Major banks roundtable discusses key industry issues

Communication, resilience and an ability to adapt to a changing market and the needs of broker partners are the key themes that emerged from MPA’s 2023 Major Banks Roundtable.

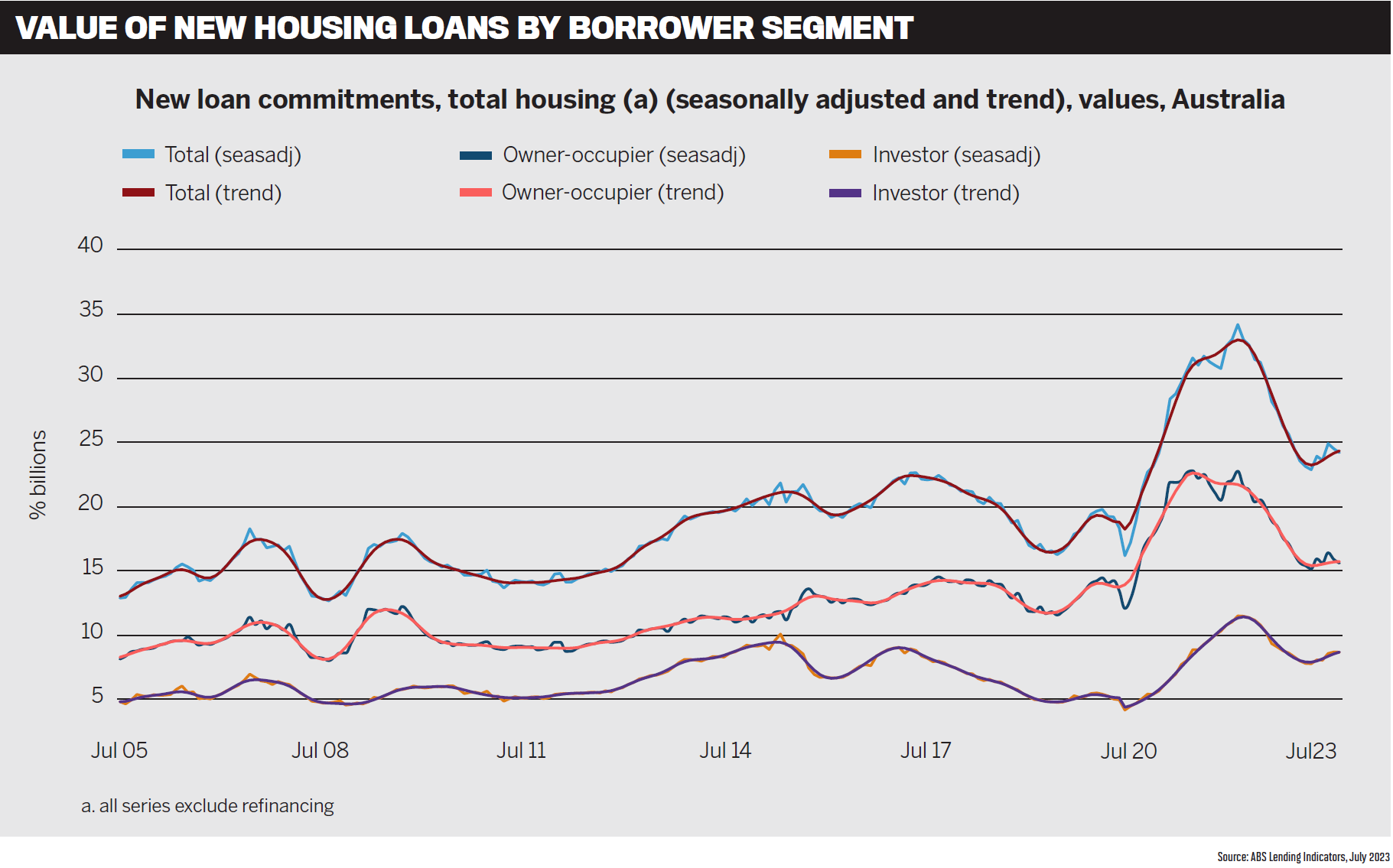

