What factors influence house price inflation and their impact?

BNZ’s latest Property Pulse anticipates a 5% rise in house prices for the year, with market dynamics hinting at a stronger second half despite current challenges.

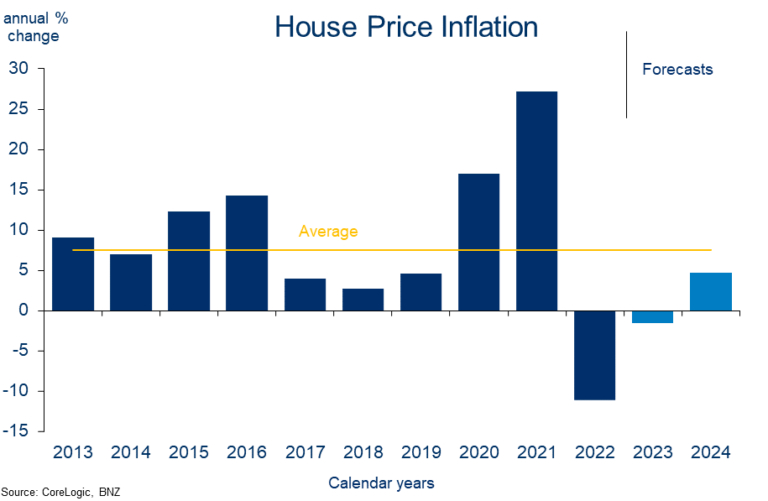

Market forecast for 2024

Mike Jones (pictured above), BNZ chief economist, projects a modest 5% increase in house prices for the year, slightly lower than previous estimates, with significant gains expected in the latter half.

“High mortgage rates and stretched affordability are restraining demand, essentially nullifying the demographic and policy tailwinds blowing in the market’s favour,” Jones said, setting a cautious tone for the initial months.

The first half of 2024 is expected to see limited market activity, with a combination of high mortgage rates and affordability issues dampening demand. Unsold inventory levels have reached a seven-year high, reflecting the market's struggle to assimilate new listings.

Jones predicted a thaw in housing market activity moving into the second half of the year, spurred by a shortfall in new home construction against population needs and potential for lower mortgage rates.

“We expect house prices to rise modestly over the second half of this year,” he said, aligning with the Reserve Bank’s anticipated interest rate cuts.

Macro factors affecting house prices

According to the BNZ report, despite a recovery in house prices, the market faces headwinds from macroeconomic factors, including demographic trends and mortgage rates. Listings have surged, yet sales have not kept pace, indicating a market-adjustment period ahead.

BNZ summarises the different factors influencing house price inflation and their impact in the table below.

Mortgage rate outlook and predictions

The BNZ report delved into mortgage rate dynamics, expecting floating rates to stabilise and fixed rates to potentially decrease slightly by year-end.

“The economy remains in a rolling recession, labour market tightness is a thing of the past, and inflation is falling rapidly and forecast to be back in the Reserve Bank’s 1-3% target range later this year,” Jones said. “To us, this mix of conditions points to a need for lower interest rates in time. The missing ingredient is a bit more progress on (core and headline) inflation continuing to fall.”

Considering these factors, BNZ predicts that RBNZ might lower the cash rate starting from November. The risks associated with this prediction are seen as evenly balanced, indicating that rate cuts could occur sooner or later than anticipated.

“But should our November forecast pan out, floating mortgage rates would be expected to end 2024 a little lower than currently, with chunkier falls in 2025,” Jones said.

To read the BNZ’s Property Pulse in full, click here.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.