Repayment costs push up market listings

Gareth Kiernan (pictured above), chief forecaster and director at Infometrics, has noted a surge in properties listed for sale, attributing this trend to growing mortgage stress among homeowners.

February saw the highest number of homes available for purchase on realestate.co.nz since 2015, a phenomenon only surpassed by listings following the initial COVID-19 lockdown.

A market constrained by affordability

Despite a brief uptick in sales in early 2023, demand has waned since October, largely due to affordability issues.

“With less intense demand for buying property, the increase in people wanting to sell their property clearly isn’t a response to improving demand conditions," Kiernan wrote in an analysis first published in Stuff.

Instead, Centrix data revealed rising mortgage arrears, with 1.47% of mortgages affected, up from 1% in 2022, indicating homeowners may be selling to avoid foreclosure, he said.

Although mortgage stress is at a pre-COVID high, it matches the arrears rates seen from 2017 to 2019.

Pandemic purchases prove costly

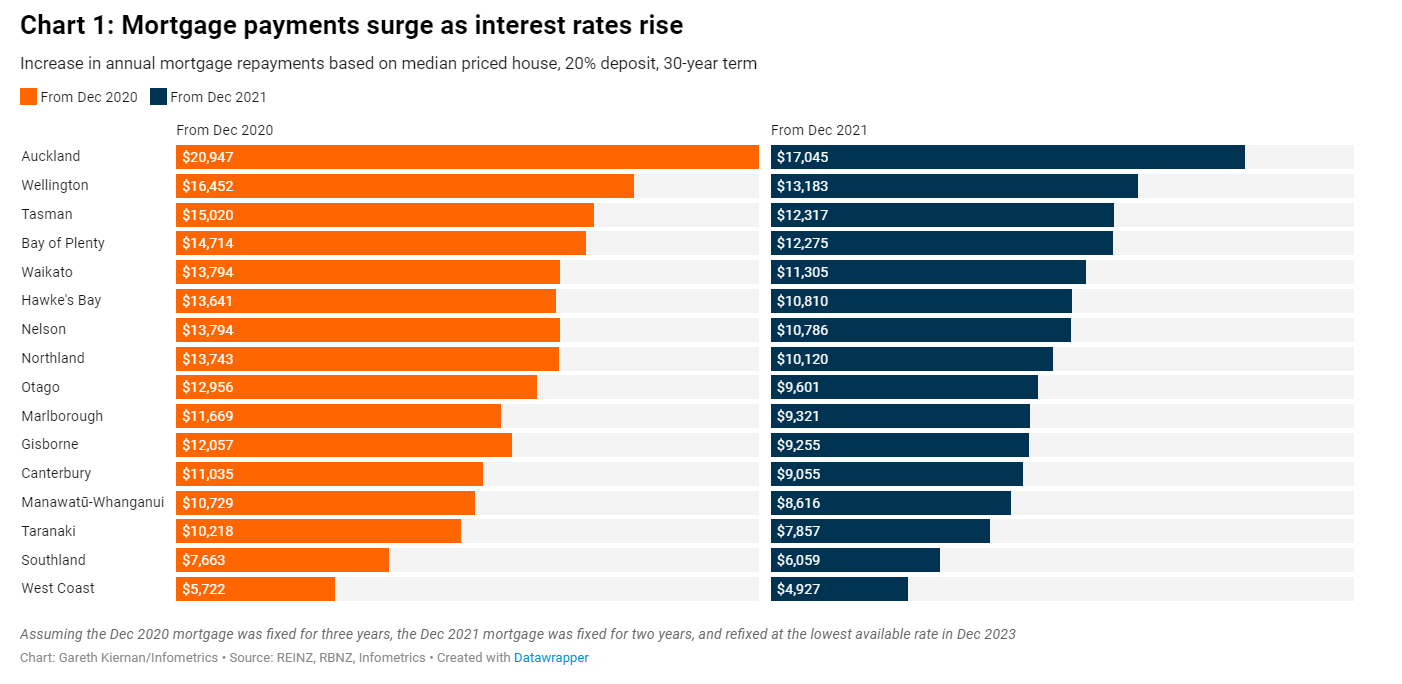

Owners who bought a house in December 2020 with a 2.8% fixed-rate mortgage and refinanced at the end of last year saw their yearly payments jump by $5,700 to nearly $21,000, depending on the location. Similarly, those who purchased at the end of 2021 with a 4.3% rate faced increases from $4,900 to over $17,000 annually.

"For people who bought during the pandemic housing boom, the source of that mortgage stress is clear," Kiernan said.