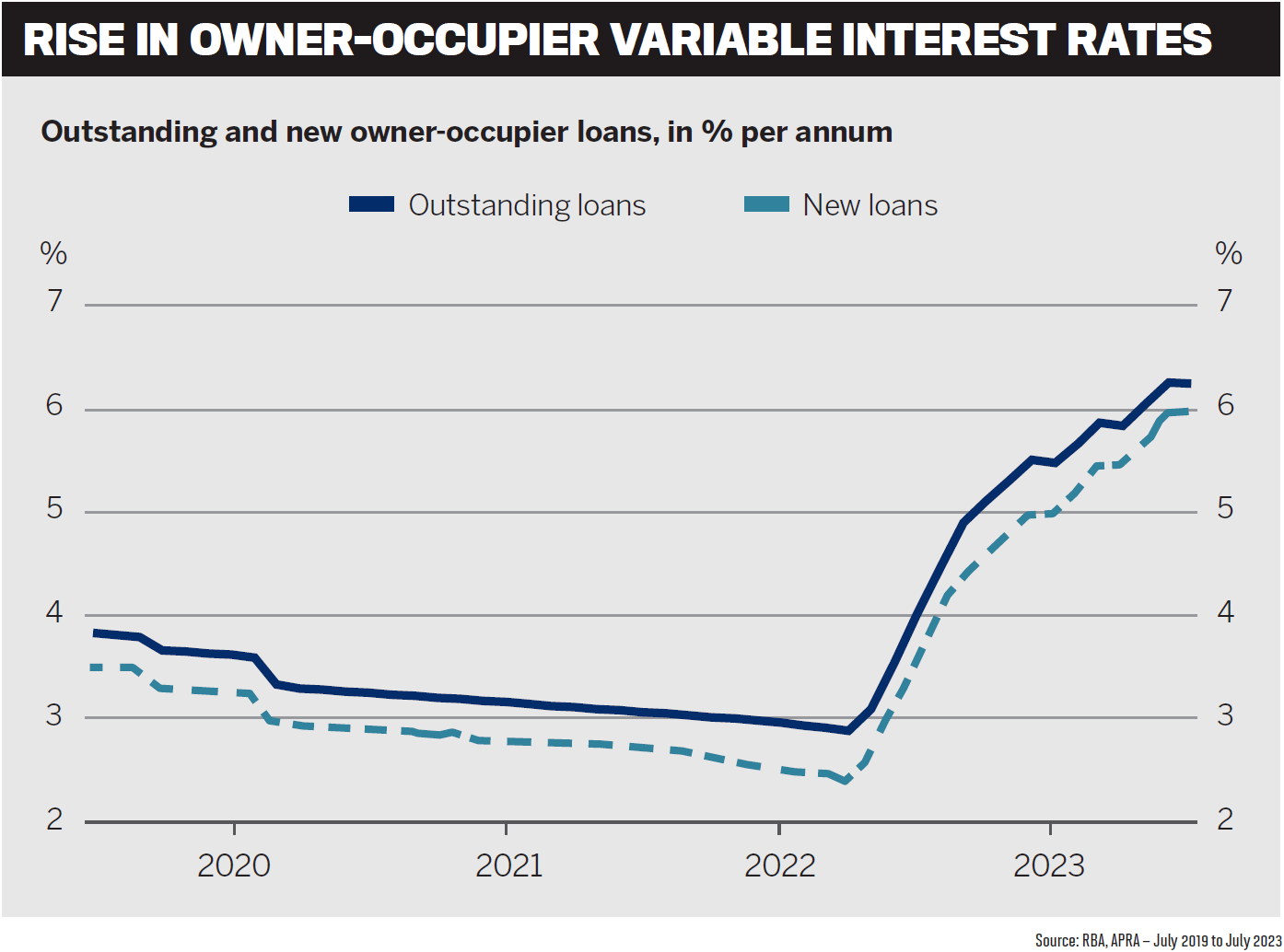

It’s been a number of years since banks, brokers and homeowners have faced such a challenging economic period, with the Reserve Bank of Australia lifting the official cash rate 12 times in little over a year.

