Jump to winners | Jump to methodology

|

Meet the New Zealand mortgage brokerages improving conversion rates, managing tighter lending conditions and helping borrowers navigate increasingly complex approval pathways as settlement conditions become more demanding. This year’s NZ Adviser’s Top Brokerages honourees reveal how the country’s leading firms are adapting in a more operationally complex market |

|

|

More deals in play, tougher deals to close |

New Zealand’s mortgage market is generating more lending activity again, but getting deals through to settlement is becoming more complicated. Lower borrowing costs and rising refinancing volumes are bringing borrowers back into the market, yet lenders remain selective, approval pathways have tightened and buyers are taking longer to commit.

For the country’s top brokerages, the result has been a significant shift in how deals are qualified, structured and progressed. The firms leading NZ Adviser’s Top Brokerages 2026 ranking are putting greater focus on front-end assessment, lender matching, file progression and borrower verification as settlement conditions become increasingly complex.

Nick Hakes, chief executive of Financial Advice New Zealand, says the strongest advice businesses are combining technical capability with a stronger focus on customer experience as technology becomes more embedded across mortgage workflows and client communication.

“When interacting with the best advice practices globally, I could sum them up as having excellent technical expertise combined with a relentless pursuit of the client experience as their competitive advantage,” he says.

Produced through brokerage submissions, aggregator verification and NZA research, the Top Brokerages 2026 ranking identifies the highest-performing mortgage advisory firms across New Zealand. From a pool of 52 nominees, the 42 winners were assessed on settlement volumes, productivity per adviser, conversion rates and loan book performance across all loan types during the 2025 calendar year.

The ranking recognises firms generating lending activity while consistently progressing borrowers through tighter approval conditions. In a market where lender fit, file quality and workflow discipline carry growing commercial importance, the report highlights the brokerages translating brokerage capability into settlement performance.

The annual ranking includes firms operating at different levels of scale and maturity. Loan book values among this year’s winners ranged from $125,105 to $6 billion, reflecting the award’s focus on conversion, productivity and brokerage performance rather than size alone.

The New Zealand mortgage market |

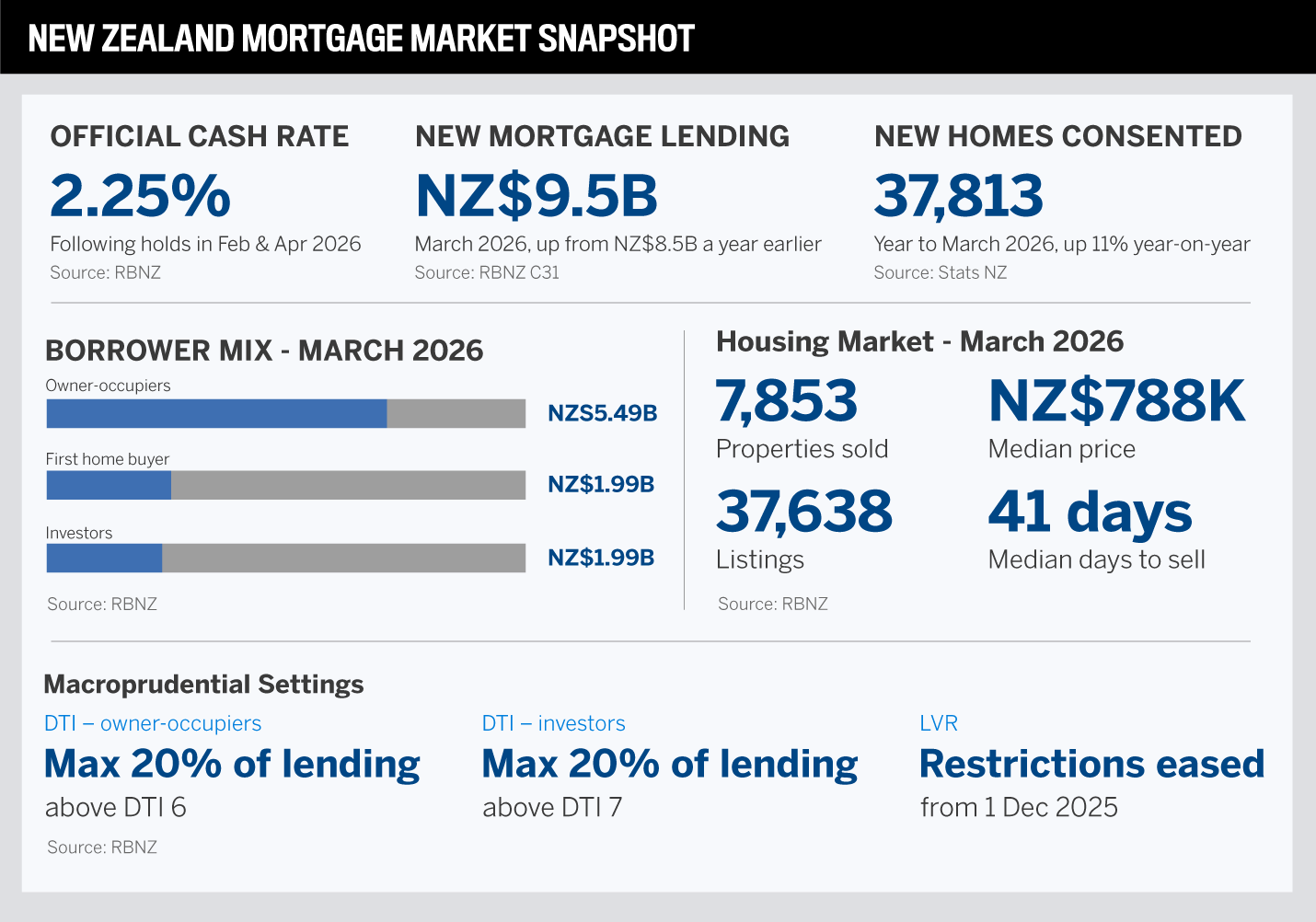

The conditions behind NZA’s Top Brokerages 2026 ranking point to a market with more lending activity, more choice for borrowers and greater complexity at the approval stage. The latest data shows rising mortgage volumes, elevated housing inventory, active first home buyer demand and a growing new-build pipeline, while debt-to-income (DTI) settings and servicing scrutiny continue to shape which borrowers progress to settlement.

