Both lenders now offer the most competitive fixed rates among the five biggest banks

ANZ has reduced its two- and three-year fixed home loan rates by up to 10 basis points (bps), moving against the direction taken by its big four bank peers. The bank's lowest fixed rate now sits at 6.29% for a two-year term.

Macquarie Bank has made similar moves, cutting its fixed rates to a low of 6.09% for a three-year term — the lowest fixed rate among Australia's five largest lenders.

The cuts come just a day after Westpac raised select fixed rates by 5bps, and following NAB's recent fixed rate increases.

"ANZ and Macquarie have shifted gears, cutting fixed home loan rates at a time when the majority of the market is still trending up," said Sally Tindall (pictured right), data insights director at Canstar.com.au. "While these cuts are modest, they are enough to put Macquarie and ANZ in front of their big bank competitors.

"ANZ and Macquarie have shifted gears, cutting fixed home loan rates at a time when the majority of the market is still trending up," said Sally Tindall (pictured right), data insights director at Canstar.com.au. "While these cuts are modest, they are enough to put Macquarie and ANZ in front of their big bank competitors.

"The mixed signals from these fixed rate changes highlights just how uncertain the outlook remains. While two of Australia's bigger banks might be cutting, fixed rates have a decent way to fall before they get back to being competitive."

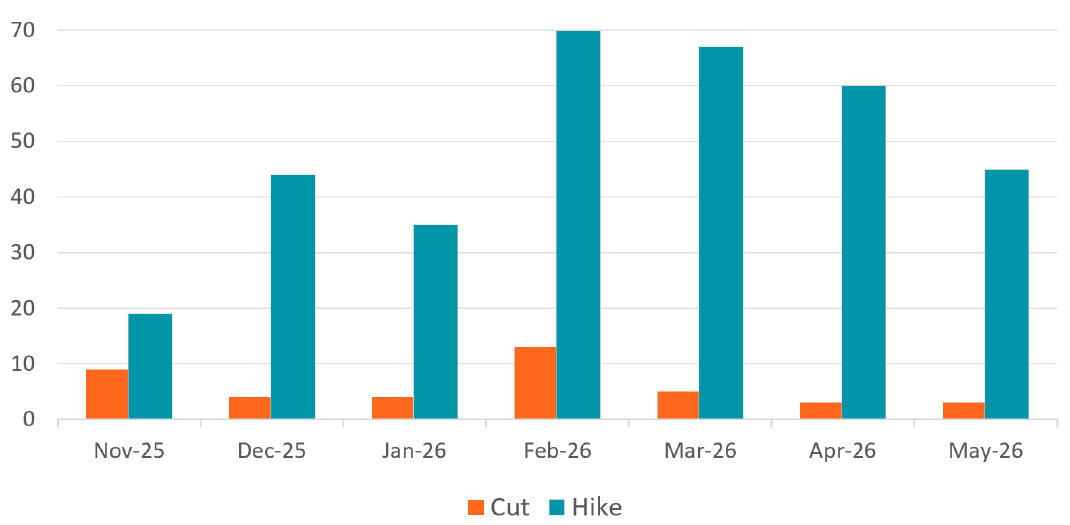

Fixed rates have become considerably less competitive relative to variable rates following months of increases. At the start of the year, 83 lenders on the Canstar database offered at least one fixed rate below 6%, compared with just two today.

Lenders that have changed at least one fixed rate in the last seven months Source: Canstar.com.au

Source: Canstar.com.au

More than 40 lenders still offer at least one variable rate below that threshold. Across the Canstar database, 90% of lenders' lowest rates are variable, with the gap between fixed and variable currently averaging 0.26 percentage points.

| Big four banks + Macquarie lowest fixed rates | |||||

|---|---|---|---|---|---|

| CBA | Westpac | NAB | ANZ | Macquarie | |

| 1-year | 6.49% | 6.44% | 6.49% | 6.34% | 6.19% |

| 2-year | 6.34% | 6.34% | 6.54% | 6.29% | 6.14% |

| 3-year | 6.59% | 6.54% | 6.49% | 6.49% | 6.09% |

| 4-year | 6.64% | 6.69% | 6.49% | 6.54% | 6.29% |

| 5-year | 6.79% | 6.69% | 6.49% | 6.59% | 6.29% |

| Source: Canstar.com.au. Rates based on owner-occupier fixed rate loans. LVR requirements apply. | |||||

Canstar's analysis indicates that an owner-occupier with a $600,000 debt and 25 years remaining who chose the lowest available one-year fixed rate of 5.99%, rather than the lowest variable rate of 5.69%, would fall behind if the cash rate remained on hold for 12 months.

If, however, the Reserve Bank of Australia delivered two further hikes — as Westpac forecasts — fixing would marginally outperform, but by only $314.

"If rates stay on hold, the move is likely to cost them more," Tindall said. "If rates rise further, fixing could potentially save money, but probably not enough to be considered a game changer.

"For many borrowers, the appeal of fixing isn't about securing the lowest rate, but instead, locking in certainty. If that's you, spend time looking for a competitive offer before you lock in, and as always, read the fine print so you're fully across the limitations of a fixed rate mortgage."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.