Jump to winners | Jump to methodology | View PDF

MPA’s Brokers on Non-Banks 2023 survey reveals that the broker-lender relationship is evolving, as evidenced by a shift in what brokers value most about the best non-bank mortgage lenders.

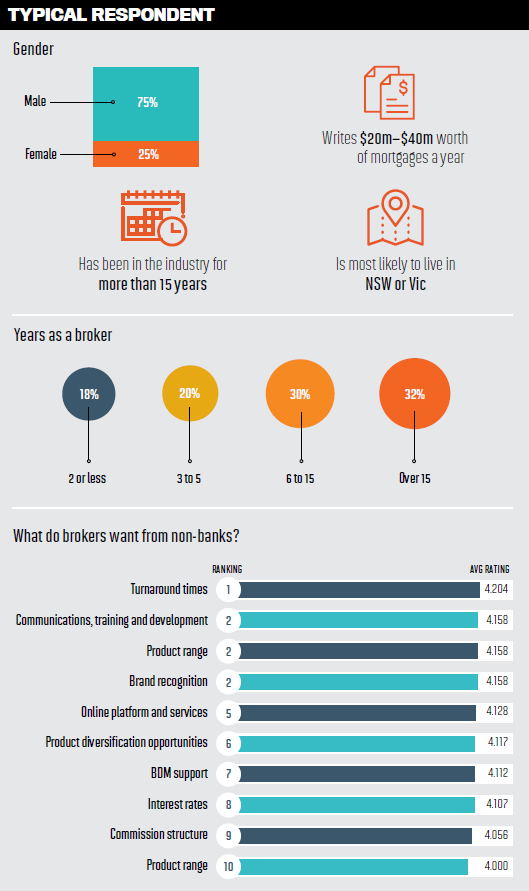

The broking community rated non-banks’ performance across 10 metrics, elevating those with the highest scores to the winner’s podium.

This year’s data suggests the medallists and runners-up have moved the yardstick forward on their overall competitiveness, which has strategically positioned them to climb back from declining market share and, as one broker said, “keep the big four on their toes”.

Non-bank’ achievements are particularly impressive, given that a confluence of factors has made it a difficult market for them, says Chris Slater, AFG’s head of sales and distribution. “For many, their only distribution channel is the third-party channel, so they are 100% committed to ensuring brokers have a wide and diverse range of products to better serve everyday Australians,” he explains. “In addition, their sales teams’ number one focus is trying to deliver a unique service proposition to stand out from the crowd. That competition is good for consumers.”

