A structural shift is quietly reshaping Australian mortgage lending, and brokers who move early stand to carve out a significant competitive advantage

The later-life lending and equity release space – once a niche corner of the industry – is emerging as one of the most underserviced and fastest-growing opportunities in Australian mortgage finance.

According to James Green (pictured), co-founder of Clinch Finance, roughly three quarters of Australia’s property wealth is held by borrowers aged over 50, yet the lending market has not kept pace with that demographic reality.

Of course, there are hundreds upon hundreds of lenders servicing the sub-50 market, from traditional lenders to a rising cohort of non-banks and private credit players, but “for the market above 50 years old, there's probably half a dozen”, said Green.

That mismatch of a vast, equity-rich population being served by a handful of specialist lenders makes for a rich ground of opportunity.

Where Australia's wealth actually lives

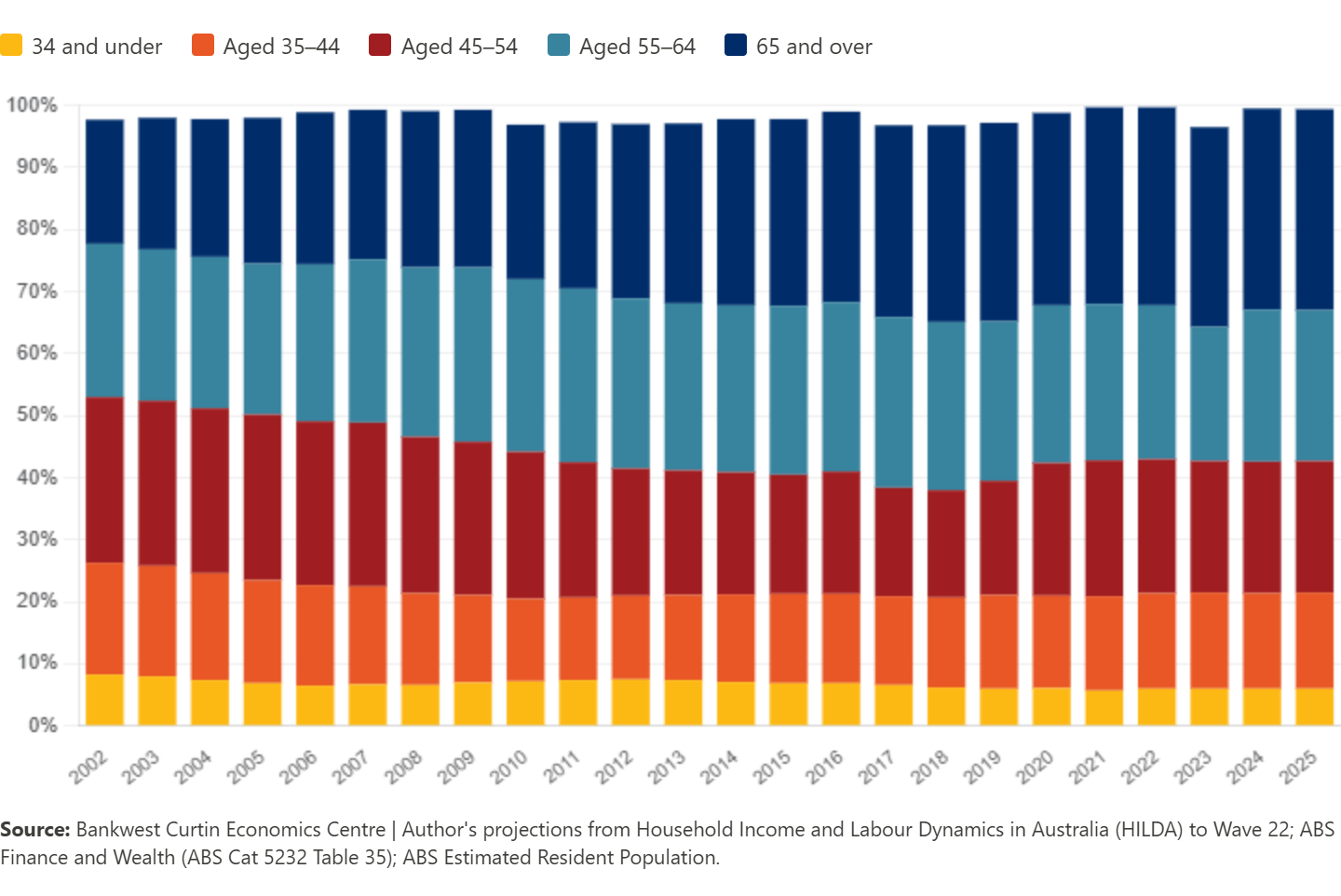

The scale of wealth concentrated in older Australians was clearly outlined in the Bankwest Curtin Economics Centre (BCEC) Policy Brief, published in March 2026.

The report showed Australia's total household net worth reached an estimated $18.4 trillion in 2025, underpinned by sustained growth in housing values, superannuation balances and financial assets.

