Figures confirm end of the recent housing market downturn

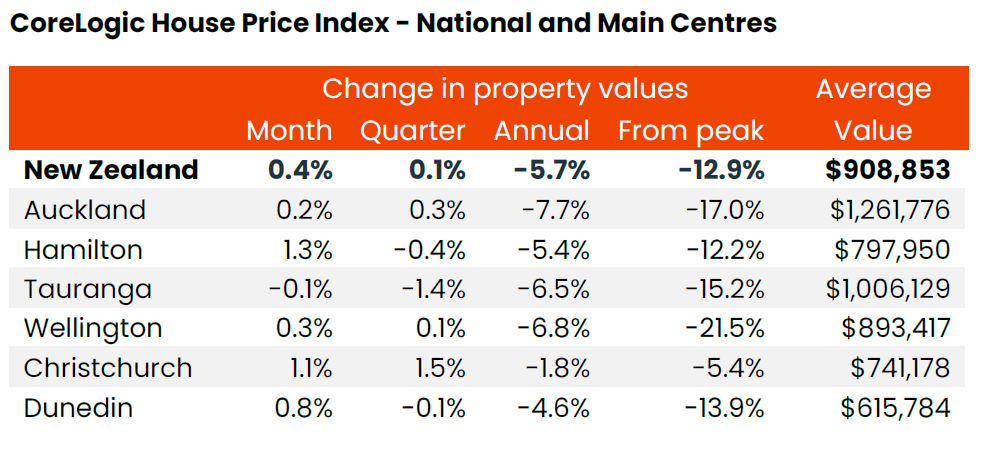

After staying flat in September, CoreLogic's national House Price Index (HPI) bounced back with a 0.4% rise in October, marking the first increase in property values since March 2022, with a 0.1% gain over the past three months.

CoreLogic said the figures confirmed that the recent housing market downturn has ended, with a total peak-to-trough decline of 13.2%, equivalent to roughly -$138,000. Nevertheless, with average values reaching nearly $909,000 in October, they remained almost 25% higher than the levels seen before the onset of COVID-19 in March 2020.

Kelvin Davidson, CoreLogic NZ’s chief property economist, noted that across the main urban centers, indicators of the emerging upturn were pretty widespread in October.

Property values in Hamilton and Christchurch increased by more than 1%, Dunedin by 0.8%, and Wellington and Auckland also saw rises during the month. Tauranga remained relatively stable, however, with a slight decrease of 0.1%.

“The key fundamentals for house prices have been looking stronger for a reasonable period of time now,” Davidson said. “October’s data has brought that first increase at the national level, but it’s early days and there's still a lot of diversity in market conditions across the country.

“Although a new government hasn’t been formalised just yet, the shift in voting to the centre-right seems to have bolstered housing market confidence, despite mortgage rates edging higher again recently,” he said. “We’ve also seen net migration rise to a new record high, which is boosting property demand.”

Another significant contributor to the housing market’s recovery, Davidson said, has been the consistent strength of the labour market.

“While this week’s official data for quarter three may show a rise in the unemployment rate, it will be due almost entirely to a larger labour force, not job cuts,” he said. “The resilience of employment has meant the vast majority of households have successfully managed to rejig their finances as they reprice from older, lower fixed rates, onto today's higher levels.”

The easing of CCCFA rules since May and the slight relaxation of LVR settings from June have also played a part, along with the persistent low supply of new listings, the economist said.

“As a result, there’s been a re-emergence of some degree of competitive price pressures, as buyers attempt to secure a property in a market where there’s a bit less choice,” Davidson said.