On top of higher interest rates, when you throw into the mix rising inflation, labour shortages, supply chain issues and a flat property market, it’s no surprise that some mortgage holders are feeling a bit anxious about what the future holds.

There has also been intense competition among banks to acquire new home loan customers in a slower market, and to hold on to existing clients. Brokers have been inun- dated with refinance requests, often driven by attractive cashback offers.

But inflation has since eased; it’s looking likely that the RBA is nearing the end of its rate-hiking cycle; and while mortgage holders are increasingly feeling the pinch, they’re proving resilient, and most are still in good shape. The property market is also on the rise as spring selling season gets underway.

Banks have either reduced cashbacks or got rid of them altogether. They have also adjusted their clawback policies to provide a fairer system for brokers when it comes to commissions.

The changing market and the so-called ‘mortgage cliff ’; increased communication with brokers and customers; the reduction in cashback offers; clawbacks, and technology were all topics up for discussion at this year’s Major Banks Roundtable, held at Silks restaurant at the Crown Sydney.

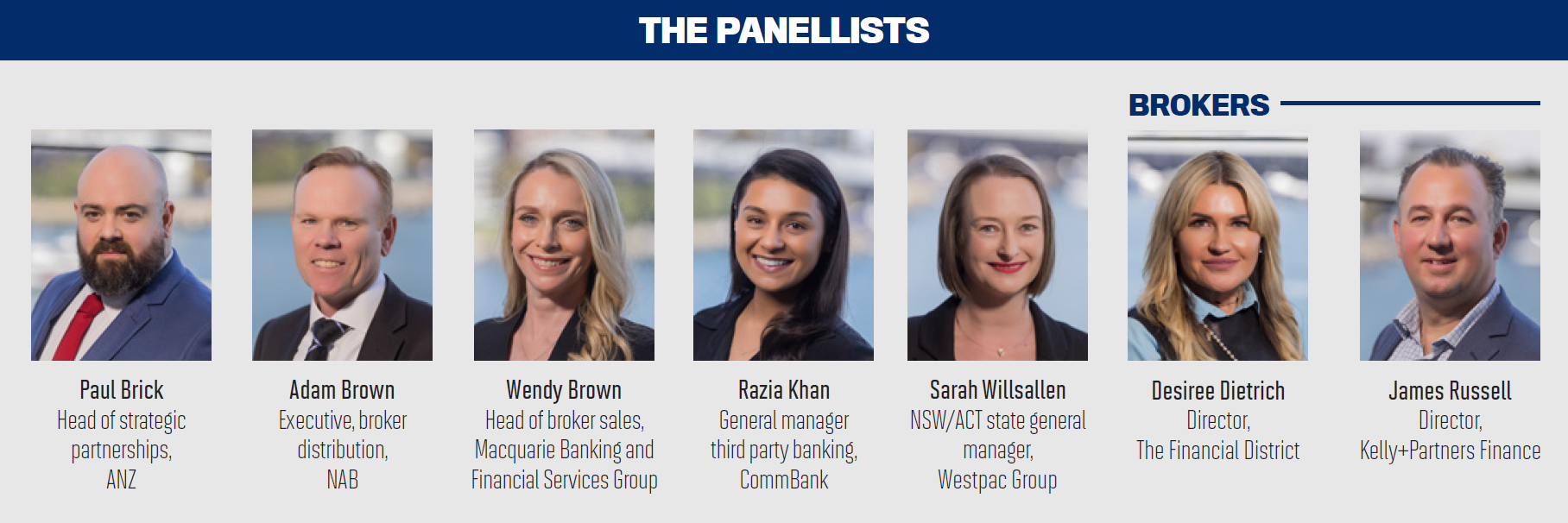

Roundtable participants included Paul Brick, head of strategic partnerships, ANZ; Adam Brown, executive, broker distribu- tion, NAB; Wendy Brown, head of broker sales, Macquarie Bank; Razia Khan, general manager third party banking, CommBank; and Sarah Willsallen, state general manager NSW/ACT – mortgage broker distribution, Westpac Group. Representing brokers were Desiree Dietrich, director, The Financial District, and James Russell, director, Kelly+Partners Finance.