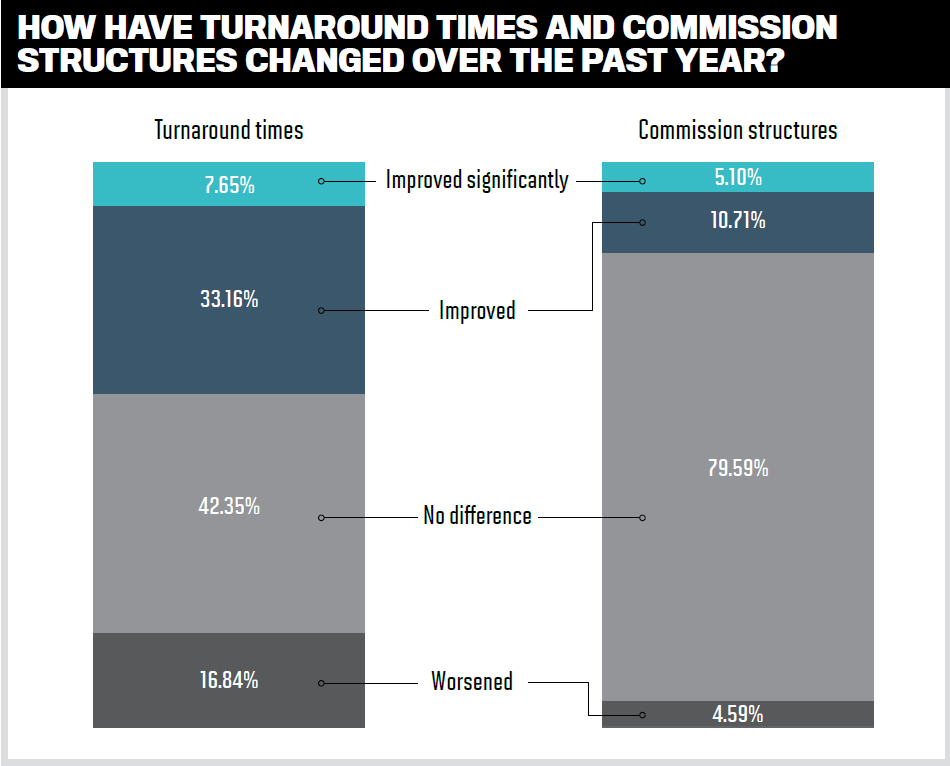

Brokers consistently identify turnaround times as their top concern, and a majority observed improvements, including to the speed and efficiency of non-banks’ systems and processes:

In a dramatic turnaround, there was a three-way tie for second place between product range, brand recognition, and communications, training and development. This highlights that there is work to be done by non-banks to boost brokers’ confidence in the promotion of their products.

This trend is unsurprising to Peter White, managing director at the FBAA. “We have a lot to thank our pioneers in this field for, but as competition increases, so does the need to nurture those who want to bring you business,” he says. “Plus, new brokers who do or will not know what you are offering are constantly entering the marketplace.”

Brokers’ heightened focus on non-banks’ product range emphasises that they believe more lending options are needed for clients who can’t meet the criteria for prime lending. This year, there has also been a rise in the desire for product diversification opportunities, which now ranks sixth on the priority list.

Perhaps that’s what prompted brokers this year to weigh in on the lending products they deemed the best. The winners are below, with some positive broker feedback:

Another significant takeaway was the increased importance of non-bank brand recognition, highlighting the value brokers place on the reputation and visibility of the lenders they choose to do business with.

A reversal in commission structure also surfaced, falling to ninth place this year from the second-place concern in 2022. Interest rates also saw a decrease in importance, moving to eighth place from fifth in 2022. This clearly signals that they are becoming less of a primary concern for brokers.

“Major banks are about rates, and non-banks are solutions-based; these are two different beasts,” a respondent commented. Still, many brokers noted that non-banks could further boost their competitiveness through “lower rates and fees”.

Non-banks’ BDM support dropped three points to seventh place, and brokers downgraded the importance of credit policy to last place from ninth in 2022.

Online platforms and services held steady in fifth place, with brokers ranking its importance slightly higher than last year.

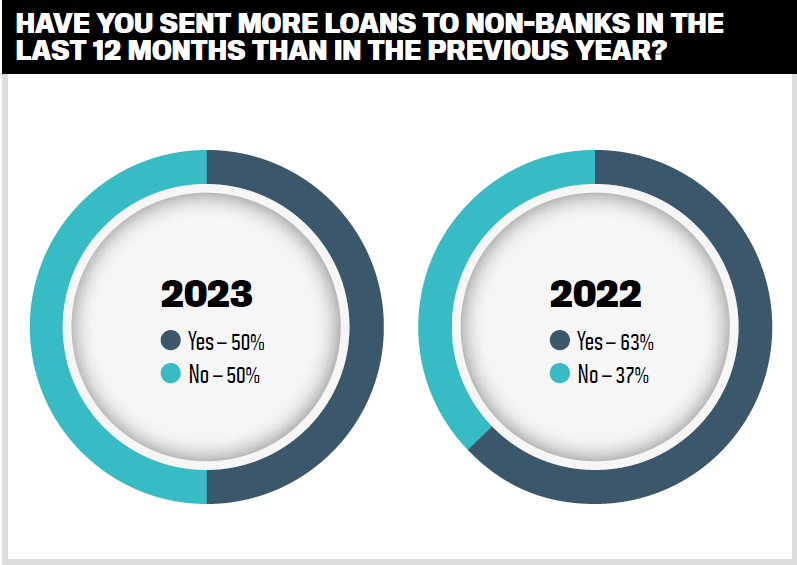

While the proportion of brokers’ loans put through non-banks continues to decrease, their appreciation of personalised service and a supportive lending experience is on the rise

MPA’s survey showed a marked decline over the past three years in the proportion of brokers who are increasing the number of loans put through non-banks: from 69% in 2021 to 63% in 2022 and just 50% in 2023.

