Jump to winners | Jump to methodology | View PDF

Time is of the essence for non-banks. That’s what brokers demand of them, and the data shows it’s becoming even more of a priority.

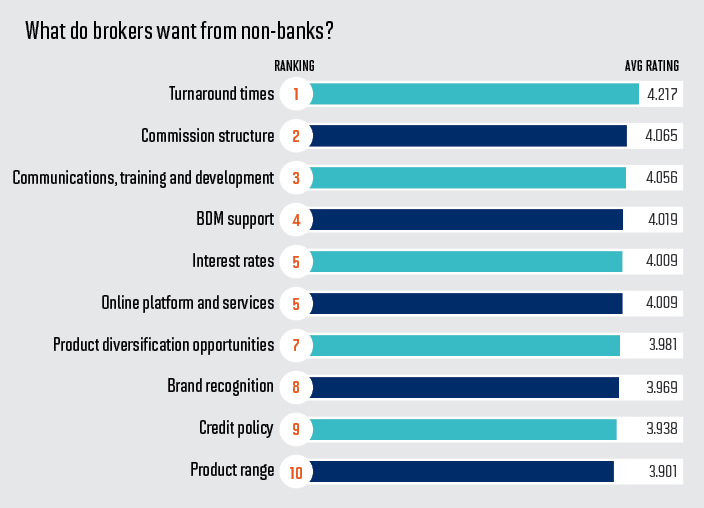

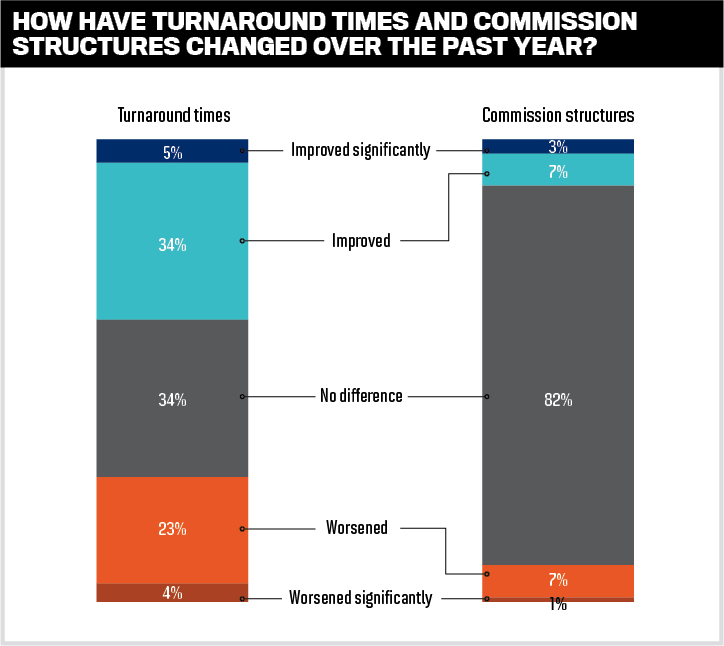

MPA’s Brokers on Non-Banks 2022 survey shows turnaround time is brokers’ number one concern. It was also their top priority last year, but by a smaller margin.

According to one respondent, non-banks are listening. “I have just noticed in the last 12 months that all lenders’ turnaround times seem to have improved,” the broker said.

The entire data set reveals that nearly three-quarters of brokers said turnaround times had improved or remained about the same. Only 27% said times had worsened – a drop from 33% in 2021.

Possibly even more eye-catching is brokers’ second most important concern: commission structure. It was the lowest concern in MPA’s 2021 survey.

Brokers evidently feel strongly that non-banks ought to address this issue better.

“One way to show their commitment to the broker channel would be to remove the ludicrous net of offset commission payments and do something to sort out clawback issues,” said one respondent.

Renewed broker worries about getting paid are in line with trends in other recent MPA surveys, such as this year’s Brokers on Aggregators report, suggesting a resurgence of more traditional priorities.