Q: In the last 12 months, Australia has experienced the most rapid interest rate rises in decades. How have major banks responded and adjusted to this challenge and supported brokers and their customers? What does your data show about levels of mortgage stress among customers?

Wendy Brown of Macquarie Bank started the discussion, saying that Macquarie Bank had been in a positive position, given that it had a lower-LVR loan book compared to the broader industry.

“So that’s set our customers up for success,” she said. “And also, in combination with having the lowest debt-to-income for quite some time, we haven’t seen any material impact on our book.

“We’ve seen an increase in phone calls, but actually not an increase in home loan stress.

We’re really seeing a trend of our customers coming to us early and having great conversations, or their brokers are encouraging them to come to us early.”

Brown said customers were asking about their options, more so than asking for help. They also had high levels of savings, and unemployment was low.

Sarah Willsallen (pictured below) said it was a similar situation at Westpac Bank.

“Default and delinquencies actually remain low, the economy is still relatively strong, and unemployment is low,” she said.

“We absolutely recognise that there’d be customers impacted by cost of living increases, and it’s a big concern for them.”

Westpac encourages any customers who are concerned about their financial situa- tions to reach out, Willsallen said.

“There are so many options – all of the lenders have amazing assist teams that are there to help; there’s so many things that we’re able to do. The earlier customers and their brokers engage with us, the more options we’ve got and the more we can support them.”

In terms of communicating with brokers, she said the main message was that they should work with the bank earlier to help support customers.

“As part of the fixed rate roll-off, we’ve been really proactive in making sure that customers rolling off are getting competi- tive pricing and good outcomes without needing to jump through hoops or do lots of extra steps. I think that proactivity and trying to help ease the transition is really important.”

Willsallen said customers should be aware of when they will be rolling off their fixed rates and how to plan for that. Westpac offers calculators and other tools to help them budget.

“But equally, the biggest thing

Adam Brown (pictured below) said NAB had proactively reached out to more than half a million customers since May 2022 to discuss their financial wellbeing.

“In the first quarter this year [we reached out to] about 10,000 home loan customers, and what we found is where we’ve engaged early, 90% of customers are back on their feet and in a better situation within 90 days.”

Brown said around 50% of NAB home loan customers were due to roll off low fixed rates on to variable rates soon, and the bank had been keeping a close eye on these customers and reaching out to those who might need extra support.

“While interest rates have gone up, there’s a large cohort that haven’t had significant impacts yet,” he said. “We’re [working] proactively with customers on fixed rate rollovers, interest-only rollovers – and helping them understand what they’re about to head into is an opportunity to provide significant support.”

Echoing Willsallen’s comments, Razia Khan (pictured below) said CommBank was also seeing similarly low delinquency rates.

“We went out and really looked at our hardship solutions in particular to make sure that we had a broader suite,” she said.

“We’ve introduced more solutions, ensuring that brokers and their customers are reaching out to our hardship team to discuss different options.”

Khan said more than a third of CommBank customers were more than two years ahead on their mortgage repayments, with 78% having made repayments in advance.

Broker James Russell (pictured below) from Kelly+Partners Finance asked how quickly banks had seen savings balances drop and whether it was something they tracked quarter-on-quarter.

Paul Brick (pictured below) from ANZ said the bank’s retail book was higher than it was pre-COVID. “Many home loan customers at ANZ are ahead in their repayments. Since the start of the pandemic, they’ve built up their savings and have increased the equity in their homes as well.”