The percentage of those putting the lowest proportion of loans (20% or less) through a non-bank was 60% versus 44% in 2022.

At the high end, just 8% of brokers put more than 60% of their loans through non-banks this year, down significantly from 13% last year and 12% in 2021.

In recent times, non-banks’ share has been declining, notes Specialist Finance Group (SFG) general manager Blake Buchanan.

“This is for various reasons, including consumer comfort with the majors during troubling times; service propositions and more,” he adds. “Non-banks usually follow technology and process trends that the banks tend to set the standards for, but this often puts them in second position and at considerable risk of further losing market share, which will lead to more mergers and acquisitions with less competition.”

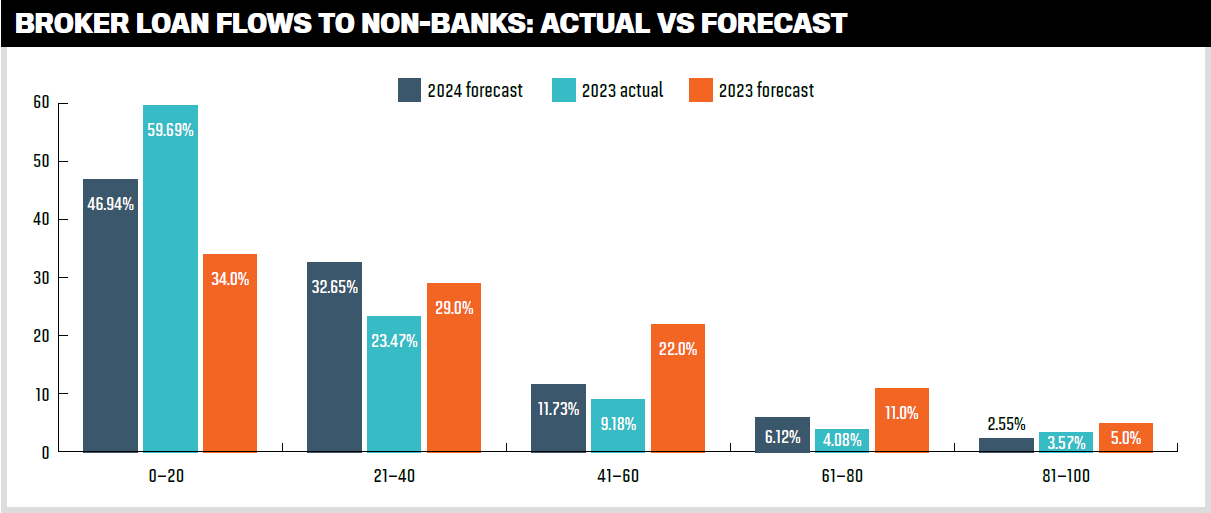

The expected proportion of loans forecast to go through non-banks in 2024 is relatively consistent with last year’s estimates, suggesting that market conditions and the competitive mortgage landscape may influence brokers’ predictions.

FBAA managing director Peter White points out that, where appropriate, aggregators need to ensure a fair and balanced approach so that all non-banks are heard and utilised.

“There is a deep history here, which is largely what brought competition into our lending sphere, but the non-banks need to step up as well and make sure the broker community’s needs beyond freebies, feed and watering are also being met,” he adds.

Non-banks remain strong for individuals with fluctuating incomes, the self-employed and investors looking for yield, and they have maintained lending standards and effectively managed risk while serving diverse clients.

In addition, loss rates for non-bank mortgages have been low in recent years, according to a March 2023 Reserve Bank of Australia bulletin.