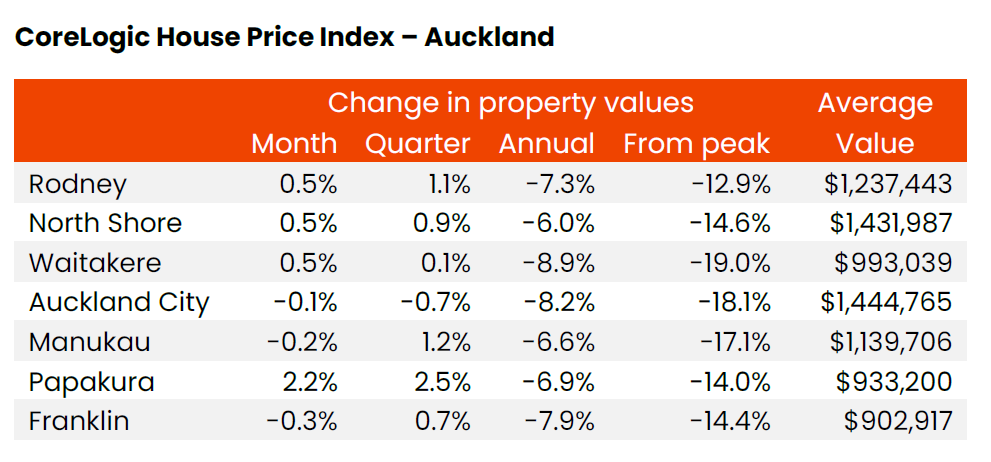

In Auckland, the average property value increased in October, continuing the trend from September; however, the rise was not uniform across all sub-markets. Papakura experienced a 2.2% surge over the month, while Rodney, North Shore, and Waitakere saw more modest value increases of 0.5%. In contrast, Auckland City, Manukau, and Franklin all posted modest declines in property values.

“This patchiness in property values by sub-region, even though wider market averages have started to turn around, could well remain a feature in the coming months, in Auckland and elsewhere too,” Davidson said. “Housing affordability is still stretched in many parts of NZ, and ‘higher for longer’ mortgage rates won’t do anything to ease that pressure.”

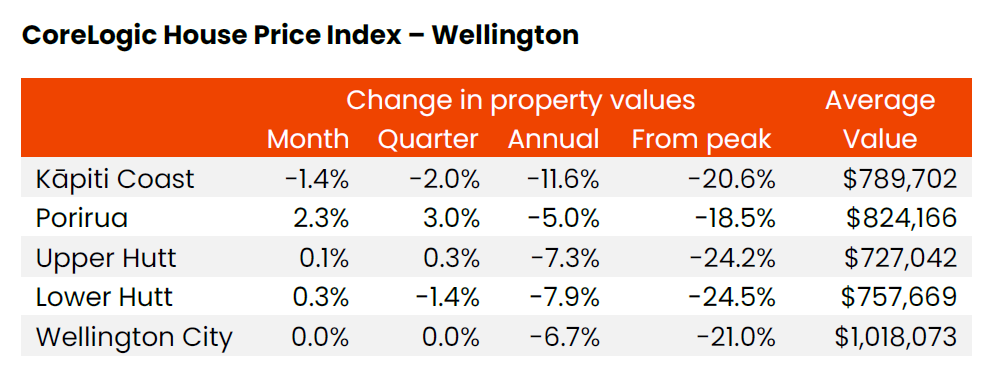

Wellington is another key area where signs of growth have emerged in recent months; however, there is still variability in the market.

“Porirua, for example, saw average values rise by 2.3% in October, but Lower Hutt, Upper Hutt, and Wellington City were more stable, and Kapiti Coast actually dropped by 1.4%,” Davidson said.

Outside the major urban centres, property value changes in October were a mixed bag. Rotorua, Gisborne, Whangarei, and Hastings saw robust increases of nearly 1% or more, while Invercargill, New Plymouth, and Whanganui experienced declines of at least 1%.

In the last three months, New Plymouth has seen a decline of nearly 3%, while Hastings has risen by nearly the same amount.

Davidson said this simply highlights the variability that persists from one region to another, and this pattern may continue in the months ahead.

The CoreLogic economist is expecting property values to continue rising in the upcoming months, although these increases may not be seen in every month or location.

“This ‘recovery’ could remain fairly subdued by past standards, given that housing affordability is still problematic, mortgage rates aren’t set to fall anytime soon, and that caps on debt-to-income ratios are still on the cards for 2024,” Davidson said.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.