Many fixed rate customers had already rolled off their rates at ANZ, Brick said.

“The important thing to note is that all those customers were assessed with a buffer. Many have now gone off their fixed rate, and there’s been no material change to delin- quency levels.”

Brick said it showed that Australians were managing their mortgages proactively.

Wendy Brown said borrowers had been vocal about picking up the phone early and contacting the bank if they encountered problems. Unlike earlier times when telling the bank you were behind on your repayments was a social taboo, she said a great cultural change had occurred when it came to customers opening up to their brokers and the bank.

Adam Brown said banks had undergone a “trial run” during COVID, when they had now they’re saying, ‘we can’t afford this; let’s sell it and downsize or sell and rent for a while’, which I’ve had a few customers do.”

Desiree Dietrich (pictured below), of brokerage The Financial District, said some clients had told her that instead of letting their mortgages suffer, they would cut back on spending in other areas – for example, by sending their children to public schools instead of private schools.

“They’re changing the way they live their lives,” Dietrich said. “Quite a few of them are selling investments. When interest rates were very low, they bought two or three invest- ment properties, but now they are having to chip in with their own money, and it’s too stressful. So they’re selling one or two.”

Q: Thousands of homeowners are set to come off low fixed rates and face much higher mortgage repayments in the coming months. What steps have you put in place to ensure brokers and customers are prepared and can handle this big change?

“We talked about early engagement before from customer to bank; the early engagement from bank to customer was really useful as well,” he said.

ANZ also offers a range of resources directly to brokers and their customers, such as a financial wellbeing program.

At NAB, Adam Brown said the bank reaches out to fixed rate customers at 90, 45 and 30 days before their terms end, but our call to action is for customers to contact their broker”.

“The brokers also receive SMS messages from us to let them know we are engaging with our customers. We recognise that brokers have a key role to play here – they introduced us to that customer. It’s also an opportunity for them to help support that customer and maintain that contact, and suits the relationship they have.”

Brown said NAB was retaining about 85% of customers who rolled off a fixed rate, and he believed it had a lot to do with early engagement with both the broker and the customer.

“If they know what they’re heading into and you’re able to help before they get to the roll-off, they’re much more comfortable with what the options are.”

Russell asked Adam Brown if NAB customers were rolling off onto variable rates or fixed. Brown said that earlier on it was fixed, but it had quickly moved to variable rates now because fixed rates had risen above variable rates.

Khan said that in her previous role at CommBank, she led the fixed rate customer retention strategy.

“We’re aiming to contact all of our fixed rate customers at 90- and 45-days pre-expiry and post roll-off,” she said. “We’re ensuring that we’re communicating with our brokers to let them know that we are having these conversations with our customers.”

Communications have also been sent out to customers, encouraging them to contact the bank.

“We also aim to add value back to customers through ‘Yello’ – our CommBank Rewards program which offers customers discounts and cashback on their everyday spend for things such as groceries, fuel and food delivery at some of Australia’s most loved brands,” Khan said. “As of July, CommBank customers had saved $30 million through our CommBank Rewards cashback program.”

Willsallen said the biggest thing Westpac had done was to ensure the roll-off rate provided a good, competitive discount up front without the customer needing to act.

Dietrich praised Westpac’s approach and said a Westpac representative rang her each month to say, “your clients are coming off their fixed and we’re offering them this”. She said the discount they were offering was unbeatable. “And they allow us to phone up the clients and say, ‘we got it for you’. This is making the broker look good.”

Willsallen said Westpac wanted to preserve the role the broker plays in engaging with the customer, and in that transition, as the rate cycle changes.

Russell said it was good for banks to keep brokers up to date on what’s happening with clients. “Some of the banks have better digital access to viewing that loan information online than others,” he explained.

“With some of them you’re flying blind unless you call the bank. If the customer fixed over the phone directly to the bank, I’ve got no record that ever happened unless someone tells me.”

