BCG research shows the bottom 80% of Canadian earners are now spending beyond their means

New research from Boston Consulting Group (BCG) reveals that net savings across the bottom 80% of Canadian households have turned materially negative — a finding with direct implications for housing affordability and the borrowers that mortgage brokers serve.

The BCG analysis tracked household income and spending patterns from 2021 to 2025, finding that while real consumer spending rose approximately 2% in Q1 2026, broadly in line with Canada's ten-year average, that headline figure conceals a deeply fragmented picture.

For the four quintiles outside the top 20% of earners, spending growth is not being driven by income. It is being sustained by a combination of savings drawdowns, rising portfolio values, and increasing debt loads.

The widening gap between income and spending

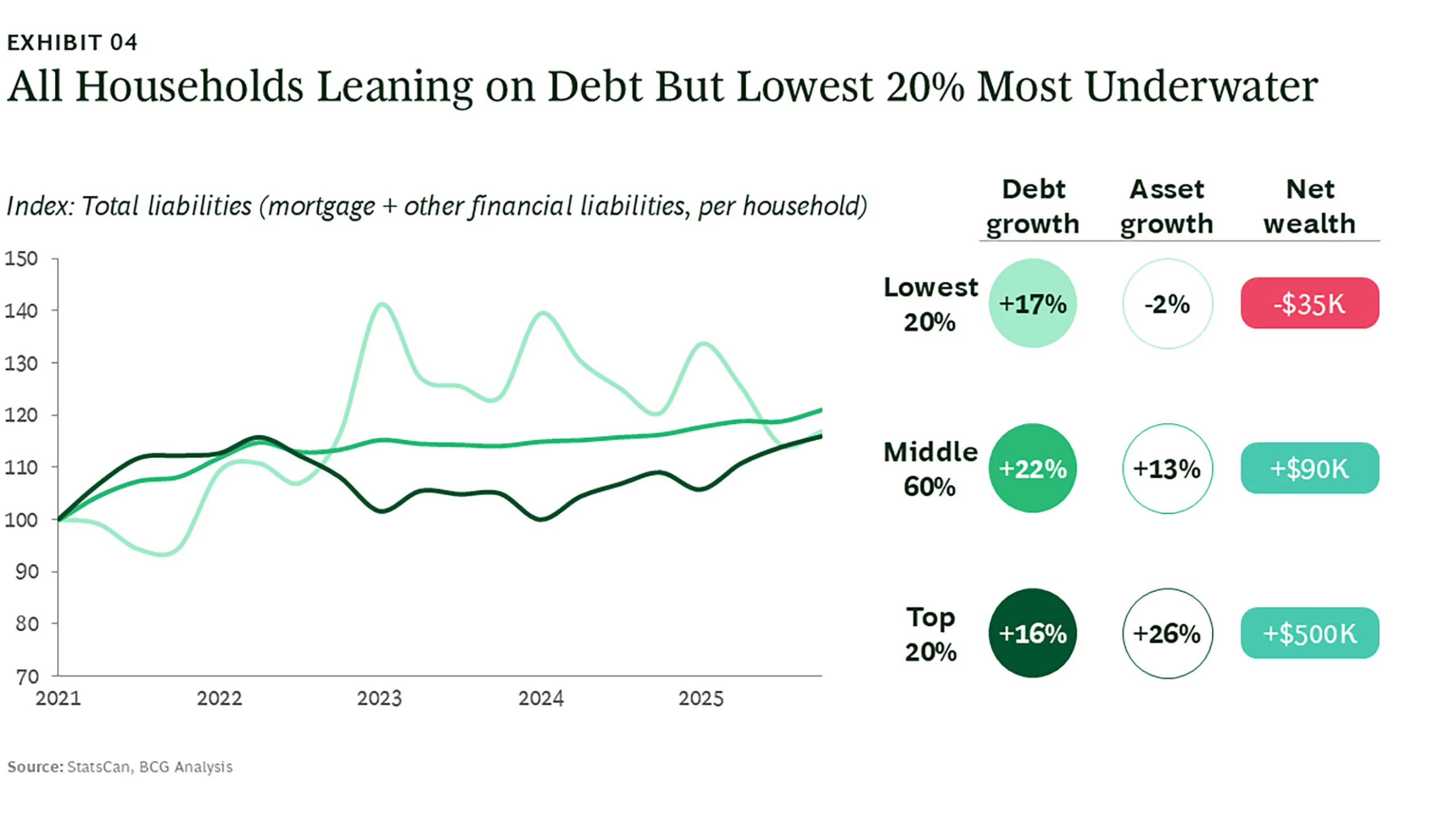

The lowest 20% of earners saw spending rise 27% between 2021 and 2025, against disposable income growth of just 3%. The middle 60% of households — the traditional engine of the Canadian consumer economy — found that income covered just 57 cents of every new dollar they spent.

Only the top quintile ended the period with their financial position broadly intact, with income growth outpacing new expenditure at 106%.

The result is a mounting savings crisis at the household level. The bottom quintile averaged -$39,000 in net annual savings by 2025 and took on 17% more debt even as their total asset base shrank, a net worth decline of approximately $35,000 per household.

The middle 60%, meanwhile, moved from modest positive savings to a per-household deterioration of roughly $7,000.

The BCG Global Consumer Radar Survey found that 41% of Canadians do not expect to save, or expect to save less, over the next six months, a figure that has held stubbornly above September 2024 levels.

Household debt-to-disposable income climbed to 179.6% in Q1 2026 as mortgage originations hit a two-year low, a sixth consecutive quarterly increase, reinforcing just how far credit has become the default mechanism for maintaining household consumption.

What a thinning savings buffer means for mortgage borrowers

BCG found that the growth in consumer outlays is concentrated not in goods — purchases of cars, appliances, and furniture are falling — but in services, particularly financial services tied to borrowing and asset-linked fees.

Households are spending more to service their debts, not to build material wealth or savings cushions.

The report also flags two macro-level signals with direct implications for mortgage pricing. Five-year Government of Canada bond yields have risen approximately 40 basis points in recent months, and equity valuations sit near a 25-year high relative to the size of the economy.

If asset values soften while borrowing costs climb, the households with the thinnest savings buffers will have the least capacity to absorb the shock — and those are, increasingly, the households applying for mortgages.

That prognosis carries particular weight given where Canada's housing market already stands. Canada's affordability ratio remains structurally among the worst in the developed world, with National Bank of Canada's Housing Affordability Monitor recording mortgage payments at 52.3% of household income as of Q1 2026.

BCG's findings suggest that for the majority of Canadians, the savings capacity that might otherwise support a down payment or cushion against a rate increase is thinning, not strengthening.

Make sure to get all the latest news to your inbox on Canada’s mortgage and housing markets by signing up for our free daily newsletter here.