Avanti Finance general manager of property Ian Boyce says the brokerage channel originated around 60% of property lending in 2025, reflecting a growing borrower demand for independent advice, broader lender access and more personalised service.

Lending activity has recovered, but settlement conditions remain uneven |

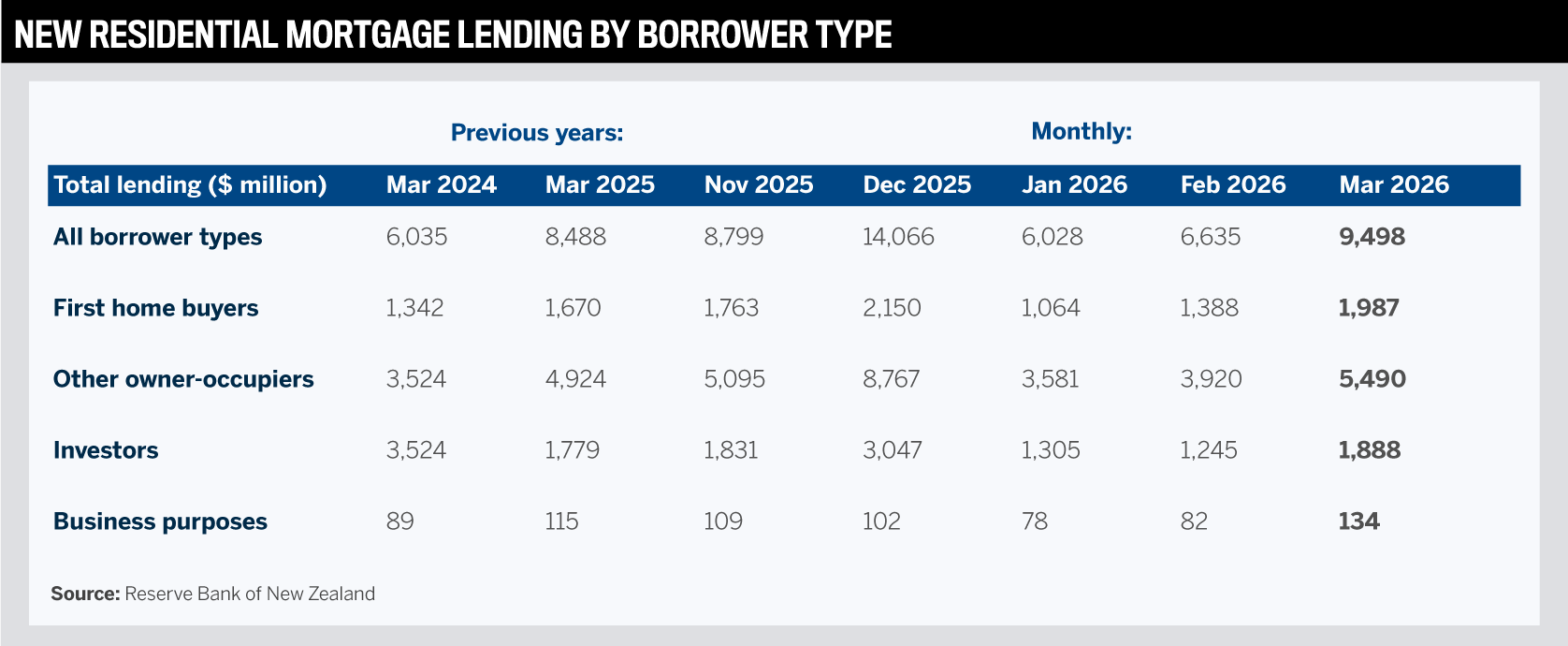

New residential mortgage lending reached NZ$9.498 billion in March 2026, up from NZ$8.488 billion a year earlier, according to Reserve Bank data. Activity has recovered across owner-occupiers, first home buyers and investors, increasing the volume of business entering brokerage pipelines.

More lending activity, however, has not automatically translated into easier settlements. Borrowers are taking longer to commit, lenders continue to apply tight servicing standards and more applications are being assessed through a narrower credit lens.

Several award-winning brokerages described earlier qualification as critical to protecting conversion. The team at Plaxo Mortgages has increased front-end assessment, reviewing servicing position, account conduct and lender policy fit before submission. Rhino Mortgages focuses on collecting nearly all supporting documentation during the first client meeting to reduce lender back-and-forth and compress approval timelines.

For advisers, the work increasingly involves identifying servicing risks earlier, testing lender fit more carefully and building applications capable of withstanding tighter verification requirements before files reach approval.

Brokerages are using repricing activity to keep refinance pipelines active as borrowers roll off higher fixed-rate terms.

Advisers are spending more time explaining fixed-term trade-offs as rate expectations remain unsettled.

Servicing buffers and household expense assessments continue to limit borrowing capacity despite lower rates.

First home buyers remain central to brokerage activity |

First home buyers continue to account for a large share of lending demand, increasing the amount of support required around deposit strategy, servicing position, budgeting and lender selection before applications proceed to formal approval.

For these borrowers, detailed preparation is becoming more important. Rhino Mortgages identified 5% deposit lending as one area where early coaching, structured qualification and comprehensive diary notes can reduce lender questions and improve approval flow for first home buyers.

Investors have also returned to the market in greater numbers, borrowing NZ$18.1 billion during 2025, up 36% year on year, according to the Reserve Bank of New Zealand - Te Pūtea Matua. Advisers say investor activity remains selective, with borrowing appetite still heavily influenced by servicing rules, rental yields and interest rate expectations.

Early structuring and pre-approval preparation are reducing rework later in the process.

Deposit composition and servicing position continue to influence lender appetite.

Investor lending remains active, though approvals are still highly policy-sensitive.

Credit policy continues to shape settlement outcomes |

DTI limits and loan-to-value ratio settings remain central to how banks allocate mortgage lending. While LVR restrictions were eased from December 2025, DTI speed limits continue to cap the share of higher-debt lending banks can undertake.

Those settings are reinforcing the importance of lender fit and application quality. Advisers say small differences in income verification, expense treatment or supporting documentation can materially alter approval outcomes between lenders.