Wendy Brown (pictured below) said Macquarie Bank is able to quickly add information into the broker portal so brokers can see not only the current fixed rate but also the expiry date. This is helpful for brokers who have brought in customers on a variable rate but have no visibility if a customer has called the bank and moved to a fixed rate.

“We also have the ability for a rate request to go straight from the broker immediately, and that’s been very successful as well,” she said.

“Brokers get credit for being able to proactively ring a customer when their rate expires – it helps your brand and your relationships, as well having accurate data. The feedback has been fantastic.”

Dietrich said this feature, also offered by CommBank, was really helpful.

Q: The home loan market is highly competitive as lenders chase refinance opportunities. A number of banks have dropped cashback offers, which has been welcomed by brokers. What are your thoughts about cashbacks, and how do you balance the needs of existing customers with the need to acquire new customers?

Brick said it was important to “have as dynamic an industry as we possibly can” that offers a range of options.

He said this was where the broker “really came into their own” in making recommendations to customers.

“Customers and brokers do like aspects of the cashback offering,” Brick said. “It will suit different people at different times, but I think as a guiding principle, competition, diversity and options are important.”

ANZ also has a $3,000 offer for first home buyers as the bank looks to balance refinances with purchases, and support those seeking to enter the market.

Willsallen said mortgage competition was intensely fierce, with a lot of lenders competing actively for a small pool of lending. “The winners are the customers,” she said. “It keeps us all focused on delivering a great offering – a mix of price and proposition and service.”

This was the role brokers played – by making sure they could guide customers through different choices of lenders across the market. Willsallen said this had helped brokers grow to achieve the market share they enjoy today.

Khan said CommBank had removed cashbacks on 1 June, and while refinancing activity had softened, the key reason for no longer offering cashbacks centred on being able to create longer-term relationships with customers.

“We know refinance activity is hot in the market. We’ve introduced a ‘Yello’ customer recognition program to all of our eligible home loan customers – we’re trying to give our customers more back, and hopefully that creates a longer-term relationship with CBA.”

“It depends on the market at the time and what customers are looking for,” he said. “The significance of creating long-term relationships with customers is at the heart of what we’re doing, particularly when it’s been a high-refinancing market.”

NAB wants to help support existing customers coming off fixed rates and interest-only terms, and the idea is to achieve a better balance between acquisition and retention by removing cashbacks and complexity.

“Having short-term incentives and long-term incentives, it can be really hard for a customer to choose between those. That’s where the broker proposition does become really important, and good brokers can give the right advice,” Adam Brown said.

Unlike the other majors, Wendy Brown said Macquarie had never offered cashbacks, for many reasons.

“We just didn’t think it was the right thing for our proposition, like you mentioned – long-term customers. We’ve always tried to be very transparent on pricing, putting it into the front card,” she said.

Russell said he was glad lenders had cut back on cashbacks because he was also keen on developing long-term relationships with customers.

“I don’t want to see customer churn just to get a short-term incentive. I’d prefer the banks reinvest back into their rates and keep them as low as possible in the longer term, than doing a short-term sugar hit and then boosting the back-book rate later on.”

Dietrich said her brokerage liked cashbacks because they were a “nice sweetener”. “They’re not the reason to do the deal,

but it’s quite nice at the end, once you’ve refinanced and you can tell them there’s going to be $4,000 in your account, and the clients are really thankful.”

But she said cashbacks did pose some problems. For example, some clients wanted a $4,000 cashback from ANZ and then six months later they sought to refinance with another bank to secure a $2,000 cashback.

“You know that if you don’t do it [refinance the loan], the client would just go to another broker or go direct, so then you get clawed back.”

Q: Broker question from Desiree Dietrich: Brokers are experiencing very high rates of clawback due to sales of properties. Is there anything further that can be done on this issue to make it fairer for the broker involved? Changes to clawback policies?

Dietrich elaborated on her question, saying that clawback was a real bugbear for brokers. “I totally agree brokers shouldn’t churn clients, and if you’re a churning broker, then you deserve to be clawed back.”