Of that figure, households with a head aged 65 and over now hold just under $6 trillion – equivalent to just over 32% of total household wealth. That share has risen substantially from around 20% in 2002, driven by four intersecting forces: rising housing equity accumulated over longer working lives; the maturation of Australia's compulsory superannuation system; strong asset growth over the past two decades; and the demographic weight of large Baby Boomer cohorts entering retirement.

The population dynamics underlying this shift are significant in their own right.

The number of Australians aged 65 and over has more than doubled since 2000, rising from 2.36 million to 4.84 million in 2025. The 65-plus cohort is now expanding at an average rate of 2.9% per year since 2020, with the 70-plus cohort growing even faster at 3.4% annually. Today, around 17.5% of all Australians are aged 65 or over – compared with just over 10% in the mid-1980s.

Housing is the dominant engine of that accumulated wealth. The 65-plus cohort holds an estimated $2.8 trillion in net property wealth, representing just over 30% of Australia's total housing assets, the BCEC report found. In gross terms, that figure rises to $2.97 trillion in property holdings, set against just $134 billion in loan liabilities – a leverage ratio of only 4.5%. Most households in this cohort carry little to no mortgage debt, and many own their homes outright.

Beyond property, the 65-plus cohort also holds an estimated $1.46 trillion in superannuation assets, or around 31% of total superannuation savings nationally. This figure is expected to grow as successive cohorts enter retirement with larger balances than those before them.

The picture that emerges is one of enormous, largely illiquid wealth held by a rapidly expanding population segment – equity-rich but often cash-constrained, and increasingly in need of financial products designed for the realities of later life rather than the assumptions of a younger borrower profile.

What brokers couldn't do before

Despite these crystal clear demographic trends, traditional lenders have long struggled to accommodate equity-rich borrowers who lack conventional income streams, namely retirees, semi-retirees, and older Australians whose wealth sits in property rather than a pay cheque.

"Brokers didn't have a place to put these loans," Green said. "Some of these customers would come to them and they'd go, 'I can't help you.' And now they don't have to do that."

That gap is precisely what specialist lenders like Clinch Finance and competitors like Bridgit are seeking to fill. Their products available typically involve short-term bridging terms of up to 24 months, capitalised interest paid back in a lump sum, and exit strategies built around property sale, refinancing, or the completion of a renovation.

Critically, they assess borrowers on the asset rather than income, with loan-to-value ratios capped conservatively – in Clinch's case, at a maximum of 65%.

A demographic wave brokers can't ignore

As the financing market plays catch up with an ageing population, the construction pipeline is also responding, with a wave of purpose-built downsizer developments – typically compact, single-storey homes priced between $600,000 and $800,000 – appearing across the country's major metropolitan fringes.

Typical retirement villages, these are not. “Equity-rich homeowners that are looking to downsize tend to prioritise access to lifestyle, with proximity to transport, healthcare and retail outweighing the need for space,” REA Group senior economist Eleanor Creagh said in a recent piece published by realestate.com.au.

“As a result, we tend to see downsizers favour amenity-rich, inner- and middle-ring suburbs, where downsizers can remain connected to their community without compromising on liveability,” Creagh added.

The 103-residence St Clare project in Melbourne’s inner east, for instance, was designed by Woods Bagot to allow residents to "age in place gracefully and without friction”. On Sydney's upper north shore, Hermitage in St Ives – due for completion mid-2026 – comprises 26 single-level residences within 450 metres of St Ives Shopping Village.

Green also noted a hotbed of downsizer activity along Eastern Valley Way in Sydney’s lower north shore.

But downsizing is only one piece of the picture. Green described a broader pattern of equity release activity playing out across the over-50s cohort, driven by a range of motivations that brokers are increasingly being asked to navigate.

"A lot of them are accessing their equity to help them now," he said, pointing to one scenario that has become increasingly common: grandparents purchasing their adult children's homes outright, moving in, and leaving the younger generation mortgage-free.

Other borrowers of all ages are using bridging finance in response to current housing market conditions. "Most people are buying now because they can get a bargain and then deferring their sale – anywhere between 12 and 24 months – because they'd rather sell when they think market conditions will normalise," Green explained.

Heating up

Clinch itself is an illustration of how quickly demand can build once a clear solution exists. The company has been operating for just nine months, but growth has been substantial.

"In terms of loan book growth, we have grown astronomically," Green said, albeit off a low initial base.

The competitive landscape, for now, remains thin. Green acknowledged that consolidation or the arrival of international players could change the dynamic in the years ahead, but said the market is still in its early stages. "I think where it really heats up and gets exciting is in the next couple of years,” he said.

For brokers, a demographic cohort holding the lion’s share of Australia's property wealth is actively seeking solutions – and the number of lenders equipped to serve them remains startlingly small. The brokers who build their knowledge of the equity release and later-life lending market now will be well positioned as that demand intensifies.