The brokerages featured in this report described a common pattern of increasing assessment work before submission. Plaxo Mortgages has intensified front-end qualification and lender policy matching, while Squirrel Mortgages uses automated data collection and verification to assess borrower position earlier in the lending process. Star Mortgage & Insurance (SMI) pointed to test rates, ACC levy changes and elevated borrowing costs as practical constraints reducing borrowing capacity before applications reach the approval stage.

DTI settings continue to constrain borrowing capacity for some applicants despite lower interest rates.

Bank appetite for higher-risk lending can change quickly as allocation limits fill.

Incomplete documentation and servicing gaps remain common causes of delayed approvals and failed settlements.

Housing conditions are balanced rather than momentum driven |

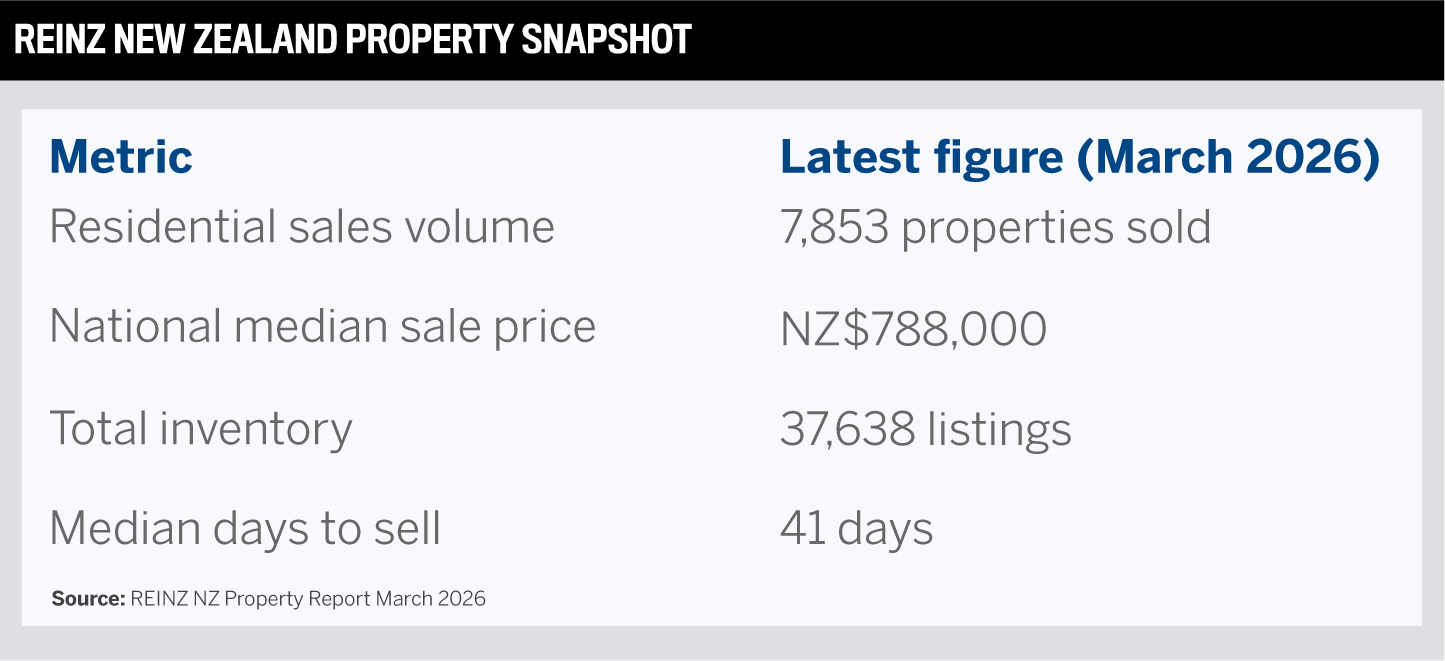

REINZ March 2026 data showed sales activity holding broadly stable while inventory remained elevated and buyers retained greater negotiating power.

For brokerages, this has increased the importance of maintaining contact with borrowers throughout longer decision cycles. Deals are spending more time in pipeline stages, increasing exposure to policy expiry, valuation changes or borrower fatigue before settlement.

Some winners are responding by tightening file timing and client communication. Plaxo Mortgages noted that buyers and builders are taking longer to commit, prompting the brokerage to accelerate document collection and communication before policy or market settings change.

Borrowers are comparing more properties and financing options before committing.

Longer transaction timelines are increasing the importance of follow-up discipline.

Delays between pre-approval and settlement are creating greater exposure to policy changes and reassessment risk.