Third-ranked training and development and fourth-placed BDM support also under-score broker concerns about keeping up with the competition as the specialist lending environment continues to change rapidly in terms of macro factors, products and technology.

Non-banks generally have higher rates than mainstream lenders, but MPA’s 2022 survey shows that rates are only of middling importance to brokers this year, despite being the focus of a massive amount of media coverage since the Reserve Bank of Australia started its tightening cycle in May.

Interest rates ranked fifth equal in the survey, tying with online platforms and services in terms of importance to brokers, higher than its eighth place in 2021 but well below the number one concern of 2020.

While there were a mix of comments about whether rates were high or not, brokers often acknowledged that they were appropriate.

“Although rates are higher, this is not a major obstacle,” said one broker.

The latest national accounts data show that savings levels are still just above what they were in 2019, and that people squirreled away cash at around four times the normal pace during parts of 2020 and 2021.

Record numbers of borrowers have also used the period of ultra-loose monetary policy during the pandemic to lock in fixed rates, affording some protection from more expensive money for the time being. Financial product comparison website RateCity’s analysis showed in June that nearly two out of five home loans remain fixed, with a large group of people not coming off their fixed rates until mid to late 2023.

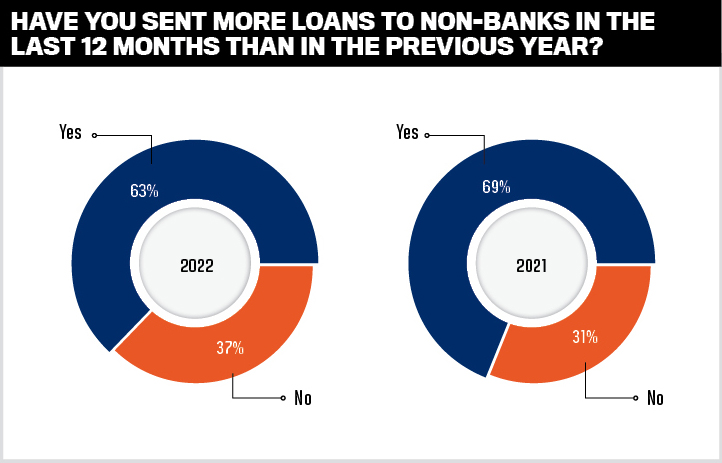

The proportion of brokers’ loans put through non-banks is down, but brokers continue to underestimate how much they need alternatives to the main lenders for customers requiring flexible solutions

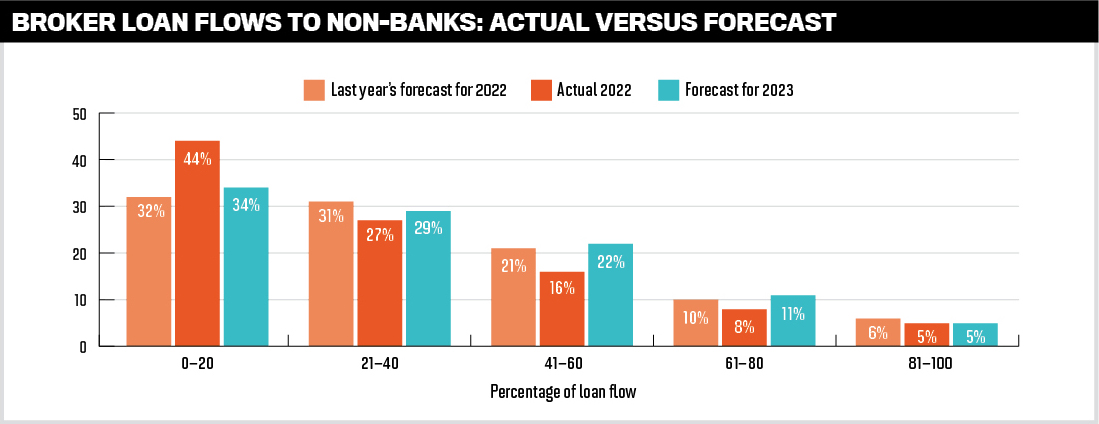

MPA’s survey showed that 63% of brokers increased the amount of loans put through non-banks in the last year, compared to a 69% increase in 2021. It also showed that, of those putting the lowest proportion (less than 20%) of loans through a non-bank, the figure was 44%, versus 45% in 2021.

