Mortgage brokers are required to have AFCA membership. But what is AFCA and how does it benefit brokers and brokering firms? Read on and find out

The Australian Financial Complaints Authority (AFCA) was formed to assist consumers and small businesses in resolving disputes with financial firms. The aim is to come up with a fair and swift solution for everyone involved

The law requires all types of businesses that offer financial advice and services to get AFCA membership. These include private lenders and mortgage brokerage firms.

But how exactly does AFCA operate? How can businesses apply for membership? How much does AFCA membership cost? We will answer these questions and more in this guide.

What is AFCA?

AFCA is an independent complaint resolution scheme authorised by the Minister for Revenue and Financial Services in November 2018. It provides dispute resolution services for consumers with unresolved complaints against financial and credit firms.

AFCA replaced the three previous external dispute resolution schemes:

- Financial Ombudsman Service

- Credit and Investments Ombudsman

- Superannuation Complaints Tribunal

The goal is to offer consumers and small businesses a “one-stop shop” for resolving complaints about:

- credit, loans, and finance

- investments and financial advice

- banking payments and transactions

- insurance

- superannuation

As part of their general conduct obligations, all businesses that hold an Australian Financial Services Licence (AFSL) or Australian Credit Licence (ACL) are required to get AFCA membership.

Who can lodge a complaint under AFCA and against whom?

Complaints can only be made against an AFCA member. AFCA also imposes eligibility requirements for those who can make a complaint. A complainant is considered eligible if they are:

- an individual

- a small business with less than 100 staff

- a registered charity, regardless of size

- a club that does business and has less than 100 employees

Consumers can use the search tool on AFCA’s website to find out if a financial firm is a member.

What types of complaints does AFCA consider?

AFCA aims for a fair resolution of disputes between consumers and financial service providers. Some common complaints that the scheme can help resolve include:

- breach of responsible lending duties

- misleading information on financial products

- inability to provide support for financial hardships

- denial of an insurance claim

AFCA, however, doesn’t handle all types of complaints. Some issues that the scheme doesn’t consider are:

- lender’s refusal to provide a loan because of a borrower’s credit risk

- general performance of an investment

- complaints concerning professional accountancy services, unless these are provided along with a financial service

- small business credit facility worth more than $5 million

If AFCA sees that a complaint may be better handled by the courts, it may refuse consideration. It also doesn’t consider complaints that have been previously dealt with. In addition, it doesn’t handle complaints where the complainant hasn’t suffered any loss or has been properly compensated.

AFCA notes that it “will not exercise our discretion to exclude a complaint lightly.” It points out that there must be compelling reasons for a complaint not to be considered.

AFCA also recommends that consumers raise their concerns with the financial firms first to allow them to resolve the complaint directly.

Which financial firms receive the most complaints?

Despite comprising the largest portion of AFCA membership, mortgage brokers and mortgage brokerage firms aren’t among the list of businesses receiving the greatest number of complaints.

Here are the top five from the last financial year:

AFCA members with the highest number of complaints – 2022-2023 financial year

|

Rank |

Financial firm |

Number of complaints |

|

1 |

Banks |

36,668 |

|

2 |

General insurers |

22,113 |

|

3 |

Credit providers |

9,837 |

|

4 |

Superannuation fund trustees/advisers |

5,680 |

|

5 |

Underwriting agencies |

3,567 |

All firms in the top five have seen a significant jump in the number of complaints from the previous financial year. Banks, general insurers, and credit providers have also been consistently in the top three since AFCA’s inception.

From logging 73,272 complaints during its first year in 2019, AFCA had a record-breaking 100,000 complaints in 2023.

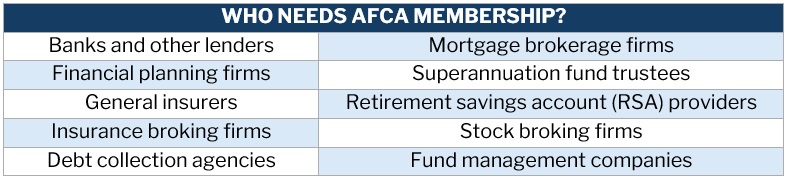

Who is required to be an AFCA member?