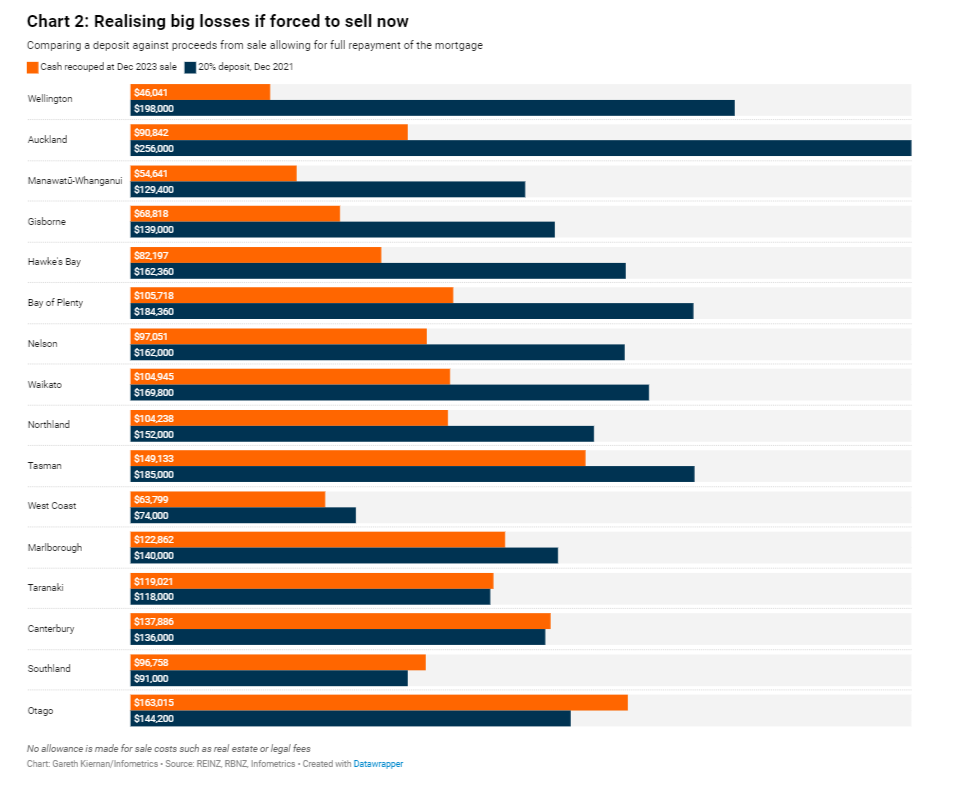

Homebuyers face substantial increases in annual repayments upon refinancing, with those who purchased at the end of 2021 potentially incurring the most significant financial strain. This cohort risks substantial capital losses if forced to sell, with only buyers in certain regions like Otago, Southland, Canterbury, and Taranaki able to recoup their initial deposits.

Investor decisions under the microscope

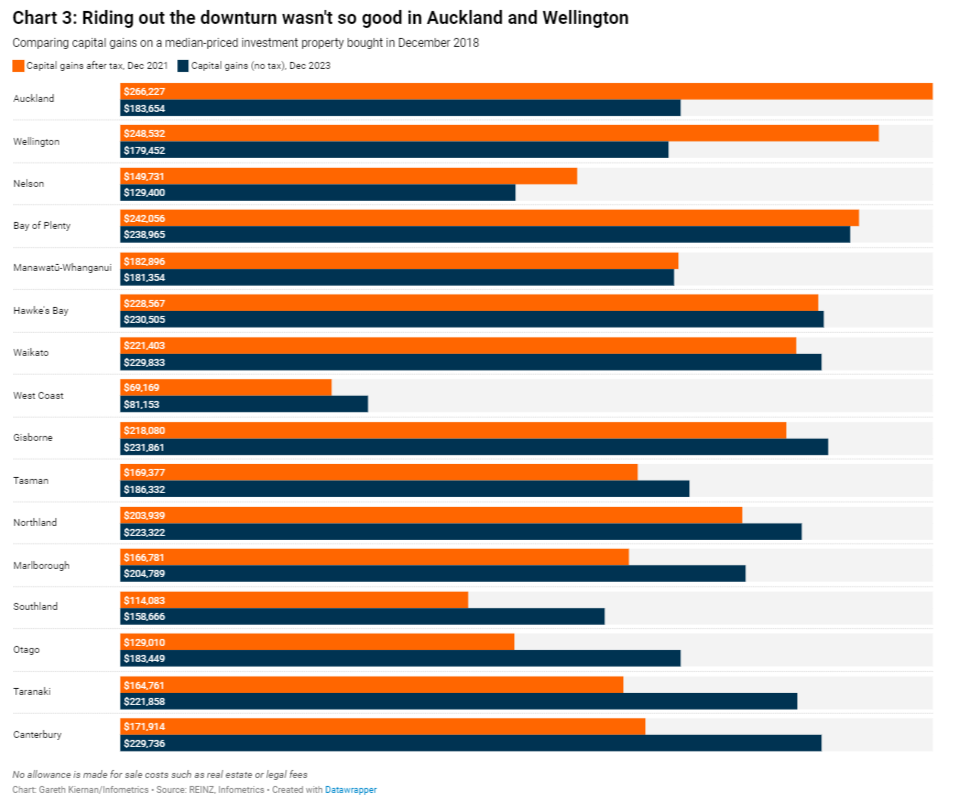

Kiernan also pointed to the impact of the brightline test extension on investor behavior, suggesting that the inability to sell without incurring a capital gains tax during the 2021 boom may have inadvertently stabilised the market.

However, with properties bought post-April 2018 now eligible for sale tax-free, and mortgage rates at their highest since 2008, investors might be pressured to sell, increasing property supply.

Outlook remains tense

With no immediate relief in sight from the Reserve Bank, and the brightline threshold ushering more properties onto the market, Kiernan predicted that the supply of homes for sale will continue to grow through 2024.

“Homeowners will continue to roll off lower fixed mortgage rates as well, leading to an increasing amount of mortgage stress,” he said. “But buyers will remain limited – affordability constraints mean that a new buyer would need to spend almost 50% of their average household income on first-year mortgage repayments, something many might be unable to afford.”

And even with a boost in buyers due to high net migration, the housing market conditions are unlikely to favour a significant increase in house prices in 2024, Kiernan said.

Read the Infometrics analysis in full here.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.