Economist explains why

The price premium over existing homes might decrease in the coming years despite traditionally being around 6% higher, according to the latest insights from CoreLogic.

“We estimate that new builds are currently running about 6% more expensive than existing properties, which is in line with past norms,” said Kelvin Davidson (pictured above), CoreLogic’s chief property economist.

This premium is largely due to new-builds typically offering higher quality, such as better insulation. However, Davidson predicted that the gap may narrow a bit in the next few years, attributing potential changes to less favourable tax rules for new properties.

See LinkedIn post here.

The evolution of new-build premiums

Historically, new-build premiums have fluctuated, with periods during the early 2000s and mid-2016 to 2020 seeing significant spikes. Yet, Davidson pointed out a time during the GFC when new builds were cheaper than existing homes, hinting at possible future discounting due to slower building work and construction cost stabilisation.

Currently, the new-build premium stands at an average of 6%, translating to a notable dollar difference of $40,000 to $50,000 recently. In February, this meant existing homes sold for $768,050 compared to new builds at $811,000, CoreLogic reported.

Factors impacting new-build premium

Davidson said the enduring presence of a premium on new-builds over time comes as no surprise.

“After all, they require less maintenance and will tend to be higher quality,” he said. “On top of that, although the growth has slowed down now, there’s previously been sharp increases in residential construction costs over the past three to four years, conceivably meaning that new builds have simply had to be priced higher to reflect that reality.”

Davidson added that recently, new builds benefited from favourable lending and tax regulations, including exemptions from LVRs, allowing lower deposits and 100% mortgage interest deductions for landlords. Additionally, a shorter Brightline Test for new builds (five years) compared to existing properties (ten years) likely contributed to their price premium.

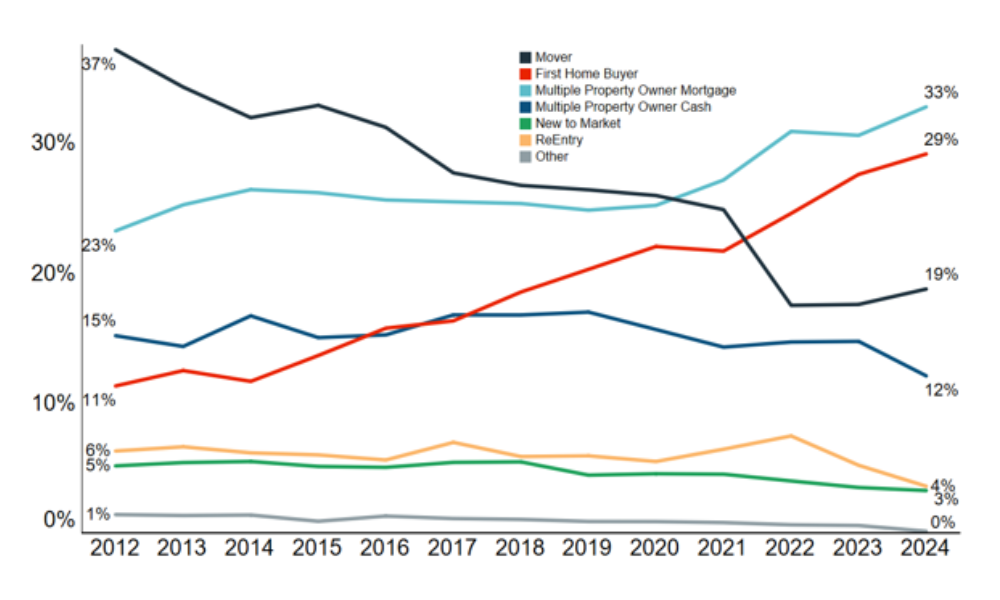

Considering these factors, it’s expected that CoreLogic Buyer Classification data indicated an increasing trend of new-build purchases by mortgaged investors and first home buyers, as illustrated in the chart below.

Future outlook

Looking ahead, Davidson suggested the premium for new builds could erode, similar to the post-GFC period. He cited current market conditions, like the slowing of building work and the challenges developers face in securing pre-sales, which may lead to near-term discounting.

Additionally, upcoming changes in mortgage interest deductibility rules could level the playing field between new and existing properties for investment buyers.

“Ultimately, whether new builds cost a little or a lot more than existing properties, the bigger point is that we simply need more of them in future,” he said, emphasising the need to accommodate population growth and address housing affordability.

Read the CoreLogic analysis here.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.