All businesses that require a financial services licence or credit licence are required by law to apply for AFCA membership. Businesses that hold these types of licences are also referred to as financial firms. These include:

Businesses that aren’t required to become members can also join AFCA to show their accountability and commitment to fair dispute resolution.

AFCA membership breakdown

At the end of the 2022-2023 financial year, AFCA had almost 45,000 members. The number is a 20% rise from around 37,500 in its first year. Almost four-fifths (77%) of current members are authorised credit representatives. The rest consists of financial firms and related service providers. The bulk of AFCA members are small and mid-size businesses.

Mortgage brokers comprise the biggest group, numbering more than 2,000. Financial advisers and finance brokers follow at around 1,480 and 1,420 members, respectively. Rounding out the top five are credit providers with about 720 members and insurance brokers with 540.

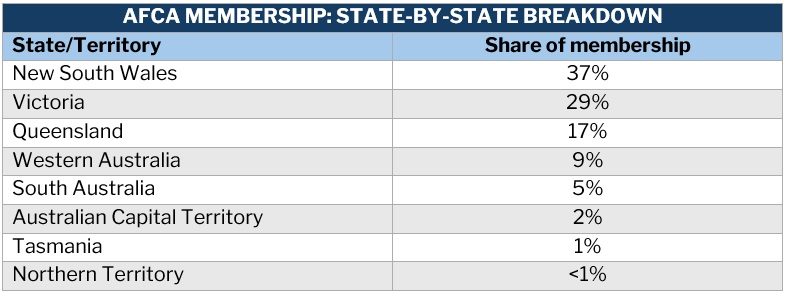

In terms of location, New South Wales is home to the highest number of AFCA members. It is followed by Victoria and Queensland.

Here’s a state-by-state breakdown of AFCA membership across the country:

How can you apply for AFCA membership?

There are two main types of AFCA memberships that businesses can apply for:

1. Authorised credit representative membership

Also called ACR membership, this is open to individuals and businesses appointed by a credit licensee or aggregator to engage in credit activities.

If a business needs both an individual and a company membership, it will need to submit separate applications.

2. Licensee membership

This applies to financial firms that require AFCA membership as part of their licensing conditions. These include businesses holding AFSL, ACL, or limited financial services licence.

Banks, mortgage lenders, and mortgage brokers fall into this category.

AFCA membership is also open to other financial service businesses that want to provide their clients access to AFCA’s dispute resolution services. These can include:

- annuity providers

- approved deposit funds

- consumer data rights participants

- life policy funds

- regulated superannuation funds, excluding self-managed superfunds

- sandbox participants

- unlicensed product issuers

Businesses can apply for membership on AFCA’s website. Applicants will also be asked to pay a corresponding membership fee. Processing takes between five and seven days. Once approved, AFCA will send an email confirmation. This contains information on the dispute resolution process and how businesses can manage their membership.

AFCA will also provide a membership number. Membership certificates can be downloaded through the membership portal called Secure Services.

How much does AFCA membership cost?

For those applying for a licensee membership between 1 January 2024 and 31 March 2024, AFCA charges an annual membership fee of $191.06. This amount includes a 1.75% surcharge. Licensees applying from 1 April 2024 to 31 December 2024 will be charged $95.52.

Credit representatives, meanwhile, are required to pay a one-time fee of $67.13 for AFCA membership.

Here’s the complete fee matrix for this year.

AFCA membership fees

|

Membership type |

Application date |

Membership fee |

With 1.75% surcharge |

|

Licensee |

1 January 2024 to 31 March 2024 |

$187.77 |

$191.06 |

|

1 April 2024 to 31 December 2024 |

$93.88 |

$95.52 |

|

|

Credit representative |

1 June 2023 to 31 May 2024 |

$65.98 |

$67.13 |

Members who applied from 1 June 2023 to 30 September 2023 were charged $382.12, including surcharges. Applicants from 1 October 2023 until the end of the year paid $286.57.