Dietrich’s brokerage budgets approxi- mately $10,000 per month for clawbacks, mostly because clients are selling their properties. “It’s annoying because you’ve done all that work – the client that claws you back is going to be the client that you’ve worked the hardest to get; that’s just Murphy’s Law.”

She said it was great that lenders had shortened their clawback period because two years was just too long.

“Sometimes you get to 21 months and there’s a clawback. Then you’ve got to do another deal to make up for that, so you’ve essentially written two deals.”

“Is there any movement on clawback, especially with sales of properties? Is there anything that you guys are thinking about?” Dietrich asked.

Willsallen said Westpac had recently reduced its clawback period from 24 months to 18 months, which Dietrich said was welcome move.

“We want to be a good partner to brokers,” Willsallen said. “We’ve had feedback, and we also looked at the market and recognised that we wanted to be aligned to where a lot in the market were.”

Brick said ANZ also has a tiered total clawback period of 18 months, and this policy has been one of the strongest in the market for many years. “We’re comfortable with where it sits at the moment,” he said.

Significant regulatory oversight on broker commissions, including clawback, was a focus of the banking royal commission and Treasury, Brick pointed out. “Whether we want to revisit that is something we would need to consider collectively, as an industry.

“With brokers eligible to receive an upfront commission, the banks are actually getting less in the first year. If you change one aspect, then other aspects might come into play as well. It’s a difficult one, but I take your point, Desiree – brokers are doing a lot of work,” Brick said.

“We’ ll get a client phoning up saying, ‘I’m in a really bad spot; I’m going to have to sell’,” she explained.

“You’re thinking we only did the deal six months ago, and you know you’re going to get clawed back. You have to think of the client’s best interests, and you have to give the advice. If you see they can’t afford it [their property], you can’t talk them back from the edge on that. You just have to just suck it up.”

She said it was especially hard for younger, new-to-industry brokers who weren’t earning a lot in commissions and then had to cope with a significant amount of clawback.

“When you’ve been in the industry for a long time, you’ve got good trail, it’s not the end of the world – you just wear it as a loss; but for new brokers it must be very tricky.”

Khan said CommBank had just extended its clawback policy, which would take effect on 1 October. “The biggest change that we’ve made is we had 12 months at 100% [clawback], the next six months at 50%, irrespective of which month you’re refi- nancing. We have extended that clawback to 24 months, but it’s a gradual decline.”

She said the change to clawback policy was aimed at fostering longer-term rela- tionships with customers and brokers, while also adding back to the customers.

Dietrich said there was a time when CommBank used to reverse clawbacks if brokers could prove there was a property sale. She asked if this was still in place.

Khan said she had reviewed clawback exceptions and took an approach based on the circumstances that were presented.

Adam Brown said NAB also had a 50% clawback policy all the way through to 24 months from month 12. He said there had been a lot of loan churn, and the average loan term had come down, driven by greater levels of refinancing; rolling-off of two-year fixed rates; and cashbacks.

“This has brought the issue of clawbacks much more to the fore, because there’s a shorter lifespan and more churn. We’re looking at clawbacks constantly.”

Dietrich said she wondered if the banks should have to take on all the responsibility when it came to clawbacks. “Maybe there’s something we could tax-deduct as a clawback cost because you’re still getting the cost of two deals for the same amount of money, and you’re only earning one. Maybe the ATO could come to the party,” she said.

“Maybe the ATO could allow brokers a ‘cost of clawback’ deduction to cater for the fact that brokers have done a lot of work on a deal and had their income taken away on it. It costs money and time to bring a loan to settlement, and we should get some relief inside our tax returns if the commission gets clawed back.”

Russell said he would be happy to trade off a refinance clawback against a sale clawback. “I’d be happy to extend a refinance clawback to three years if we could do a sale clawback to one year. I’m not a broker who churns, so I wouldn’t be worried about pushing that one out to three years.

