Australians purchasing their first home can save for a deposit faster, but there is a drawback too

The journey to owning a first home in Australia has become more complex due to the dual impact of high interest rates, according to property marketplace Domain.

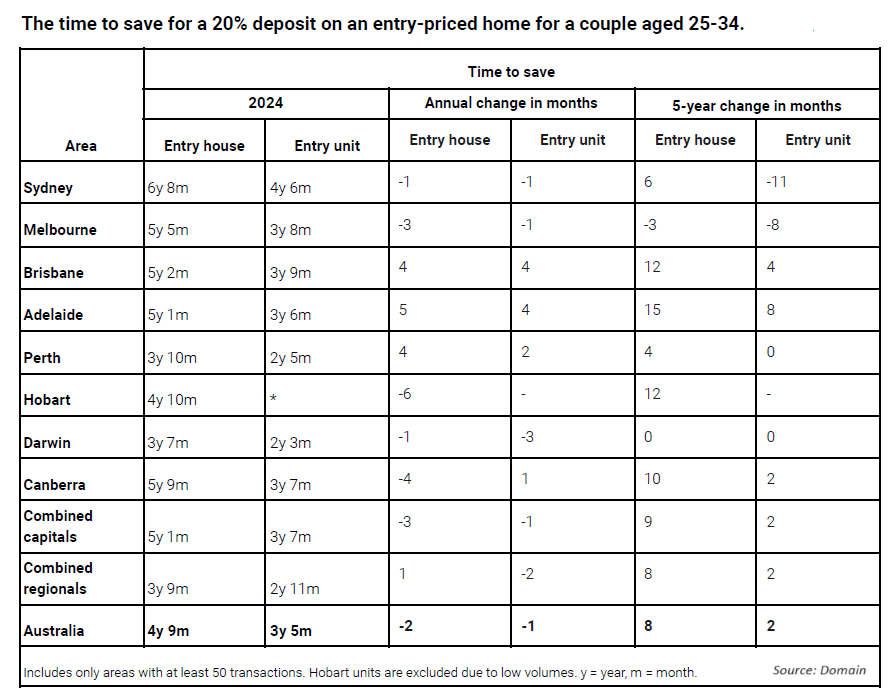

In its latest 2024 First Home Buyer Report in collaboration with digital lender Unloan, it was found that higher rates assist in accelerating the savings process by two months for properties at entry-level prices for those who manage to save regularly.

A couple aged between 25 and 34 now need less time to save a 20% deposit for an entry-level property, with houses and units requiring two months and one month less, respectively, compared to the previous year.

However, this financial benefit comes with a significant drawback. Once first-home buyers have secured their property, they encounter the challenge of increased mortgage repayments, resulting in mortgage stress and adding to the complexities of home ownership.

“The current market still poses significant challenges for first-home buyers, given the record high property prices and the ongoing cost-of-living crisis,” said Nicola Powell (pictured left), chief of research and economics at Domain.

“While there has been a slight decrease in the time required to save compared to the previous year, it’s important to note the nuances involved. This decrease primarily applies to Australians who can save a consistent amount ongoingly and have experienced wage growth, as these factors are key drivers.”

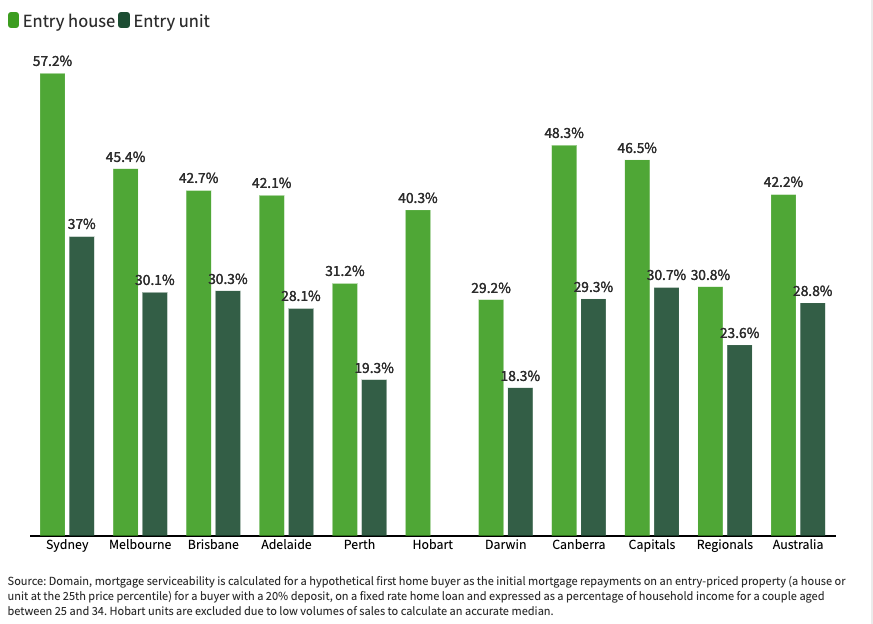

The report also highlights the issue of mortgage serviceability, which has become more difficult for first home buyers. With mortgage repayments for entry-level properties now consuming a larger portion of average household income for the target age group, many are experiencing mortgage stress.

Specifically, the report indicates that mortgage repayments for both houses and units exceed the recommended threshold of 30% of income, underscoring the pressure high interest rates place on first home buyers.

“Our data shows that mortgage serviceability is stretched across our capitals, as both entry-level house and unit home loan repayments surpassing this comfortable threshold, accounting for 46.5% and 30.7% of income, respectively,” Powell said. “The stretched mortgage serviceability highlights the dual effect of high cash rates on first home buyers.

“While there has been a slight reduction in the time required to save a deposit (for those who can consistently save and have experienced wage growth), the higher interest rates are also making home loan repayments more difficult, which is why more people are facing mortgage stress,” Powell said.

She also discussed the increasing dependence of first-home buyers on financial assistance from parents to afford a deposit and suggests exploring different types of homes or locations to find more affordable options.

Powell then called for government intervention to address the housing supply issue, citing the Help to Buy scheme as a positive step towards support.

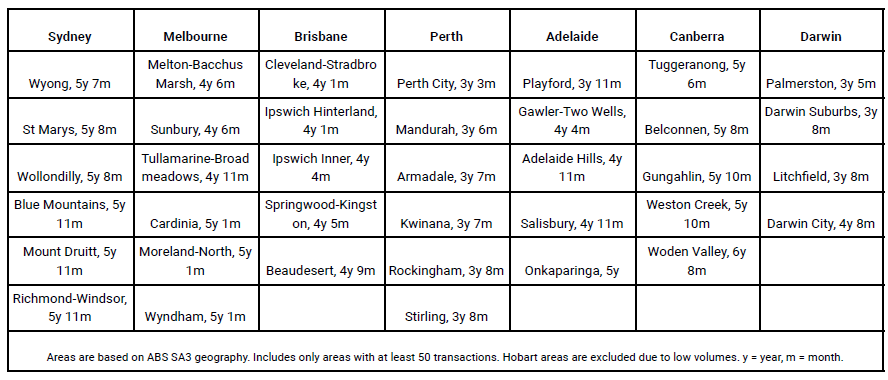

To support first home buyers, the report has revealed the areas with the shortest saving times for a 20% deposit on an entry-priced house by city.

“We want to see more young Australians achieve their dream of owning a first home,” said Dan Oertli (pictured right), chief executive of Unloan.

“Buying a home is one of the biggest purchases most Australians will ever make – and knowing where to start can feel overwhelming. That’s why we’ve collaborated with Domain to share some insights to help first home buyers enter the market with more confidence.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.