This was higher use of non-banks than brokers had forecast, likely reflecting the tougher lending criteria at traditional banks and the larger number of self-employed customers seeking flexible lenders not fazed by unstable income records during COVID.

At the top end of the table, just 13% of brokers put more than 60% of their loans through non-banks this year, up from 12% last year but down from 19% in 2020.

The expected proportion of loans forecast to go through non-banks in 2023 is essentially in line with expectations seen in last year’s survey, but with interest rates still rising for now and tighter lending at banks, brokers may once again come to rely on non-banks more than they currently anticipate.

“There’s a great opportunity now and going forward over the next 24 to 48 months for non-banks to really increase on their market share,” says Peter White, FBAA managing director, who was not part of the survey.

“Even if times get a little bit tough for borrowers going forward – which it will for many – there are lots of options that can be considered. Brokers just need to be well-skilled and well-versed as to what those options are.”

The best interests duty requiring brokers to provide a suite of lending options is another factor in non-banks’ favour.

“They are on just about every aggregator panel in some shape or form or another … if it could well be in the best interest of the client, then [brokers] look at a non-bank.”

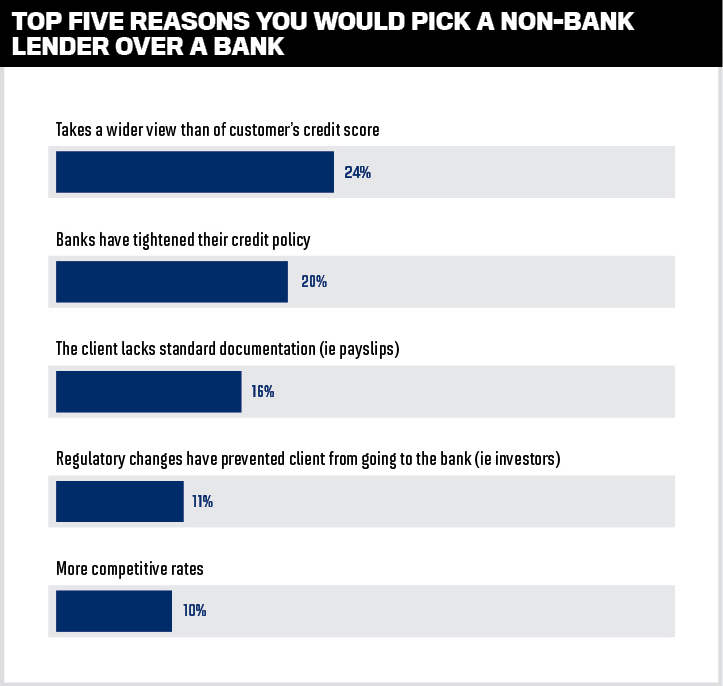

Brokers continued to turn to non-banks mainly because they take a wider view of their customers than just looking at their credit scores, with around 24% of brokers saying that was the main reason to use non-banks.

Non-banks are particularly strong in the self-employed sector due to the messy paperwork that regular banks are less able to consider when looking at an application. Life events and fluctuating incomes are also regular fodder for alternative lenders.

Contractors or labourers such as construction workers are a case in point. Such groups generally continued to be employed over the pandemic, but some had difficulty maintaining robust tax records.

One survey respondent said non-banks “provide clients who are self-employed with options that the banks will not consider. Applicants may not have lodged income tax returns, and this is a concern for banks”.

Non-banks are the only option for such people with truncated paperwork.

Another broker said specialist lending “covers clients who otherwise wouldn’t be able to proceed anywhere else”.