These fees, along with user charges and complaint fees, serve as AFCA’s funding.

In July 2022, AFCA transitioned to a new funding model that adopts what it calls a “user pays” approach. Under this system, firms that frequently receive complaints pay a fair share towards the scheme’s services. This means that those with few to no complaints pay low fees.

According to AFCA, the new system is designed to be “efficient, sustainable, responsive, and support early resolution of complaints.”

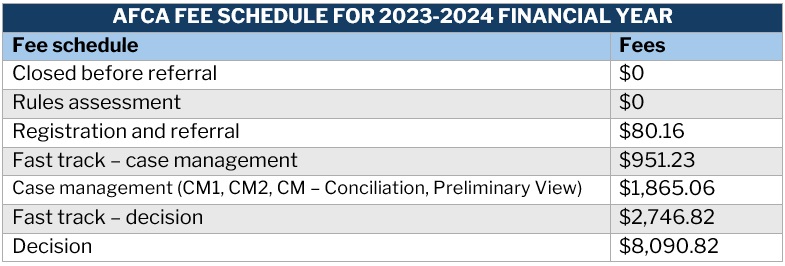

Here’s the fee schedule for the current financial year. All fees include a 10% GST.

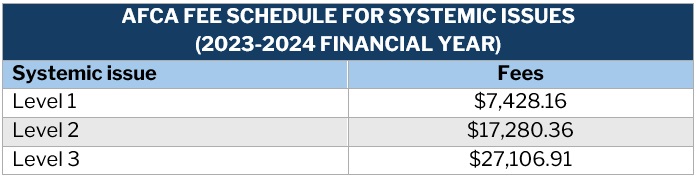

AFCA also charges a complaint fee for “systemic issues.” AFCA defines this as an issue that’s likely to affect one or more consumers or small businesses, apart from the complainant.

Here’s the fee schedule. These amounts don’t include GST.

AFCA’s services are free for consumers and small businesses.

How can you renew your AFCA membership?

AFCA membership renews automatically on the first of August every financial year. Members have until the last day of July to pay the annual membership fee.

For firms unable to pay by the due date, membership will still be renewed. However, they won’t receive their membership certificates until they have settled the fee. Failure to pay the membership fee can lead to expulsion from the AFCA.

Members can settle the renewal fee through AFCA’s online payment system. After payment, their membership certificates will be emailed within five business days.

For businesses that want to withdraw their AFCA membership, they can do so through the Secure Services portal. If they cancel their membership on or before 31 May, they won’t be charged a renewal fee.

How do mortgage brokers benefit from AFCA?

Although the scale seems to be heavily tipped towards the consumers, AFCA membership presents several benefits for financial firms, including mortgage brokers. Here are some of them:

Access to expertise

AFCA is supported by a team of industry and legal experts. These include ombudsmen and adjudicators. These decision makers work independently to come up with a fair resolution for all financial complaints.

Professional development

AFCA membership allows businesses to enhance networking opportunities through several professional development events. AFCA hosts conferences, industry forums, liaison group meetings, and webinars to help members connect with others in the industry. These events also help members gain a deeper understanding of effective dispute resolution.

Knowledge and resources

AFCA members can access a range of resources, including digital publications, guides, and eLearning courses. These are designed to help them understand the AFCA process better.

Membership portal

The Secure Services portal gives members access to several customised resources, including video tutorials, process information, and statistics. They can also use the portal to manage complaints and update their membership details.

AFCA membership is an important part of being a mortgage broker. If you think this is a career worth pursuing, this guide on how to become a mortgage broker in Australia can help.

What are the other benefits of AFCA membership? Is the scheme too heavily tipped towards consumers and small businesses? Let us know what you think in the comments.