National values rise for fourth straight month

Despite lingering global uncertainty and ongoing interest rate speculation, New Zealand property values edged higher in April—marking the fourth consecutive monthly gain and reinforcing signs of a gradual market recovery.

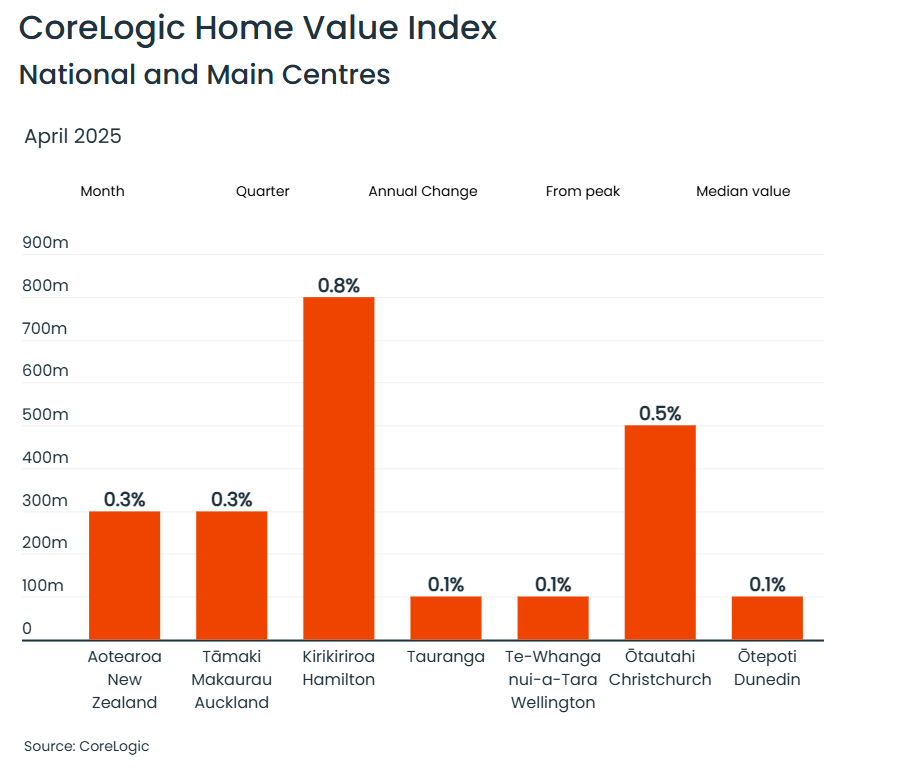

According to the latest Cotality Hedonic Home Value Index, national values rose +0.3%, lifting the average home price to $819,096—the highest level since June 2023.

Despite this momentum, prices remain about -16% below their January 2022 peak of $974,045.

Major centres see broad-based gains

April saw value increases across most major urban centres:

- Hamilton: +0.8%

- Christchurch: +0.5%

- Auckland: +0.3%

- Dunedin, Wellington, and Tauranga: each up +0.1%

At a property-type level, the upturn is also becoming more widespread. Townhouses (flats) have risen by +0.9%, standalone houses by +1%, and lifestyle properties by +0.2% since January.

Upturn is real, but no boom ahead

Cotality NZ chief property economist Kelvin Davidson (pictured) said the trend is unfolding much as expected, though the market remains finely balanced.

“Clearly, lower mortgage rates have been a strong support for property values in recent months, giving more buyers the confidence and ability to enter the market,” Davidson said. “Perhaps in a slightly perverse way, the recent global uncertainty about tariffs and trade protectionism could also see interest rates fall further.”

However, Davidson noted several factors may limit any rapid surge in prices.

“That said, a fresh boom in property values seems unlikely,” he said. “For a start, the stock of listings on the market remains high, giving buyers plenty of power when it comes to price negotiations.”

Daviddson added that borrowing conditions are evolving too, with new regulatory considerations affecting buyer behaviour.

“Meanwhile, as interest rates for internal serviceability tests at the banks fall to less than 7%, the caps on debt-to-income ratios (DTIs) for mortgage lending are reportedly becoming a bigger consideration for more borrowers.”

Davidson also urged caution, pointing to past volatility and the broader economic outlook.

“It’s also worth keeping in mind we had a ‘mini upturn’ in values over the second half of 2023 and first few months of 2024 which then partially reversed out again,” he said. “This latest emerging phase of growth seems to have stronger fundamentals than the previous one, but even so, a subdued economic backdrop still looms as a restraint.”

Auckland sub-markets show uneven growth

Auckland saw broad, though mild, improvement across sub-regions in April. Suburbs such as North Shore, Rodney, Waitakere, Auckland City, and Franklin recorded gains of +0.3% to +0.4%.

Manukau remained flat, while Papakura dipped by -0.1%. Over a three-month period, North Shore, Franklin, Manukau, and Auckland City have all risen by at least +1%, although Rodney is down -0.6%.

“In any part of the cycle there are different areas that either underperform or outperform, and with buyers still holding the bulk of negotiating power, it’s not all one-way traffic for property values in Auckland,” Davidson said.

“However, the impact of lower mortgage rates does seem to be spreading across the super-city.”

Wellington’s recovery led by Kapiti Coast

In Wellington, Kapiti Coast led with a +1.4% increase in April. Lower Hutt rose by +0.4%, while Upper Hutt edged up +0.1%. Porirua and Wellington City remained flat.

Kapiti also outperformed over the past quarter, rising +1.7% since January, with Lower Hutt up +1.1% in the same period.

“The large falls in property values around the Wellington area in recent years seem to have come to an end, and significantly improved affordability may be piquing the interest of more buyers,” Davidson said.

“But as with many other parts of the country, available listings remain high, so buyers aren’t in a rush to compete or bid up prices sharply.”

Mixed results across regional markets

Regional New Zealand showed more varied results in April:

- Whangarei, Rotorua, and Napier: each up by +0.5%

- Whanganui and Invercargill: both rose +0.4%

- Nelson: down -0.5%

- Hastings: down -0.6%

- Queenstown: down -1.0%

“In the current environment where listings are higher than normal in many parts of the country and some sectors of the economy are yet to rebound, a bit of variability across the provinces is to be expected,” Davidson said.

“But lower interest rates are a significant support, so the outlook for a modest recovery in values this year is likely to be replicated across regional markets too.”

Outlook: 5% growth forecast for 2025

Looking ahead, Davidson expects a 5% national increase in property values in 2025, broadly in line with recent trends.

“That rate of increase looks relatively modest by past standards and given that we’re still about 16% below the record highs from early 2022. Some people may well be disappointed with such an outlook.”

“But it’s always worth noting there are two sides to the housing market coin, and any aspiring first home buyers, or investors, who are progressing towards saving a deposit will no doubt be pleased with a flatter patch for values.”

“Of course, there’s now quite a range of lending hurdles which also need to be negotiated, and it’s going to be fascinating to see how the impact of DTIs plays out over the next year or two.”

RBNZ’s 5% outlook aligns with a recent Reuters poll, but is more upbeat than ANZ’s revised forecast of 4.5%—down from an earlier 6%—as the country’s largest lender cites rising listings and softer momentum. BNZ remains the most bullish, tipping a 7% gain in values this year.

Read the Cotality announcement here.