The second, third and fourth most popular reasons why brokers would use a non-bank are all related to this point: banks have tightened their credit policies; the client lacks standard documentation such as payslips; and regulatory changes have ruled out a normal bank as an option for the client.

Lack of standard documentation was bottom of the list of reasons in 2021 and didn’t even make the list in 2020. The fact that it has jumped to third in 2022 suggests that brokers are seeing a rise in borrowers with unusual income records due to seasonality, business disruption and the rise of the gig economy.

One respondent said the existence of products such as near prime at non-banks “has meant homeownership has been possible for clients that did not fit typical lending criteria”.

Borrowers continue to see non-banks as a good option, and a more competitive market means that brokers are becoming more discerning when it comes to rating institutions

In terms of brokers’ ratings of the benefits of using a non-bank, 2022 marks a watershed year not for any single financial organisation but for the industry as a whole. This is reflected in the extreme closeness of the results, underscoring more competition between non-banks.

The top three non-banks overall won just one gold in each of the 10 categories. Pepper Money won gold for the fifth year in a row for its BDM support, Liberty topped credit policy, and Firstmac won gold for product range.

Indeed, non-banks in the middle of the field won more golds than those on the podium, with fourth-placed RedZed winning two and seventh-placed La Trobe Financial winning three.

This year, it was silver that decided first place, with Liberty collecting six second places, showing strong consistency across a range of criteria.

But final tallies across categories were all much lower this year; the top overall score of 3.659 would only have been good enough for sixth place in the 2021 contest.

The even distribution of the field in 2022 may also have been due to the larger field of entrants who did not make the winners list this year, but still thinned broker votes at the top of the table.

BDM support

Pepper Money

Liberty

La Trobe Financial

Commission structure

La Trobe Financial

Liberty

Thinktank

Credit policy

Liberty

Firstmac

Mortgage Ezy

The organisation that brokers most wanted to see added to their aggregator panel this year was also the overall winner – Liberty. Last year’s winner in this area, Mortgage Ezy, slipped to the number three choice, while RedZed came second.

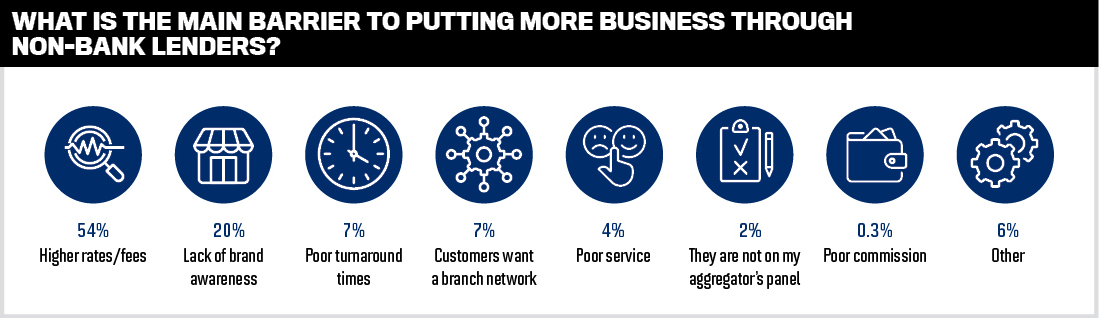

While interest rates only appear mid-table when it comes to importance to brokers dealing with non-banks, they continue to be the major barrier to doing more business with them. This suggests there is a limit to how much share non-banks can take from mainstream banks, or at least it shows a dynamic balance that can only change if more borrowers get turned away from regular lenders.

More than half of all brokers said non-banks’ higher rates and fees were stopping them from using them more.

“Rates are too high still,” said one broker. “I understand there are higher risks with self-declared income, but if the rates reduced with LVR that would be great.”

Another said, “They are expensive; they have a lot more upfront costs.”

Despite such comments, several respondents praised the rates available at non-banks, saying they were “low”, “good”, or “competitive”, often tying in praise for rates with praise for the product, such as a “higher borrowing capacity for clients”.