New-build lending is creating a different set of operational demands |

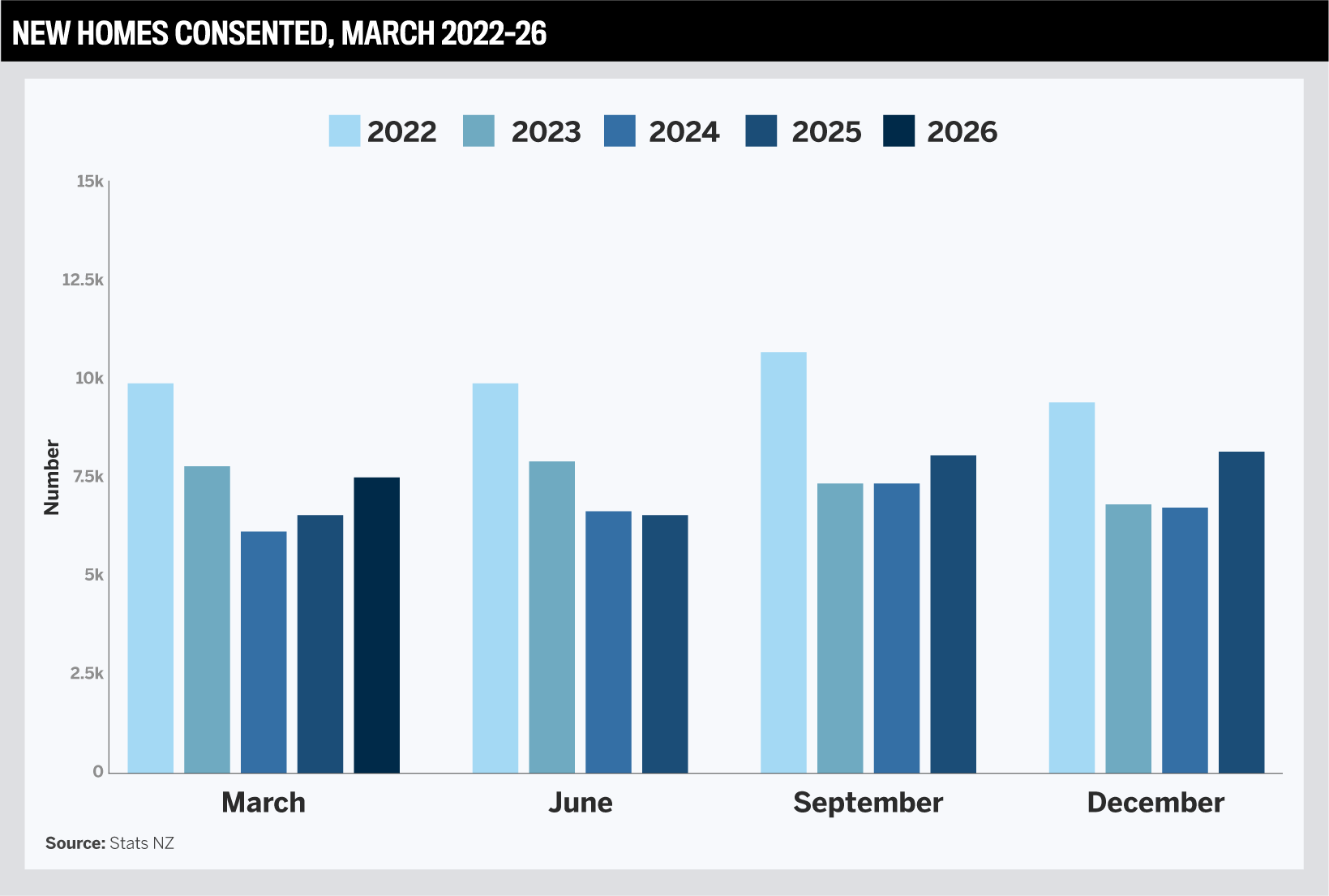

Residential building activity has recovered over the past year, with 37,813 new homes consented in the year ended March 2026, up 11% year on year, according to Statistics New Zealand.

That increase is creating additional lending opportunities, particularly around construction finance and staged drawdown lending. It is also increasing the operational complexity attached to some applications, particularly where project timelines, valuations and builder requirements evolve during the lending process.

Boyce remarks that leading brokerages continue to differentiate themselves through specialist lending capability, tailored solutions and diversified service offerings as more borrowers fall outside standard bank criteria. “Innovation plays a critical role,” he says. “Initiatives such as investing in CRM systems and early adoption of AI and automation help enhance speed, efficiency and customer experience.”

Several winners pointed to construction finance as a specialised source of lending activity. Rhino Mortgages built a significant portion of its first-year volume through construction lending, including multi-dwelling projects requiring more specialised lender structuring. Squirrel Mortgages identified construction finance as one area where non-bank lending pathways can support borrowers outside standard bank criteria.

Construction lending often requires more coordination between brokers, lenders, builders and valuers.

Project delays and feasibility changes can affect settlement timing and approval validity.

Lender appetite for new-build lending continues to vary materially across the market.

Operating structure is becoming a larger competitive factor |

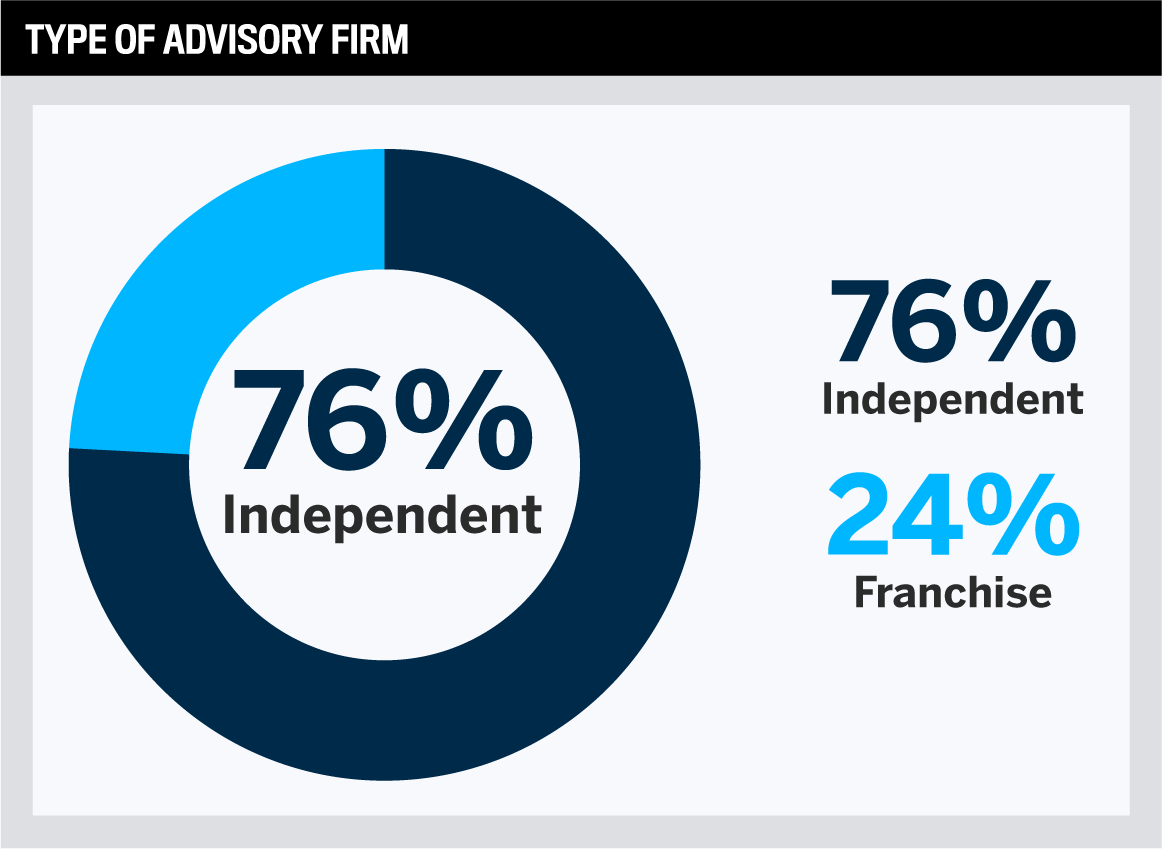

The mortgage advice sector spans sole advisers, boutique firms and scaled multi-adviser brokerages operating within the same regulatory framework. Preliminary Financial Markets Authority data for 2025 shows New Zealand’s advice sector included more than 9,100 financial advisers operating across approximately 1,550 licensed financial advice providers.

