The figure is a significant increase from 2022

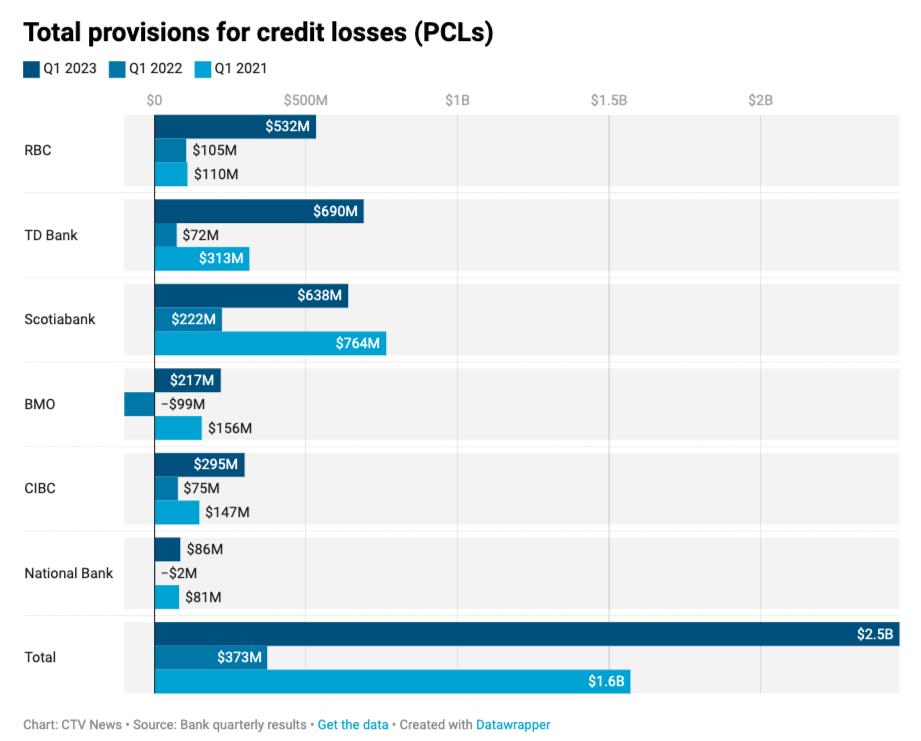

Canada’s Big Six banks have set aside a total of over $2.4 billion as provisions for credit losses in anticipation of an influx of Canadians unable to pay off their debts and a recession later this year.

The Royal Bank of Canada, Bank of Montreal, TD Bank, Scotiabank, CIBC, and National Bank all outlined the cumulative billions they had set aside for credit defaults – also known as provisions for credit losses or PCLs – in the first quarter results they published earlier this year.

Around this time last year, the Big Six had allocated only $373 million for PCLs – around 15% less than it has set aside for the year ahead.

It was also in the first quarter of 2022 that the Bank of Canada began hiking interest rates in its ongoing tussle with inflation, which has since climbed to a record 4.5%, the highest interest rate recorded since 2007.

“[Some] people cannot repay loans that they have taken out," a University of Toronto Rotman School of Management professor of finance, Laurence Booth, said to CTVNews.ca. Booth explained that while credit losses happened on a regular basis, they generally shot up each time the country was headed towards a recession and people lost major sources of their income, such as their employment or small business profits.

“Currently, with the Bank of Canada pushing up short-term interest rates to slow down the economy and bring inflation down, the expectation is for a recession in Q2 or Q3 this year,” Booth said. “Consequently, the banks are making provisions for potential losses should a recession occur.”

Can anything prevent the influx of credit defaults?

Earlier this year, bank executives agreed a high employment rate and better savings could help avert a large increase in payment defaults, CTVNews.ca reported.

“Current underlying conditions, particularly the strong level of employment and consumer savings, are supporting a slower rate of normalization of impaired PCLs than we had expected," National Bank executive vice president of risk management William Bonnell said in an earnings call earlier this year. “The same factors we discussed last year – inflationary pressures, geopolitical risks, and the direction and timing of interest rate changes – are still present and all contribute to a less certain outlook.”

Royal Bank of Canada chief risk officer Graeme Hepworth said that while the PCL ratio on impaired loans was lower than they were pre-pandemic, the bank had observed “the normalization of delinquencies and impairments” driven by the impact of climbing interest rates on credit outcomes.

“We expect PCL on impaired loans to increase through 2023, as we head into a forecasted recession,” said Hepworth.

Bank of Montreal chief risk officer Piyush Agrawal agreed that BMO’s provisions for credit losses remained below pre-pandemic levels and that the quarterly increase in impaired provisions for credit losses was consistent with “the expected normalization trend in delinquency rates in unsecured consumer loans and credit cards”.

What does this mean for Canadians?

Rotman School of Management associate professor of finance Claire Celerier explained that bigger reserves for loan defaults – or higher PCLs – pulled down banks’ ratio of equity to assets, which in turn affected the banks’ lending capacity.

“This might contribute to a decrease in lending in the coming months,” Celerier told CTVNews.ca.

Any thoughts on the story? Let us know in the comments below.