Confidence declines amid global volatility, but second-half sentiment improves

New Zealand business confidence declined in May as firms responded to international uncertainty, particularly around US tariffs.

However, fresh survey data from ANZ revealed that sentiment improved in the second half of the month, hinting at stabilisation beneath the surface.

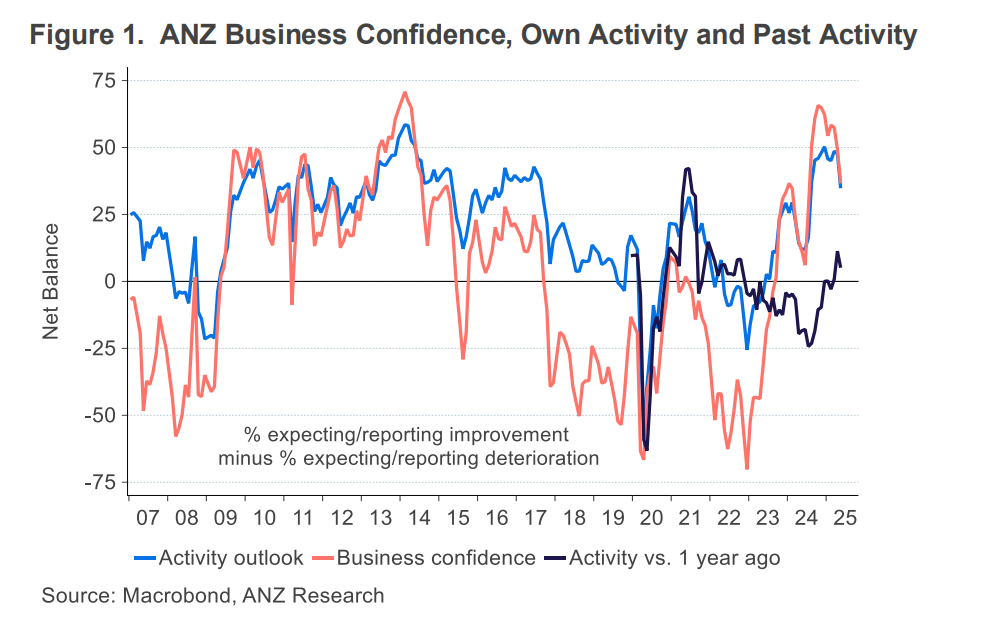

“Business confidence fell 12 points to +37 in May, and expected own activity fell 13 points to +35. However, late-month responses were higher than the early-month ones,” said Sharon Zollner (pictured left), chief economist at ANZ NZ, in the May Business Outlook.

Michael Gordon (pictured right), senior economist at Westpac NZ, observed similar dynamics.

“Business confidence has softened in the wake of the US tariffs – though next month may tell a different story again,” Gordon said.

Confidence metrics remain above average but well off late-2024 highs

Confidence, while still above long-term averages, continued to fall from its late-2024 highs. The survey’s reported own activity, a key GDP proxy, fell to +5, while past employment dipped to -10. Business confidence dropped to 36.6 in May from 49.3 in April.

“The biggest fall in confidence in May was seen in the construction sector, with retailing also noticeably softer on some aspects,” Gordon said.

Survey volatility masks recovery signs

Despite headline weakness, ANZ noted underlying improvement as global turmoil began to settle. While volatility is still expected, confidence, profitability, and investment intentions have all lifted off their April lows.

“There’s still plenty of scope for more volatility, but for now, some of the initial hit to confidence, own activity expectations, profitability and investment intentions has dissipated, with these indicators well off their late-April lows,” Zollner said.

Cost pressures and pricing ease despite inflation tick

Inflation expectations rose marginally to 2.71%, but pricing intentions and cost indicators both eased. This indicates firms are still struggling to pass on costs.

“Pricing and cost indicators eased. One-year-ahead inflation expectations lifted marginally from 2.65% to 2.71%; we’d call that pretty steady,” Zollner said.

Gordon noted the impact of recent CPI data, which showed inflation rising more than expected in Q1, but said pricing pressure from firms was retreating.

“Firms’ own pricing intentions eased back for a second month, and there was a slight drop in expected cost pressures.”

Wage expectations remain benign, RBNZ expected to stay supportive

Expected and reported wage growth stayed subdued, supporting ANZ’s view that inflation pressures remain contained.

“Expected and reported wage increases were also benign… Overall, there are not any obvious grounds in this survey for the RBNZ to be overly concerned about the recent tick higher in some surveys of inflation expectations,” Zollner said.

Following the Reserve Bank’s 25bp cut to the official cash rate in May, ANZ said current conditions support ongoing stimulus.

“The economy is recovering, but that it’s still hard going here and now, and that it’s still difficult to pass cost increases through to prices. That’s an environment in which the RBNZ can afford to support growth,” Zollner said.

“Failing that, we expect the RBNZ will ultimately take the official cash rate to a low of 2.5% to shore up the economic recovery as it faces into global headwinds.”

Read the latest ANZ Business Outlook and the Westpac NZ insights.