Leaders from the top brokerages suggest the operating structure is becoming a larger dividing line between firms. The models vary. SMI pointed to full-file auditing and structured adviser training. Plaxo Mortgages standardised the workflow from discovery through settlement. Squirrel Mortgages uses head-office support to keep advisers focused on clients, while The Mortgage Girls relies on shared templates and collaborative process improvements to help a smaller team move quickly.

As compliance and workflow demands increase, larger firms are leaning more heavily on standardised processes, administrative support and technology integration. Smaller firms often rely more directly on adviser capability and client relationships.

Workflow consistency is becoming more important as application volumes recover.

Administrative support and quality control are reducing avoidable delays and rework.

Firms with stronger internal systems are better positioned to manage longer settlement cycles.

Technology is moving further into mortgage workflow management |

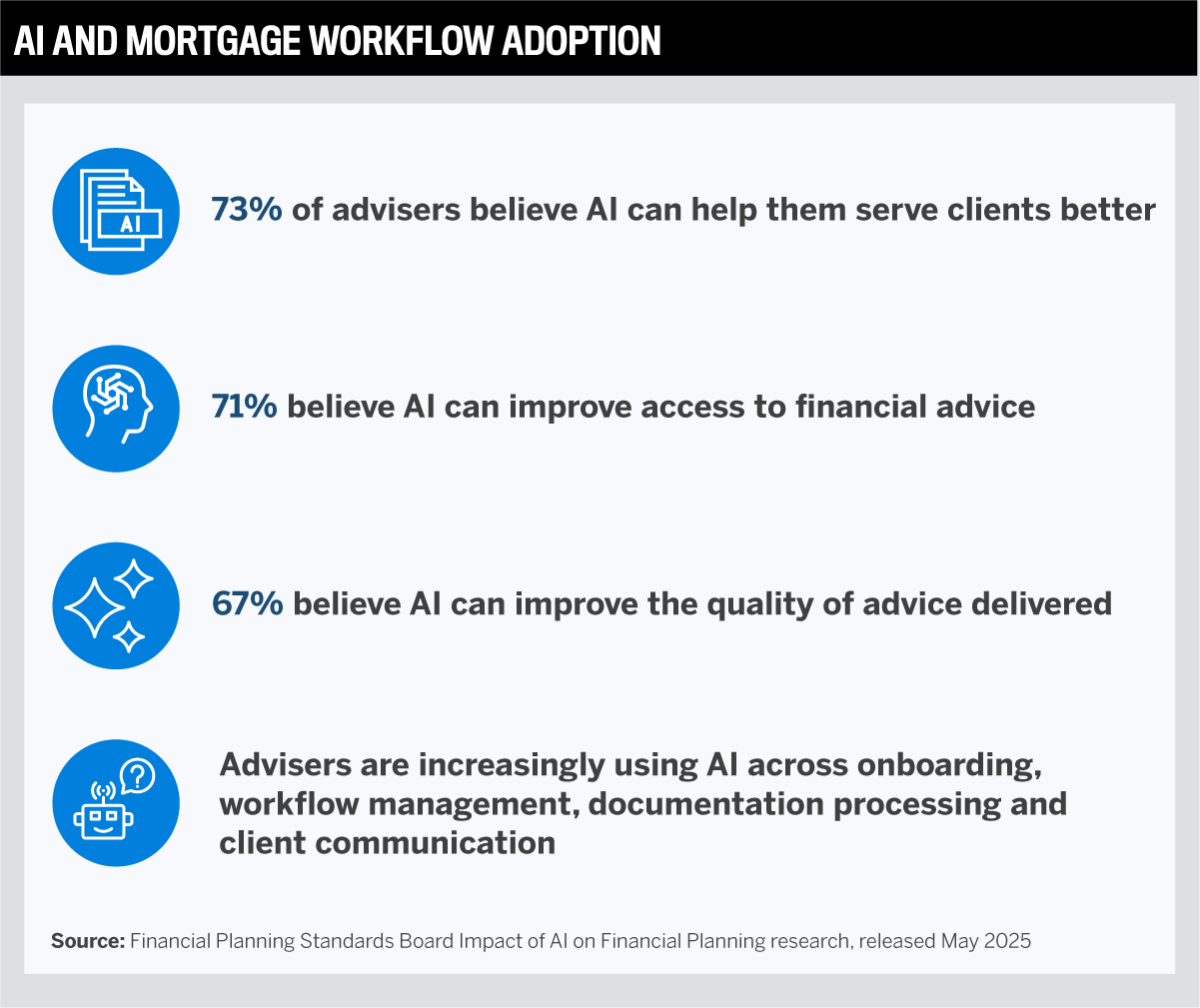

Brokerages are investing more heavily in technology as they look to improve processing capacity without materially increasing headcount. Artificial intelligence tools are increasingly being used across onboarding, document analysis and borrower communication, while some firms are building more integrated lending systems.

According to Boyce, AI is increasingly being used to accelerate document processing, support credit decisioning and strengthen fraud detection. He says the biggest opportunity is reducing the time between application and unconditional approval.

“Tech is reshaping the mortgage industry,” he says. “Open banking integrations for income verification, faster ID verification and credit checks are some of the things we’re already seeing.”

Financial Advice New Zealand’s Hakes says growing technology adoption is increasing the importance of distinguishing personalised advice from general financial information. “The distinction needs to be made between what is impartial, personal advice and what is financial information and consumers need to be able to understand the difference.”