The second biggest barrier to using a non-bank lender was a lack of brand awareness, a repeat of the survey result in 2021 and 2020. However, non-banks may be beginning to make headway in this depart-ment, with only 20% of respondents saying brand awareness was low, compared to 27% last year.

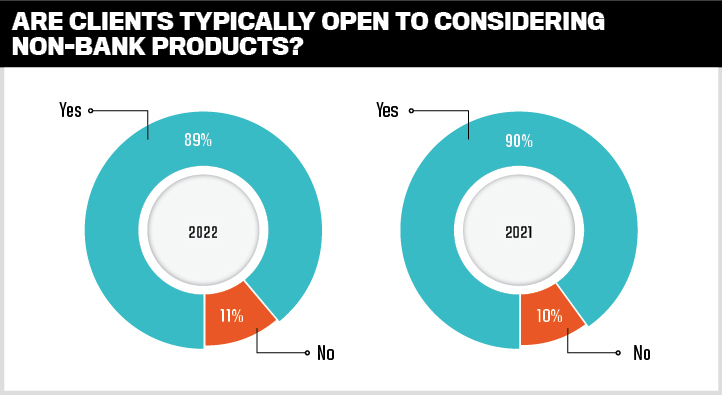

The proportion of brokers who said their clients were typically open to considering non-bank products remained high in 2022, at 89% versus 90% last year. In 2020, the figure was 70%.

Survey comments backed up the higher levels of trust in non-banks than a few years ago. “[There are an] increasing number of customers for these types of processes and policy,” said one respondent.

La Trobe Financial took home the gold medal for brand recognition for the second year in a row, suggesting its marketing is effective. But overall, many brokers still believe non-banks need to do more in this area.

“I think they could do a better job of banding together to get awareness out to the general population,” said one respondent, adding that “some people are afraid of non-banks because they don’t understand them”.

Another agreed, saying that “non-bank lenders really need to differentiate themselves from the majors if they wish to secure the bulk of brokers’ business”.

At the same time, the image of banks was not so great in the eyes of a few brokers. “Banks can have limited policy criteria and operate like robots,” said one respondent.

Another criticised mainstream banks for lifting rates too quickly in the current environment. “As soon as the RBA increased their rates the big banks went along for the ride and increased their rates yet again, making them less competitive,” a broker said.

Interest Rates

La Trobe Financial

Liberty

Firstmac

Brand Recognition

La Trobe Financial

Liberty

Better Mortgage Management

Product range

Firstmac

Mortgage Ezy

Better Choice Home Loans

Product diversification opportunities

RedZed

Bluestone

Liberty

Both positive and negative experiences abound for brokers, but on the whole, tech gains seem to be improving turnaround times more than they did a year ago

Nearly three-quarters of brokers this year said turnaround times had improved or remained about the same. Only 27% said times had worsened – a drop from 33% in 2021. This suggests the tech improvements seen in recent years are finally paying off for non-banks and brokers. Some non-banks were praised by brokers for having same-day turnarounds, but improvements seem to be across the board.

Brokers cited an increase in staffing levels and people being back in the office post-COVID as a factor, with BDMs easy to reach to move things along.

“In 2021, times were terrible due to the pandemic,” said one respondent.

Brokers also said non-banks were doing better in this area than banks: “[Times have] definitely improved with the major banks not able to deliver with the volumes … the same products are available with non-bank lenders who have capacity to take more customers on board and deliver.”

Negative comments around turnaround cited a lack of knowledge about processes, and difficulty in contacting the right people as factors hurting time to decision.

“[There are] too many gatekeepers who don’t understand the file or documents sent, returning files that are correct. Would a phone call really kill them over emails?” said one respondent.

RedZed, which won gold in this category, was described by several brokers as very efficient, while one broker called bronze winner Firstmac “a joy to deal with”.

But others such as Resimac and La Trobe Financial were panned for slower turnaround times. This slowness in turnaround likely weighed on La Trobe Financial in the overall rankings, given that it won gold in three other categories.