There was no shortage of broker commentary on whether non-banks have provided enough competition for mainstream lenders in the past year:

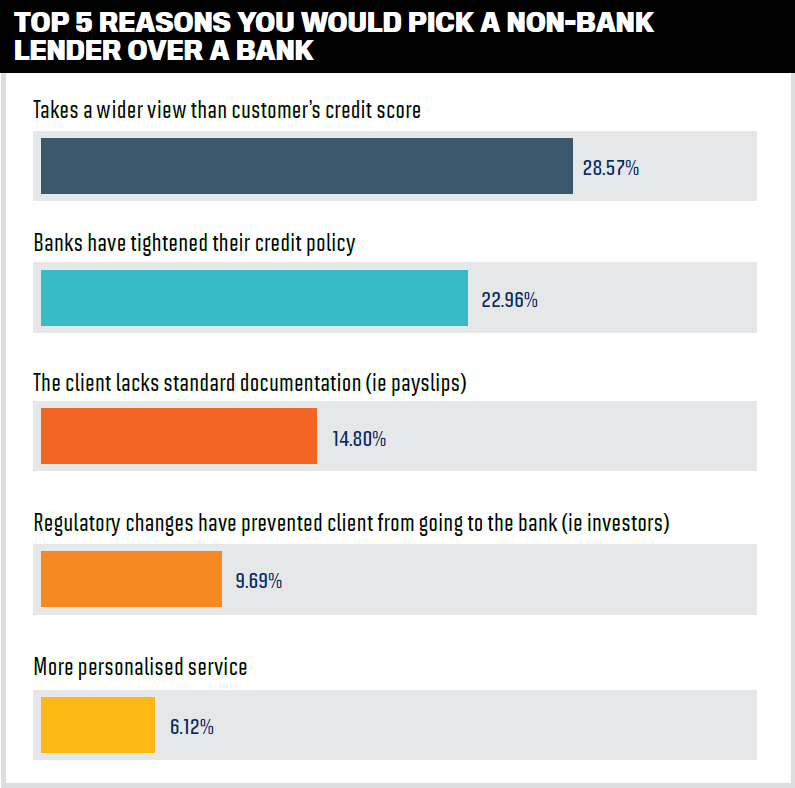

The second, third and fourth most popular reasons brokers would use a non-bank remain the same this year as last:

Although easing off slightly in importance, a lack of standard documentation remains a primary factor driving clients to non-bank lenders, particularly borrowers with diverse financial backgrounds.

One broker commented that some non-banks’ near prime products “allow lending to clients with credit impairment”.

More personal service has replaced competitive rates at the bottom of the top five. This factor appears to be tied into the top reason for brokers choosing to work with a non-bank lender, which is that a wider view of the client’s credit score is considered. Brokers appear to find value in a supportive lending experience that is nuanced and solutions based.

A high proportion of borrowers continue to see non-banks favourably, though this figure is declining, and a lack of brand awareness remains a concern

Brokers’ ratings of the benefits of using non-banks in 2023 showcase the increasing competitiveness of the specialist lending landscape. Although there is a clear overall winner, the small differences between the gold, silver and bronze winners suggest the top performers are competing earnestly.

The top three non-banks overall won six golds, five silvers and four bronzes across all categories except for product range. That distinction went to the eighth-place winner overall, Better Choice Home Loans. Pepper Money won gold for the sixth year for its BDM support, Liberty also took gold in four categories, including turnaround times and interest rates, and Bluestone garnered the same for communications, training and development.

Non-banks in the middle of the rankings with gold wins included Prospa for commission structure and product diversification opportunities, and Better Mortgage Management for brand recognition.

BDM support

Pepper Money

Liberty

La Trobe Financial

Commission structure

Prospa

Liberty

ORDE Financial

Credit policy

Liberty

Pepper Money

Firstmac

This year, the golds determined the champion, and Liberty was crowned first place overall with a score of 3.90 out of 5. This result, and other top lenders’ final tallies, topped last year’s by a significant margin, indicating industrywide improvements that brokers lauded.

Liberty was also the lender that brokers most wanted to see added to their aggregator panel this year. Mortgage Ezy made a comeback, securing second choice, and Better Mortgage Management claimed third.