The strongest technology examples came from brokerages using automation before adviser review. Squirrel Mortgages has automated bank statement collection, credit checks and property-data capture through proprietary systems. The Mortgage Girls uses transcription, templates, documentation portals and bank-statement tools to accelerate back-end processing while maintaining tailored advice.

AI tools are increasingly being used to reduce administrative workload and accelerate document processing.

Workflow automation is helping brokerages manage larger application pipelines more consistently.

Faster processing is becoming more commercially important as competition for settled lending intensifies.

The best mortgage advisory firms in New Zealand |

Star Mortgage & Insurance (SMI) | Auckland |

|

Five years after launching with two founders, Star Mortgage & Insurance (SMI) has grown into one of New Zealand’s highest-volume mortgage advisory firms, with 20 licensed advisers and two more currently in training. The Auckland-based brokerage settles over $800 million annually across residential mortgages, non-bank lending, property finance and development funding, while also operating integrated insurance, legal and property management divisions.

General manager and financial adviser Eric Hao describes the firm’s lending mix as extending well beyond standard residential mortgages. SMI works across non-bank lending, large-scale subdivision projects and full development funding, including projects spanning land acquisition, subdivision, construction and end-sale funding.

“We don’t just focus on mortgages,” Hao says. “A big part of our settlement is actually non-triple CFA and also quite a substantial portion with property finance and property development.” Some projects move through the full development cycle from acquisition through construction and sale. “You settle one of those deals, and, effectively, you’ve done 15 mortgages.”

Operating in a dynamic market |

Changing lending conditions have also increased the importance of timing and borrower preparation. Hao points to higher test rates, increased borrowing costs and ACC levy changes as factors continuing to affect borrowing capacity, with advisers spending more time helping clients weigh the risks of delaying approval decisions.

The brokerage has also differentiated itself through full-file auditing and internal adviser development. Rather than reviewing only a sample of files each year, SMI audits every application throughout the lending process and again after settlement. The firm also recruits staff from outside financial services, including nursing, hospitality, retail and real estate, before training them internally into licensed mortgage advisers through a structured development program.

For Hao, the approach reflects the leadership team’s longer-term focus on scaling the business while continuing to build internal capability and consistency across the adviser team.

Q&A: SMI

|

What is one part of your operating model that most consistently improves performance, and how does it show up in your day-to-day workflow?

“The biggest challenge in our industry, at least in New Zealand, is compliance. As far as I’m aware, we’re the only organisation that actually audits every single one of our applications. We’re selling over $800 million, so imagine how many deals those equate to. Most of the market is auditing only a handful of deals per adviser each year. We audit every deal throughout the process and again once it settles. That gives advisers confidence to focus on sales and business development because there’s a separate internal team reviewing every file. If something is missing, we identify it immediately rather than finding it much later. They’re not scared to do a job and scared to pick up another deal because they’re thinking, ‘Oh my God, I might lose my license because I haven’t done my first one correctly.’”

Squirrel | Auckland | No. 2 ranked

|

Squirrel has continued strengthening its position as one of New Zealand’s leading mortgage advisory firms by investing heavily in proprietary technology, automated data integration and specialist support infrastructure. Group head of advisory Callan Wayne-Bowles says the brokerage has focused on improving how borrower information is captured, verified and assessed as lending conditions become more demanding.

Wayne-Bowles explains that Squirrel has expanded the use of automated bank statement collection, automated credit checks and integrated property data to help advisers understand a borrower’s position earlier in the lending process rather than waiting for lenders to validate information later. The brokerage develops its systems internally, allowing the firm to tailor workflows around advisers and borrowers instead of relying entirely on third-party platforms.

“One thing that’s a little bit unique about Squirrel is we have proprietary tech, so we build our systems in-house,” he says. “That enables us to have really bespoke workflows to help the customer and to help our advisers.”

Looking to the future |

The brokerage’s technology investment is designed to reduce manual processing rather than replace adviser interaction. Automated workflows and third-party data integrations are helping advisers spend less time processing documentation and more time guiding borrowers through major financial decisions.

Squirrel has also expanded its specialist and non-bank lending capabilities, particularly across construction finance, self-employed borrowers and high-net-worth clients who may fall outside standard bank lending criteria. The brokerage’s funding solutions provide additional lending pathways when traditional bank finance is unavailable, while also giving intermediary partners access to a broader range of options for more complex borrowers.

The combination of internally developed systems and expanded specialist lending capability has helped position Squirrel as a brokerage operating across both traditional mortgage advice and more specialised funding solutions as lending conditions continue to tighten.

Q&A: Squirrel Mortgages

|

What is one part of your operating model that most consistently improves outcomes, and how does it show up in your day-to-day workflow?

“We have a lot of support for our advisers. A lot of mortgage advisers are kind of jacks of all trades, and they’re running their own small businesses, and they’re sort of doing everything. We’re a different model where we have a lot of our head office or support team involved, and it allows our advisers to really be specialists and experts. They’re not having to juggle multiple things. They’re just really focusing on the customer. That allows us to really ensure that the centre of the adviser’s focus is just looking after the customer.”