Other brokers cited structural or cyclical factors as reasons for better or worse turnaround times.

“There have been periods post promotional offers where turnaround times have worsened, but this is the same for any major bank,” said one.

Another respondent said times were quicker “more due to customer involvement in lending rather than good management by institutions”.

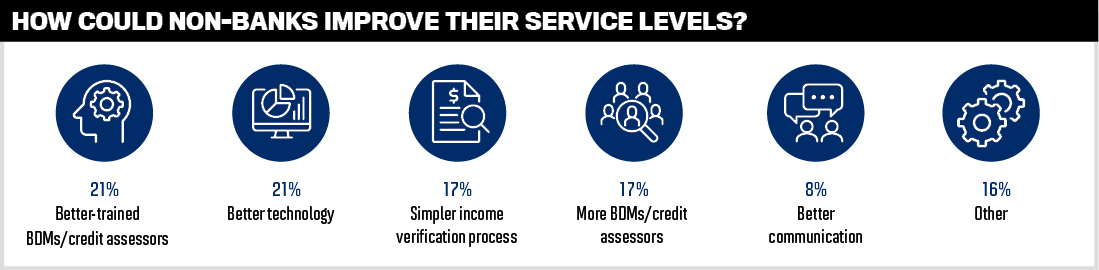

When asked how non-bank lenders could improve their service levels, brokers’ responses were different to last year, when better technology was at the top of the wish list by several percentage points. This year, better-trained BDMs and credit successors tied with better tech as ways non-banks could improve their service, suggesting that many brokers are happy with the improvements over the last 12 months.

Fintech is an area that continues to evolve rapidly, with banks and non-banks investing heavily in better systems to improve the broker experience. Providing a seamless experience for brokers is a key way that non-banks compete for custom.

Simplifying the income verification process ranked third on brokers’ wish lists for improving service, and better technology plays a key role in this.

Turnaround times

RedZed

Liberty

Firstmac

Communications, training and development

Bluestone

Pepper Money

RedZed

Online platform and services

Mortgage Ezy

Liberty

Pepper Money

There were three chances to win bottle of liquor by answering the question, ‘Do you think the non-banks have provided enough competition to the banks over the last year? Why/why not?’

With a large haul of silvers across the categories and no single institution dominating the golds this year, consistency of performance pushed Liberty into first place overall in the Brokers on Non-Banks survey

Specialist lending

Liberty

First home buyers

Firstmac

Property investors

Firstmac

Commercial

La Trobe Financial

Alt-doc

Pepper Money

SMSF

Liberty

Foreign non-residents

Mortgage Ezy

In this year’s survey, brokers were asked to rank non-bank lenders across 10 categories: BDM support; brand recognition; commission structure; communications, training and development; credit policy; interest rates; online platform and services; product diversification opportunities; product range; and turnaround times. Brokers could rank the non-banks with a score out of five in each category.

Only those institutions that achieved a response rate of at least 10% of brokers for each non-bank were included in the final list.

The survey also recorded 322 broker responses on their preferred non-banks in these areas: specialist lending; first home buyers; property investors; commercial; alt doc; SMSF; and foreign non-residents.

MPA asked the brokers a series of questions relating to their business with non-bank lenders, as well as which non-bank they would like to see added to their aggregator’s panel, but these did not influence the overall score.

MPA: What does winning the No.1 spot mean to Liberty and what are your plans for the next six to 12 months?

John Mohnacheff, group sales manager:

To receive recognition direct from the brokers themselves is a testament to the dedication of the entire Liberty team. From our BDMs to our operations teams, underwriters and support staff, every department has come together to ensure we continue providing the excellent service brokers have come to expect.

Liberty has always led the market with diversification and operated with agility, innovation and flexibility. Our ability to pivot quickly in response to market needs is what sets us apart.

We take pride in being a business that’s willing to listen and look beneath the surface, while discovering innovative ways to improve financial inclusion for more borrowers. By adopting a free-thinking approach and providing out-of-the box credit solutions we can help find the right fit for more customers.