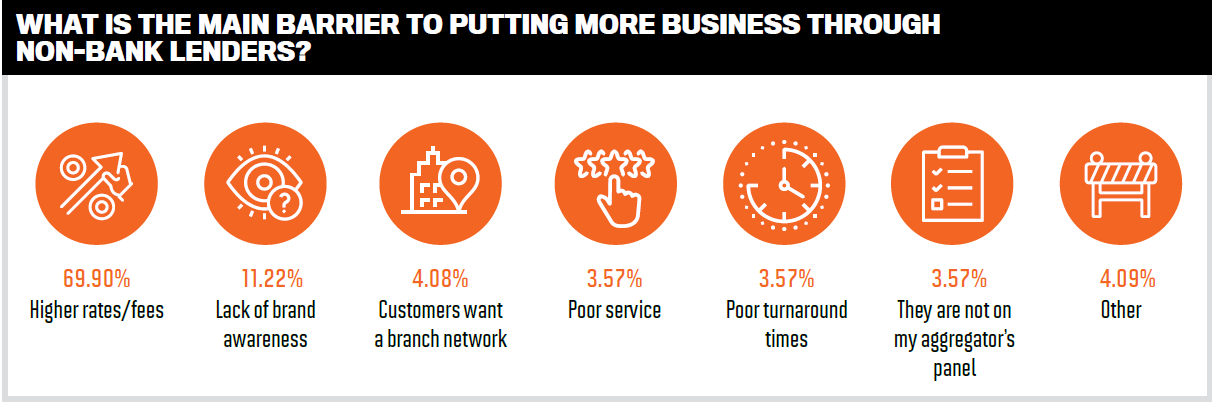

While interest rates took a dive in terms of importance to brokers when dealing with non-banks, high rates and fees are consistently cited by a majority of brokers as the number one barrier to putting more business through non-banks. This persistent trend underscores the complex and evolving nature of the lending industry and just how acutely aware brokers are of the impact interest rates have on loan origination.

It also suggests that a high interest rate environment will limit non-banks’ market share, but they have been adapting to compete effectively by offering bespoke loan products, competitive rates and flexible lending policies.

“Challenger lenders should be groundbreaking in the fulfilment space and investing more and sooner into open banking, payroll accesses and direct digital connectivity to broker CRMs for credit decisioning responses in real time,” says Blake Buchanan at broker aggregator SFG.

Still, 70% of brokers expressed concerns:

But not all share that view, commenting that certain lenders’ products offer:

AFG’s Chris Slater emphasises that major banks continue to exert significant influence over the sector and have increased their market power and concentration.

“The irony is that the dominance of major lenders has been aided in part by regulatory moves to strengthen the nation’s financial system, and the flow-on consequences have meant a material advantage for the big players that helps reinforce the lower capital and funding cost structure they conventionally enjoy through their size and scale,” he says.

“The situation is compounded by the current environment of high inflation and volatile markets, which has meant that the RMBS market, which smaller lenders often rely on as a source of competitive funding, has not been an option for many this year. This lack of competition and favoured status of the major banks is the reason that AFG has been lobbying for a supplement to the private RMBS market with a publicly supported RMBS scheme.”

The second barrier to using non-banks was a lack of brand awareness, but it appears they have steadily upped their visibility in recent years, judging by the number of respondents who noted it as a barrier: 11% in 2023, compared to 20% in 2022 and 27% in 2021.