Plaxo Mortgages | Auckland | No. 3 ranked

|

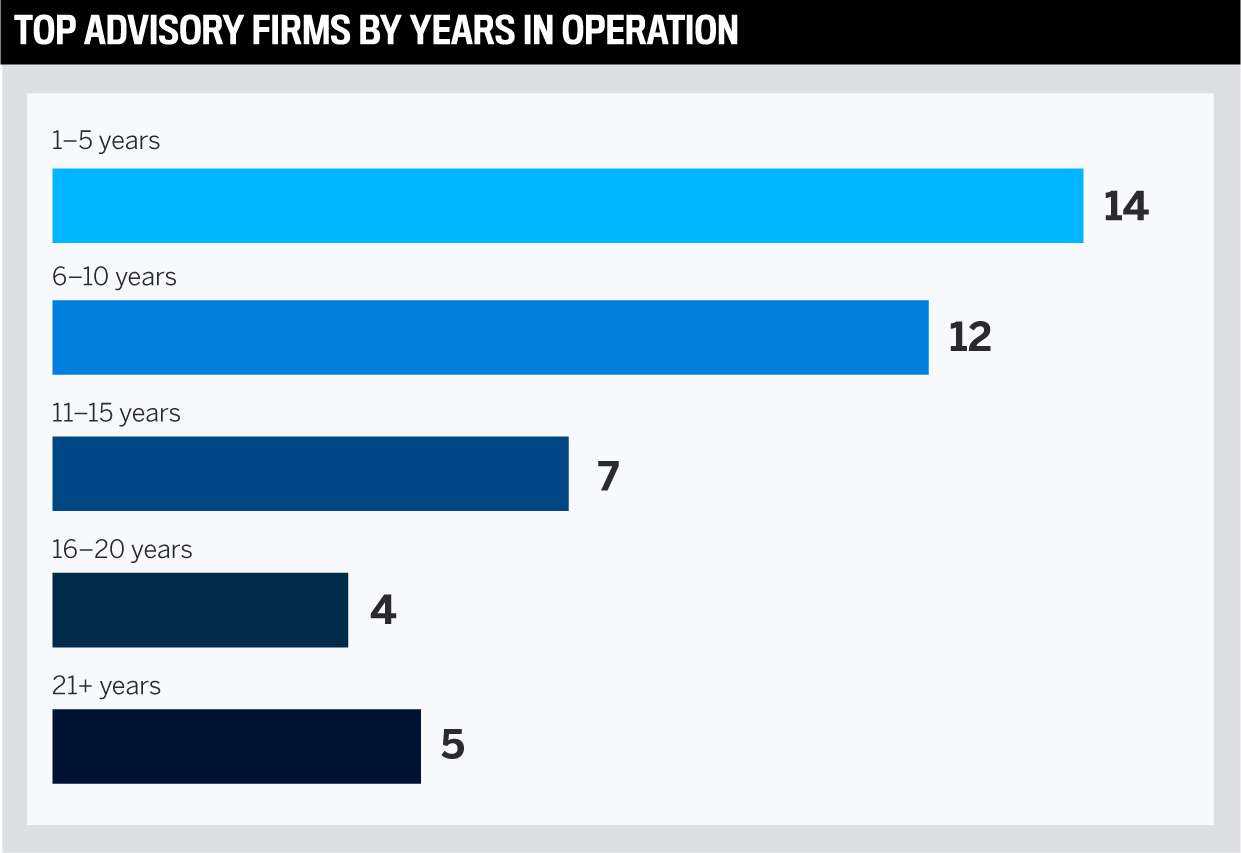

After more than 20 years in operation, Plaxo Mortgages continues to rank among New Zealand’s leading mortgage advisory firms by adapting to longer approval timelines and increasingly fragmented lender policy settings. Led by director Chang York, the brokerage has shifted more assessment work to the earliest stages of the lending process as buyers take longer to commit and approval pathways become more complex.

The brokerage now spends more time stress-testing servicing positions, reviewing account conduct and identifying policy concerns before applications are submitted. Advisers are also spending more time structuring deals rather than focusing solely on product selection, particularly as lender policy differences widen across the market.

“In the current market, the lender policy difference matters a lot more,” York says. “Matching the clients to the right lender and presenting the right structure up front has significantly improved our conversion rate.”

Service delivery is key |

Managing borrower expectations has also become a larger part of the brokerage’s day-to-day work. York notes that many clients still expect the lowest interest rate, the highest cashback offer and fast approval timelines simultaneously, despite tighter lending settings and changing bank appetites.

As transaction timelines lengthen, the firm has tightened document collection and communication standards to reduce delays later in the process. Buyers are taking longer to purchase or build, while lending conditions can materially change within a matter of weeks, increasing the importance of progressing applications quickly once clients are ready to proceed.

Q&A: Plaxo Mortgages

|

What is one part of your operating model that most consistently improves outcomes, and how does it show up in your day-to-day workflow?

“We have a very structured workflow across the client journey. We want to make sure clients get very consistent customer service. From discovery and client document collection to lender selection, submission and also through settlement, every stage has different processes and communication standards. We have very clear adviser checklists. Brokers aren’t working by their own standard. They’re working to the Plaxo standard. We also have pipeline reviews and milestone updates through the CRM system to make sure every file is progressing correctly and meeting lender requirements before submission.”

The Mortgage Girls | Christchurch | No. 14 ranked

|

Over more than a decade in business, The Mortgage Girls has built its brokerage model around personalised advice supported by increasingly efficient back-end systems. Co-founder and head mortgage adviser Elyce Peters says the firm is continually refining how it qualifies, structures and progresses deals as lending conditions, insurance costs and servicing settings continue to change.

Rather than following a standard product pathway, advisers focus on understanding each borrower’s individual circumstances before structuring lending recommendations around affordability, goals and lender fit. Peters explains that changing market conditions have increased the importance of tailoring advice more closely to each client’s situation rather than relying on fixed processes.

“It really drills down to zoning in on that individual client, figuring out what’s going to be best for them, and then creating a customised package for them,” she says. “For us, it’s about creating efficiencies in the background so that the rest of the stuff that takes a lot more time, we can do with a lot more efficiency.”

Embracing tech |

The brokerage has expanded its use of technology to reduce manual processing for both advisers and clients. Peters points to transcription tools, AI-assisted templates, documentation portals, Akahu, bankstatements.com and Contented as part of a broader effort to speed up administration while preserving tailored borrower advice.

Technology, however, is only part of the process. Advisers still need to identify inconsistencies, ask deeper questions and investigate further when borrower information does not feel right, particularly as AI-generated documents and fraud risks become harder to detect.

The brokerage’s approach has also allowed the firm to adapt quickly as lending conditions continue to evolve. Peters says the business regularly updates workflows, templates and internal systems as new technologies and compliance requirements emerge.

Q&A: The Mortgage Girls

|

What is one part of your operating model that most consistently improves outcomes, and how does it show up in your day-to-day workflow?

“We have a whole behind-the-scenes setup which have templates for emails, templates for different statements of advice and lots of different information that our advisers are able to access in one spot. That’s consistently being updated all the time. We also have quite a horizontal management kind of structure. Advisors can’t do their job without support, and the support can’t do their job without advisors. If someone finds a process that works really well, then we share it so everyone can use it. Because we’re small enough, we can make changes quite quickly compared to some of the bigger firms.”