“In PEXA, you can see whether it’s a refinance or a sale very, very easily, so it would be easy for the banks to track that.”

Q: Broker question from James Russell: My question is on the use of technology to enhance post-settlement services for brokers. What are lenders doing to provide brokers with better access to their client loan information online and streamline loan administration using digital pathways?

Russell said some banks were better than others at providing portals so brokers could see their loan book, view interest rates and get data on their clients.

He was keen to know what the banks were doing to digitally enhance back-office processes such as loan switches and fixing loans, rather than having to fill out paper forms and do wet-ink signatures.

“Can we do that through a portal? What’s each bank doing with regard to that?” Russell asked.

Willsallen said currently Westpac did not have the ability to see a broker’s back book on its portal, but it was “definitely something we’re interested in exploring”.

“It’s about balancing the other things we’re also trying to invest in to improve the broker and customer experience,” she said.

“Our principle is absolutely, we want to be a digital-first bank. We want to be simpler, easier and faster to do business with, so every time we can take a form out of a process, we think it’s a really good thing, and we’re certainly keen to do it.”

Willsallen said Westpac was also investing in making further improvements, including to its broker portal. It recently fixed the portal password reset issue and made several other enhancements.

Much of the bank’s tech efforts in the last few years have focused on a new mortgage originations platform, which is now up and operational. “We now have one common platform across all brokers and across the bank,” Willsallen said.

Brick said ANZ was “continuing to pedal really hard towards digitising our processes and a digital home loan, and we’re engaging with aggregators to design elements of that”.

Brick said brokers having access to a digital loan proposition was really important to ANZ, especially considering the percep- tion that digital loans could compete directly with brokers for clients.

“We’ve made some amazing strides when it comes to technology, and we’ve still got a bit of work to do, but it’s exciting.”

At CommBank, Khan said the bank had launched its refreshed broker platform and tested it using a pilot group of brokers.

“CommBank recently launched another refreshed tool as part of our investment in upgrading the CommBroker Portal. The updates make it simpler and easier to track your applications and provide greater visibility and control of inflight applications. Mobile optimisation means this is also now accessible on the go.”

Khan said CommBank had announced that she would oversee the technology teams as part of her role.

“We’ve got dedicated technology teams focused on improving the broker proposi- tion, whether that’s our commission system, Your Loans, our CommBroker portal or Your Applications. How we evolve will depend on direct feedback from our brokers.”

Dietrich agreed that the process with CommBank was very easy now.

At NAB, Adam Brown said the bank had just refreshed its broker portal to bring a fresh new look and support for customers, and there was more work in the pipeline to further improve functionality.

New features included an instant repricing tool, which enabled brokers to just press a button to reprice loans for existing customers and “there was nothing else you have to do”.

“The other thing that’s coming to our industry, which is great and that we support, is digital documents delivered to customers,” he said.

Adam Brown said features such as DocuSign and Digital ID provided accuracy, without the need for “reams and reams” of paperwork. This type of technology would continue to evolve and would have a key impact on brokers and their customers.

At Macquarie Bank, Wendy Brown said the broker team had learnt how to look after brokers when they needed it. The bank’s broker portal had been very successful, but second-order questions were now being worked on.

“The broker portal will answer lots of questions on where your application is in flight, what the current pricing is – but it’s the next action we’re up to now.”

She said it was now about monitoring customers in the portal and understanding what other problems needed to be resolved.

“All of what we do is based around the data. So if you look at digital ID, we are not only solving for digital ID, we are also solving for name accuracy.”

Brown explained that because Macquarie Bank was able to get loan documents out on the same day, if brokers had misspelled a name, the documents would have to be recalled four hours later.

“I think that’s really changed our mindset about digitising everything,” Brown said.

She pointed out that if banks didn’t really invest in the process behind the system, then the technology was never going to solve all the problems.

“Whether it’s the broker help centre or broker portal, our technology is always on; you just see it’s constant, and our goal is to be much more like the leading technology companies like Amazon and Google – you’re just going to notice the difference.”