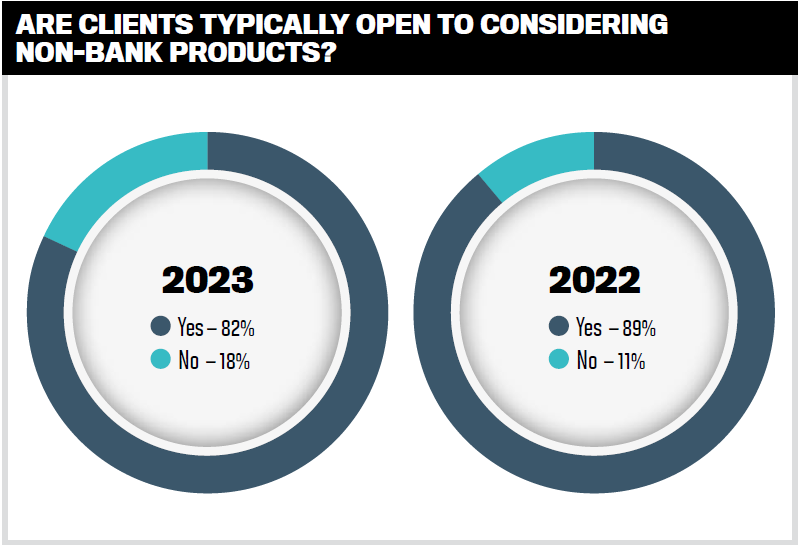

The proportion of brokers who said their clients were typically open to considering non-bank products continued to decline over the past three years but remains high at 82%, compared to 90% in 2021.

Comments highlighted clients’ confidence in non-banks:

Better Mortgage Management won the gold for brand recognition, a testament to its efforts to build a strong reputation that brokers perceive to be at the leading edge.

The survey’s overall results show that brokers are prioritising brand recognition to help boost the credibility of non-banks with clients. A small group of respondents identified lack of brand awareness as a barrier to putting more business through non-banks.

One broker observed that it is “huge in the current market”.

Interest Rates

Liberty

Better Mortgage Management

Bluestone

Brand Recognition

Better Mortgage Management

Better Choice Home Loans

Liberty

Product range

Better Choice Home Loans

Firstmac

Mortgage Ezy

Product diversification opportunities

Prospa

Liberty

Bluestone

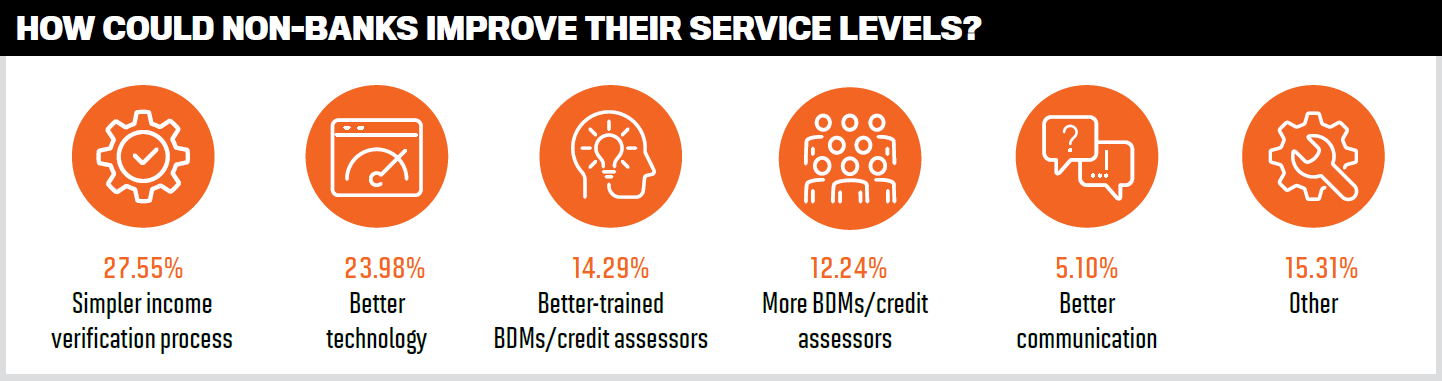

A majority of brokers reported improved turnaround times, but their wish list has changed this year to prioritise a simpler income verification process to boost customer experience

A significantly higher proportion of brokers this year – 83% compared to 73% in 2022 – said turnaround times had improved or remained the same. Less than a quarter felt that times had worsened, suggesting that while non-banks have made gains in this area, there is room for further improvement.

Brokers felt that staffing levels and communication were better and processes more streamlined, resulting in faster and more efficient service:

For the small group of respondents who felt times had worsened, the reasons offered included:

Liberty, which won gold in this category, was acknowledged by brokers as “quick”, with turnaround times that are “great compared to the major lenders”.

