A slow start to 2025 despite lower interest rates

Westpac’s senior economists, Michael Gordon, Satish Ranchhod, and Darren Gibbs (pictured above, from left to right), began the new year with a cautiously optimistic outlook for New Zealand’s economy.

Despite a series of weak economic updates at the end of the previous year, there are hopes for improvement in 2025, largely fuelled by lower interest rates.

However, the journey to recovery appears to be a prolonged one, as indicated by the initial data sets of the year.

Insights from the NZIER quarterly survey

The latest findings from the NZIER’s Quarterly Survey of Business Opinion, which serves as a precursor to quarterly GDP reports, initially suggested an uptick in business sentiment.

A net 9% of firms anticipate an increase in their activities in the coming months, with slight enhancements in hiring and investment plans.

Despite these positive expectations, the survey’s retrospective indicators tell a different story. A significant 26% of firms experienced a decrease in activity in the last quarter of the previous year, indicating a gap between expectations and current realities.

Economic indicators and growth forecasts

The backward-looking measure of the QSBO closely aligns with quarterly GDP developments and currently signals potential risks to economic growth projections.

Despite these concerns, anomalies in quarterly GDP data, such as the recent resolution of low hydro lake levels boosting renewable electricity generation, suggest some upcoming positive adjustments.

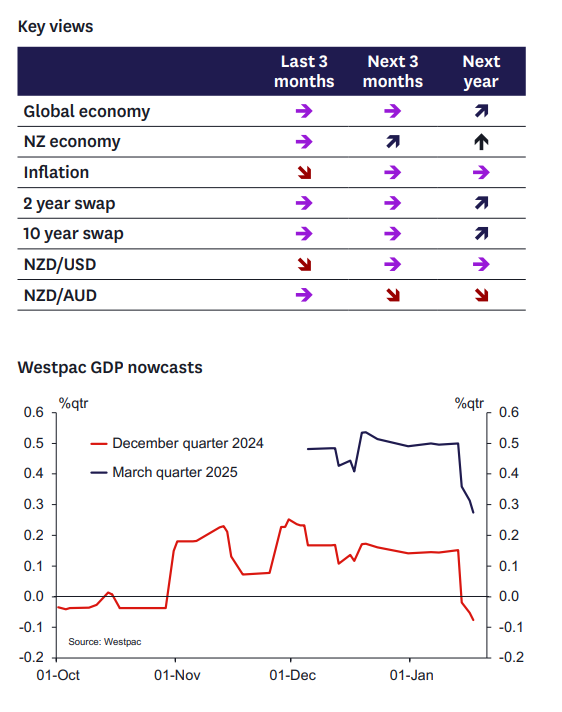

“We’re sticking with our forecast of a 0.3% rise in the official GDP figures for Q4, even though the underlying picture was still weak on many fronts over that time,” the Westpac economists said.

Labour market and housing sector developments

Towards the end of last year, there were emerging signs of stabilisation in the labour market, with a modest 0.3% increase in filled jobs reported in November.

Additionally, homebuilding consents saw a 5% increase in November, hinting at a potential uplift in the housing sector, driven by lower interest rates and relaxed regulatory frameworks.

Challenges in household economics

However, broader economic challenges remain, with households continuing to feel the pinch.

Stats NZ reported no growth in household incomes from March to September, with unemployment rising to 4.8% and economic activity shrinking by approximately 2%.

“Households with mortgages are now spending around 20% of their disposable incomes on interest costs, up from about 16% prior to the pandemic,” the economists said, underlining the increasing financial pressures on families.

Inflation trends and monetary policy outlook

Consumer price inflation has slowed to 2.2% annually as of September, down from over 7% in previous years, indicating easing price pressures.

With inflation expected to dip further to 2.1%, according to Westpac's projections, there is speculation that the Reserve Bank of New Zealand (RBNZ) may cut rates by another 50 basis points in the upcoming February meeting.

Fiscal concerns and government spending

The fiscal outlook remains dim, with the latest updates suggesting potential increases in government borrowing unless spending controls are enforced as projected.

“Unless the government can control spending as tightly as predicted in the HYEFU, further increases to the government's borrowing programme seem likely over time,” the Westpac economists said.

Access the full Westpac report here.