We know brokers value high-touch, personalised support, and our BDMs work tirelessly to help our business partners achieve the best customer outcomes.

We’ve worked hard to strengthen our brand and ensure brokers and customers are aware of the genuine alternative solutions available to them. It all comes back to our mission of helping more people get financial.

We want to know how we can continue to improve. Surveys such as Brokers on Non-Banks are important in helping us learn how to best serve business partners and clients, particularly in the current environment.

In the next 12 months, Liberty will ultimately do what we have always done – listen, analyse and innovate. We will continue to deliver a range of solutions that will help a wide spectrum of customers with leading lending options.

MPA: What challenges and opportunities do you see for the next six to 12 months?

Barry Saoud, general manager, mortgages and commercial lending:

In this rising-rate environment, building relationships and confidence with customers is arguably more important than ever for brokers. Ensuring a customer’s loan application makes it all the way to settlement is crucial for our brokers’ success, so supporting conversion is a fundamental focus for us across the next six to 12 months. We see this as an opportunity to continue investing in technology and broker education. For our brokers, this includes better understanding the parameters of their lender panel, whether it be mainstream banks or non-bank lenders, and the probability of customers getting a loan with specific lenders.

MPA: Pepper Money won gold in the BDM support category. What are your strengths in this area?

BS: While building strong relationships with our distribution partners has always been part of our mission, it was hugely important in a lending year disrupted by COVID-19, a war in Ukraine, rising rates, and a slowing property market.

As customer scenarios are becoming more complex, Pepper Money continues to be at the forefront supporting brokers in trouble-shooting complex scenarios with speed and confidence. Our BDMs are relentlessly focused on ensuring brokers across the country are fully supported now more than ever. In the last 12 months, we’ve introduced additional layers of support, with two new regional managers and five new desktop BDMs to ensure our team continue to deliver world-class service. We’re also upskilling our BDM teams across both the residential and comercial credit spectrum, as one expert point of contact makes for better experiences.

What challenges and opportunities do you see for the next six to 12 months?

Kim Cannon, managing director: The main challenge for everyone is client retention. Official interest rates have been steadily rising, causing many people to review their lending arrangements. It’s a super-competitive, price-sensitive refi market. In this environment, brokers can really help their customers by encouraging them to focus on repaying their home loans instead of being distracted by short-term incentives that may extend their loan term and set them back. The main opportunity for us is to benefit from the strength of refinancing enquiry by maintaining our culture of personal service that is focused on helping brokers get their deals across the line.

Firstmac won gold for its product range. What are your strengths in this area?

KC: Our long-standing strength is in bringing simple, affordable, prime home loans to market. However, brokers are looking more now to diversity their standard offering, and we’ve been able to provide for this with some innovative new product streams. We’ve brought out the best SMSF product in the market and some of the best car loan products. We also have pioneered green car and home loans that reward customers with cheaper interest rates for energy-efficient assets which help them to protect the environment.

What challenges and opportunities do you see for the next six to 12 months?

Chris Calvert, executive general manager for distribution: The immediate challenge non-bank lenders such as RedZed face in this increasing interest rate environment is cost of funding. All lenders are trying to find the right balance between keeping their rates competitive whilst managing their funding position. No matter the economic cycle, there is always opportunity. We believe the lenders that have invested in both their technology and systems with a focus on improving simplicity and speed for their customers are those that can remain competitively priced without sacrificing the service they provide.

RedZed won gold in the product turnaround times and product diversification opportunities categories. What made you stand out in these areas?

CC: The feedback that we constantly receive from our brokers is that turnaround times, consistency of decision-making and offering products that are solutions focused are what is most critical to them in servicing this market. This is what we focus on. We are obsessed with delivering the best customer experience that we can, and measuring key touchpoints such as our turnaround times and the time it takes to answer calls and emails is central to this. Our brokers also want products that reflect the needs of the self-employed, and that’s what we try to do. We are continually enhancing our product features to enable more self-employed borrowers to find a lending solution.