La Trobe Financial was once again the source of broker frustration for its perceived slowness. However, its strengths in other areas were recognised: brokers named La Trobe Financial as their preferred lender in the commercial and foreign non-residents categories, and it won the bronze medal for its BDM support.

It appears that brokers’ experience with turnaround times can vary widely:

Brokers suggestions for how non-banks could improve their service levels are in line with last year’s results. But a significantly increased number, or more than a quarter of respondents, want a simpler income verification process. High on brokers’ wish list are also more and better-trained BDMs and credit assessors. Brokers’ feedback included:

Better technology was cited as important by a slightly higher number of brokers this year, indicating their awareness of how critical it is to the broker and client experience and to giving non-banks a competitive edge.

Turnaround times

Liberty

ORDE Financial

RedZed

Communications, training and development

Bluestone

Liberty

Pepper Money

Online platform and services

Liberty

Thinktank

Better Choice Home Loans

There were two chances to win a bottle of liquor by answering the question, “Do you think the non-banks have provided enough competition to the banks over the last year? Why/why not?”

Liberty emerged as the overall champion of the 2023 Brokers on Non-Banks survey with a significant haul of gold and silver medals across the board

“We are thrilled our business partners have chosen Liberty as their preferred non-bank lender for the second year running,” says Liberty CEO James Boyle. “This recognition is a testament to the commitment of the entire Liberty team, from our BDMs to our underwriters and support staff.”

Boyle says surveys such as Brokers on Non-Banks help Liberty understand how it can best serve brokers and clients in any economic environment. “They help us ensure we continue to improve and create positive experiences for brokers and customers alike, even under challenging conditions,” he says.

“As well as a reliable and fast response, customers want competitive terms and the flexibility to help them move forward.

“By adopting a free-thinking approach and providing out-of-the-box credit solutions, we can help a wide range of customers with exceptional lending options. Liberty continues to lead the industry with unmatched diversification and capital strength.”

Boyle says brokers have been central to Liberty’s business since day one, and “we will continue to build strong relationships and meet the needs of our broker partners”.

First home buyers

Liberty

Property investors

Liberty

Alt-doc

Liberty

Commercial

La Trobe Financial

SMSF

Liberty

Foreign non-residents

La Trobe Financial

In this year’s survey, brokers were asked to rank non-bank lenders across 10 categories: BDM support; brand recognition; commission structure; communications, training and development; credit policy; interest rates; online platform and services; product diversification opportunities; product range; and turnaround times. Brokers could rank the non-banks with a score out of five in each category.

Only those institutions that achieved a response rate of at least 10% of brokers for each non-bank were included in the final list.

The survey also recorded broker responses on their preferred non-banks in these areas: specialist lending; first home buyers; property investors; commercial; alt doc; SMSF; and foreign non-residents.

MPA asked the brokers a series of questions relating to their business with non-bank lenders, as well as which non-bank they would like to see added to their aggregator’s panel, but these did not influence the overall score.

MPA: Pepper Money is a persistent gold medal winner for BDM support. What factors underpin your excellence in this category?

Barry Saoud, general manager, mortgages and commercial lending:

As customer scenarios are increasingly becoming more complex, Pepper Money continues to be at the forefront of supporting our brokers with troubleshooting complex scenarios with speed and confidence.

Pepper Money BDMs are actively workshopping applications with brokers even when it might look like a no on the surface. They are willing to invest time and effort in exploring alternative approaches, asking: “If we can’t do it this way, can we do it that way?”

It’s this can-do attitude that Pepper Money’s BDMs are celebrated for. They go above and beyond to ensure brokers are supported across all aspects. Many of our BDMs who have been in the industry for a long time are passionate about finding ways to back brokers to grow their businesses.

It is a reputation that Pepper Money takes pride in. Our BDMs are accessible and provide great support to brokers in the market. And it is support that’s backed through the same methodology that our credit assessors use when they assess the application.

Ultimately, our BDM team plays a key role in delivering our market-leading and innovative broker service proposition.

MPA: How do you intend to leverage your current success moving forward?

