As brokers work harder than ever to get deals across the line, is it time for a fee model rethink?

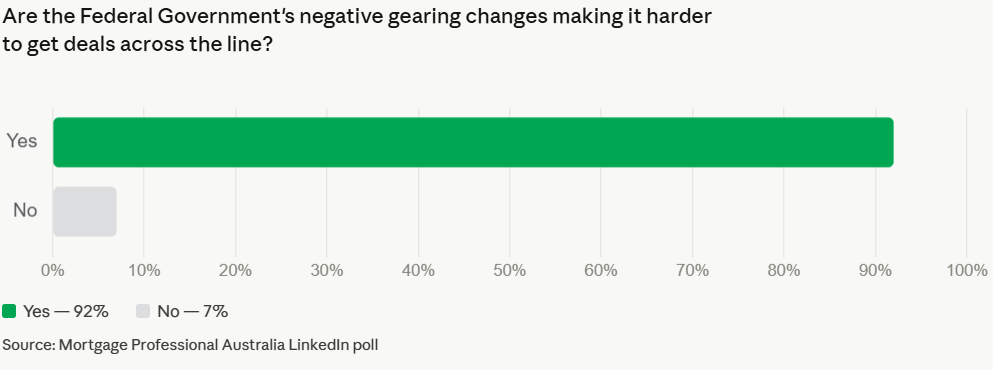

Australia's mortgage brokers are working harder than ever to get deals across the line, as the federal government's negative gearing changes create policy inconsistencies, servicing calculator errors and a wave of in-transit deal complications that are adding significant time and complexity to every file.

Per-deal workloads have increased and brokers are having to have more strategy conversations before clients are ready to proceed, leading to mounting concern that brokers will be doing more work for lower or delayed revenue, which could have implications for the industry’s fee model.

While some brokers are seeing an opportunity to reposition themselves as strategic advisers, they are also cautious of moving into the tax and financial advice spheres.

Andrew Stevens (pictured, left), national manager at Nectar Mortgages Group, is seeing this post-Budget confusion play out across Nectar’s 200-plus broker network.

"That confusion comes from both the inconsistency from lender to lender, from policy right through to lender calculators, which were already quite inconsistent from lender to lender,” Stevens told MPA.

The policy confusion has been compounded by lenders pulling in-transit deals from their pipelines without notifying brokers, while turnaround times have blown out, particularly among smaller lenders.

Stevens said one bank has “taken a whole bunch of deals out of the system and just cancelled them without communicating to the brokers directly”. While a broker could log onto the portal to see these changes, the lack of direct communication was a source of frustration.

In some instances, when a deal is quietly cancelled and later requires resubmission, the borrower may no longer qualify under the new policy settings. "It has been handled really poorly by some lenders," Stevens said.

Katie Thomas, founder and managing director of Focus Finance, has also seen an increase in per-deal workload.

“Some files require double handling or resubmissions, in-flight deals require additional cross checking to ensure they’re still valid, and others in pre-submission require additional verifications due to the rapid change of policies,” said Thomas. “Then there is the additional time in the client conversation to discuss next steps and forwarding planning.”

Borrowing capacity drops by up to 12%

Stevens estimates that, on a like-for-like basis, borrowing capacity for investment borrowers has fallen by between 8% to 12% since Labor scrapped negative gearing benefits on existing properties on 12 May. However, he added that deal structure can make the actual impact far greater or far less.

Some borrowers have seen their borrowing capacity drop by as much as 30% at some lenders, causing brokers to restructure deals and take them elsewhere.

The variation between lenders comes down to how each has interpreted and implemented the policy changes. Some have removed negative gearing from their calculators entirely, while others are still applying it in certain grandfathered situations. Other lenders are holding off until (or, if) the negative gearing changes are formally legislated.

A specific example of confusion flagged by Stevens involves cross-securitised investment properties where one falls under grandfathered rules and one does not. "How do you treat that loan, and then how do you place that loan in a lending calculator to get the correct result?" he said. "Most lenders will play the conservative card first."

The fee conversation is changing

Beyond the immediate policy disruption, Stevens says the changes are forcing a rethink on brokers’ fee models.

"Every deal is just taking a lot more work to put together to get it through in a way that is read correctly by that lender," he said. "Those brokers who have been a little bit more lazy or just relying on AI – they're struggling."

With deals becoming more complex and requiring more effort, and brokers increasingly expected to provide investment strategies alongside loan structuring, some are now exploring fee-for-service models.

"(Brokers) are not selling a home loan product. They are selling the strategy that matches the goal, and navigating that,” said Stevens. “Brokers are the only professionals customers can obtain lending strategy and recommendations that are in their best interest, and this is valuable.”

Non-bank lenders picking up investor business

Stevens said inquiries about alternative and non-bank lenders such as Pepper Money, Bluestone Home Loans and Brighten have increased noticeably across his broker networks since the Budget, driven by their more flexible treatment of complex scenarios and SMSF lending.

"Their policies are just naturally more friendly and easier to understand when it comes to some of the complexity that's come into the lending space," he said.

But this is a trend with a tail that stretches beyond the events of May 12.

"This investor lending transition to the non-bank space is something that's been happening for a couple of years," Tony MacRae (pictured, right), chief commercial officer at Bluestone Home Loans, told MPA. However, the federal government's negative gearing changes have certainly kept the trend firmly in focus.

MacRae’s view is that the major banks were already under pressure to pare back their investor lending books well before the May Budget.

Bluestone, which has been deliberately growing its investor loan volume over the past 18 months, had not updated its own negative gearing policies at the time of writing, with MacRae noting that the legislation had not yet been passed by the Senate but Bluestone will be complying with relevant legislation.

MacRae urged investors to seek independent financial advice before proceeding under the new conditions. "Whatever changes get put through, people will recalibrate and work out what the new norm is," he said. "Australians are not going to stop their love affair with property."