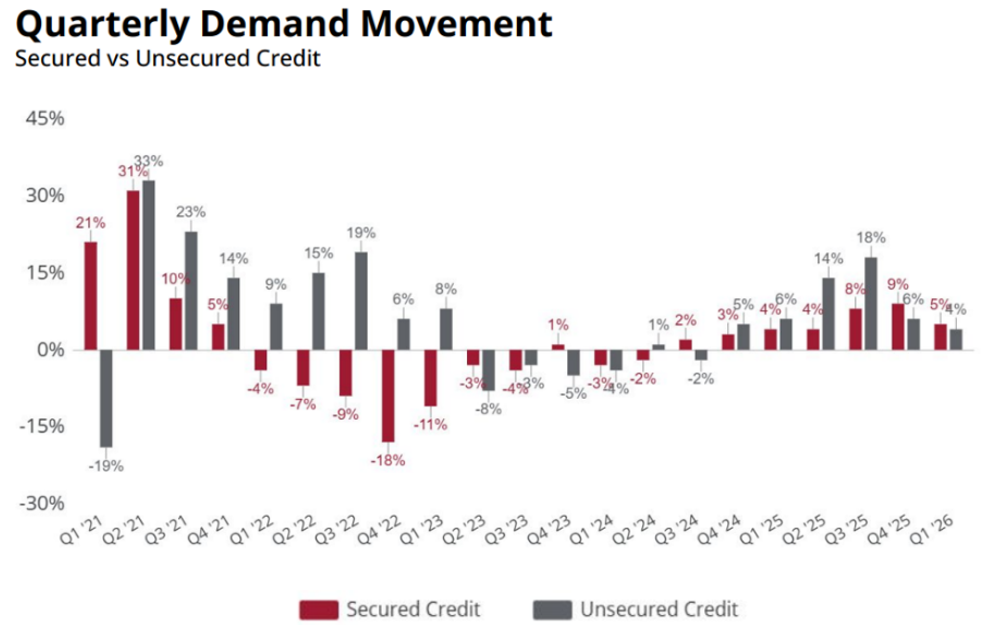

Secured credit demand grew 4.9% year-on-year, with mortgage activity the primary driver. Arrears rates held at the lower end of recent historical ranges despite elevated petrol prices, persistent cost-of-living pressures, and successive RBA rate increases weighing on consumer confidence.

Source: Equifax

Equifax noted that current conditions echo those of 2022–23, when a 4% rise in the cash rate within roughly 12 months and peak inflation of 7.8% prompted fears of widespread credit failures and a so-called “mortgage cliff.” Those fears did not materialise, with credit card demand remaining steady and mortgage arrears stabilising relatively quickly after an initial rise.

“With global uncertainty, supply chain disruptions, higher consumer borrowing rates and rising fuel prices, it is easy to suggest that we could expect to see a dramatic decrease in credit demand,” said Kevin James (pictured right), chief solution officer at Equifax. “However, it’s important to recognise that we can draw parallels to conditions consumers experienced in 2022 and 2023.

“With global uncertainty, supply chain disruptions, higher consumer borrowing rates and rising fuel prices, it is easy to suggest that we could expect to see a dramatic decrease in credit demand,” said Kevin James (pictured right), chief solution officer at Equifax. “However, it’s important to recognise that we can draw parallels to conditions consumers experienced in 2022 and 2023.

“The data demonstrates the resilience of Australia’s credit market, as long as factors such as unemployment remain low. The labour market is also a key factor when considering the appetite and ability of consumers to borrow and spend; and in line with the overall resilience theme of the Equifax Consumer Market Pulse, the unemployment rate, at 4.3%, is near 50-year lows.”

Upgrades and refinances drive mortgage growth

The 7.5% year-on-year rise in mortgage demand was led by upgraders and refinancers rather than first-time borrowers, with new market entrants falling approximately 3.5% over the same period.

Among new mortgage accounts, borrowing limits grew 6.7% year-on-year in dollar value, indicating that a smaller number of new accounts is underpinning portfolio growth.

Source: Equifax

“The reduction in new market entrants likely reveals that during a trying period of intense economic headwinds, Australians were focused on managing existing financial obligations and mortgage debt in Q1,” James said. “For new mortgage accounts, borrowing limits are growing in dollar amount value up +6.7% year on year, revealing that a smaller number of new accounts are driving portfolio dollar value growth.

“With mortgage lending being often a useful indicator of dwelling price direction, positive growth in mortgage demand could suggest the price cycle is yet to turn down. This outcome would align with previous cycles where dwelling prices remained resilient; historically, the market has maintained a long-term average growth rate of approximately ~6% per annum, even during periods of RBA tightening.”

Arrears broadly stable, though personal loan stress emerging

Mortgage arrears at 90 or more days past due improved in Q1 2026, with a three-basis-point reduction in active accounts and a 2.2% decline in total limits compared with Q1 2025. Credit card delinquencies at the same threshold stood at 0.31%, down nearly 3% in financial value year-on-year, with an notable 10% reduction in arrears among the 18–25 age demographic contributing to the improvement.

Personal loans presented a more mixed picture. While the headline 90-plus days past due rate stabilised and the volume of accounts in arrears fell by 14 basis points, the financial value of personal loans in arrears rose 3.1%, pointing to growing stress on larger balances.

“The softening of mortgage and credit card arrears in Q1 showcases Australians' responsible financial reaction to economic headwinds,” James said. “Interestingly, the personal loan arrears indicators demonstrated features of exposure divergence - while headline 90+ DPD arrears rates stabilised and the volume of accounts in arrears improved by 14 basis points, the financial value of those personal loans in arrears rose +3.1%, indicating mounting stress on larger balances.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.