BS: We are humbled and delighted that brokers consistently choose Pepper Money. We cannot thank them enough for their continued support, ongoing feedback, recognition, and confidence that we deliver the right products, services and support to meet brokers’ and customers’ needs.

Keeping our finger on the pulse is crucial to continually improving our offering and providing tangible value to brokers and their customers.

Across the business, we practise ideation and open dialogue with our extensive network of aggregators, white label partners, brokers and customers to help us understand the challenges being felt in the market. Starting here allows us to ensure our lending options meet the unique needs of brokers and their customers, filling the gaps where other lenders fall short.

For over 23 years, brokers have assisted us in building Pepper Money, and we will continue to lean on our broker network for future success.

MPA: Bluestone won gold in the communications, training and development category. What are the driving forces behind your success in this area?

Tony MacRae, chief sales officer:

We’re proud to have won gold in the communications, training and development category for the second year in a row. It’s fantastic to receive industry recognition for the effort the team has put in to ensure transparent and clear communications with our broker partners. This is an absolute priority at Bluestone; it saves precious time for both brokers and us.

Our success comes down to our implementation of simple yet effective processes. Earlier this year, we launched the Scenario Hotline – brokers can call 13 BLUE and speak directly to a senior underwriter to workshop pre-submission deals, ask policy questions, or get help with application submissions. We’ve received positive feedback from brokers who have used the Scenario Hotline, which has received over 2,500 calls in the past six months.

When we introduced our SMSF loan late last year, we had one clear focus: we wanted to make it as easy as possible for all brokers to write an SMSF loan. Education is at the heart of the support we provide to brokers so that they can leverage our experience to diversify their businesses. In addition, we help at every step of the process so brokers can feel confident their customer needs are met.

MPA: How do you intend to leverage your current success moving forward?

TM: We are thrilled to receive industry recognition, which means the team can see the results of their hard work and dedication to the broker channel. At the same time, we know there is much more work to do. We have a clear focus on helping brokers serve more customers and grow their businesses; communications and training are a vital part of that.

We strive to be the ‘go-to’ lender for brokers for non-standard mortgages. We have recently expanded our credit policy to ensure we give brokers greater choice in helping customers. We have grown the team to ensure we can provide greater support to brokers on the ground. We’ve given brokers access to decision-makers in credit so they can confidently submit deals with Bluestone. We’ll continue improving our support for brokers with non-standard customers and non-standard loans; watch this space!

MPA: RedZed won bronze for turnaround times. What are your strengths in this area?

Loralle Slater, chief sales and marketing officer:

At RedZed, we are committed to supporting and empowering our self-employed customers and pride ourselves on ensuring that they remain at the heart of everything we do. To this end, we have invested significantly in technology, allowing our team to achieve consistently fast turnaround times and deliver exceptional customer experiences to our borrowers and broker partners.

We understand that brokers and our customers are busy people, so we strive to make accessing finance simple, fast and stress-free. We adopt a holistic view of business and income and take a common-sense approach to the loan application process. We measure our key touchpoints, such as assessment turnaround times and the time it takes to answer calls and emails, to keep ourselves accountable, inspire improvement and innovation, and ensure that we’re delivering the highest service levels. We also give our broker partners direct access to our BDM and client services teams and our credit assessors so that they can talk to real people at every stage of the application process. Respecting relationships is one of RedZed’s core business values, and we remain true to this value by being readily available and easy to do business with.

How do you intend to leverage your current success moving forward?

LS: This recognition will motivate our team to continue building on our support and service to our broker partners and the self-employed community. A clear and simple strategy, together with a focus on ongoing improvement and innovation, is central to achieving success, so we will continue to invest in technology to assist RedZed staff with finding the right solutions for their brokers and customers promptly while ensuring that a human is still involved in every loan decision.

We will also continue enhancing our product and service offerings to ensure we deliver outstanding customer experiences for brokers and borrowers. We are launching a free educational resource for all RedZed accredited brokers, following feedback from brokers eager to better understand the unique needs and opportunities of the self-employed market. We are confident that this interactive digital course will drive business growth for our broker partners while improving customer experiences. It is a real win-win for brokers and their self-employed customers.