Rhino Mortgages | Auckland | No. 31 ranked

|

Just one year after launching, Rhino Mortgages has already secured a place among New Zealand’s top brokerages. The Auckland-based firm is led by senior mortgage adviser Ankit Tomar, whose 16-year banking career included roles with BNZ, ASB and Westpac before establishing Rhino Mortgages independently.

Tomar says the brokerage has built its early momentum around construction finance, complex lending and highly structured upfront qualification. The brokerage focuses heavily on upfront qualification and document preparation before files are submitted to lenders.

“Doing it right the first time,” Tomar says. “In my first meeting, I ensure that I collect 99% of the documentation.” He adds that preparation reduces lender back-and-forth and shortens approval timelines. “Some of my customers sign a finance condition for almost 10 days, but I get their loans approved in two days.”

Becoming specialists |

Construction lending has become a major part of the brokerage’s lending mix. Out of approximately $75 million settled during Rhino Mortgages’ first year, Tomar says more than $30 million came from construction lending, including multi-dwelling projects many advisers avoid because of their complexity.

The brokerage has also expanded relationships outside Auckland, including development and construction connections in Queenstown and Christchurch, with Tomar regularly travelling to meet borrowers and developers in person.

Q&A: Rhino Mortgages

|

What is one part of your operating model that most consistently improves performance, and how does it show up in your day-to-day workflow?

“I think what I’m doing differently is connecting with customers from day one and ensuring they understand every step of the lending process rather than me presenting myself as the specialist and saying, ‘Leave it with me.’ I’ll draft a flowchart for them, and it’s really easy for them to follow. At the end of the meeting, I ask, ‘Are there any questions?’ and usually they have none because everything has been explained properly. One area where we’re growing significantly is first home buyers with 5% deposits. There’s complexity in that space, but I’ve made it easier for clients to get approval seamlessly without too many questions being asked. Everything is documented in the diary notes, and that helps keep the process moving.”

Industry expert Q&A |

Nick Hakes

|

Generally speaking, how would you characterise the New Zealand brokerage sector in 2026?

“The advice profession is constantly evolving and responding to shifts in consumer expectations, new technologies, government policy and regulatory settings and competitive market conditions. What remains constant, and mission-critical to our ongoing relevance, is our commitment to putting the interests of the client before our own.”

What types of services and initiatives do you feel are industry-leading and driving brokerages forward in New Zealand?

“Two almost contrarian themes are playing out in the industry. Firstly, in our hyper-digitised world, the need for deeper human connection has never been greater. Impartial financial advice that helps people clarify goals, identify issues and tailor client-centric solutions that improve financial and emotional wellbeing will continue to be actively sought out by consumers. At Financial Advice New Zealand, we see the next phase of advice being defined by an adviser’s ability to understand behaviour as deeply as they understand the family balance sheet. Embedding behavioural psychology into professional practice is becoming increasingly important. Secondly, there is the continued adoption of technology throughout the advice process. Implementation can be both externally and internally focused for advice practices. When implemented well, technology can create significant gains in efficiency and improve the client experience. The risk comes when businesses fail to define the problem they are trying to solve and deploy technology for purposes it was never designed to address.”

What role does technology play in New Zealand’s leading mortgage brokerages, and where does AI fit into that?

“AI, like any technology, follows a pattern of adoption, from innovators and early adopters through to the middle majority and laggards. We are seeing AI adopted across mortgage businesses in much the same way. What’s critical is ensuring regulation and industry practice standards keep pace with adoption and continue delivering positive outcomes for consumers.”

Do you feel brokerages are growing in importance in New Zealand relative to banks and other channels, and if so, why?

“If the question is whether Kiwis are financially better off having access to quality financial advice, then the answer is unequivocally yes. Consumers can access advice through different channels, and that’s part of a vibrant and diversified marketplace. Recent FMA research suggested that 28% of people had used a financial adviser over the past 12 months, yet two-thirds of people think about their financial situation at least weekly. From Financial Advice New Zealand’s perspective, there has never been a greater need for financial advice.”

Ian Boyce

|

Ian Boyce has over 35 years of experience in financial services, banking and insurance. He has held several senior leadership roles at ASB Bank, driving growth, profitability and strategic initiatives. Since joining Avanti Finance as general manager, property in 2022, Ian has led one of the industry’s largest and award-winning property lending teams. Avanti Property Lending has made significant contributions consistently to Avanti Finance Group’s rapid growth, particularly in New Zealand’s highly competitive property market.

For top brokerages, how important is the service side of the business and connecting/building trust with clients outside of having technical mortgage expertise?

“A trusting relationship with customers is a major differentiator. Behind every application is a life story. Successful brokerages take time to listen to customers’ needs and circumstances and provide personalised service, backed by solid technical expertise.”

Do you feel brokerages are growing in importance in NZ relative to banks and other channels, and if so, why is that?

“Yes. The brokerage sector has consistently gained market share over the years, with further growth potential as seen in markets like Australia. Customers increasingly value broader access to credit, specialist expertise and personalised guidance, particularly in today’s evolving market conditions and more complex lending environment.”

How top mortgage brokerages are handling more complex lending |

New Zealand’s mortgage market is no longer defined by a shortage of lending activity. Borrowers are returning, refinancing volumes have recovered, and competition between lenders has become more active again. Yet the brokerages featured in NZA’s Top Brokerages 2026 ranking show that the harder part of the market now begins after the enquiry stage.

Across the country’s leading firms, success is increasingly being determined by how well brokerages manage complexity before applications ever reach a lender. The strongest performers are investing more heavily in front-end qualification, workflow discipline, documentation quality, lender matching and operational support as approval conditions become more demanding and borrowers take longer to commit.

What stands out across this year’s winners is that there is no single blueprint for scale or growth. Some firms are building proprietary technology and specialist support infrastructure. Others are focusing on construction finance, standardised workflows, collaborative operating models or highly personalised borrower advice. What connects them is an ability to adapt operationally without losing sight of the client experience.

That balance may become the defining characteristic of the next phase of mortgage advice in New Zealand. As automation moves further into onboarding, verification and workflow management, advisers are spending more time where borrowers still place the highest value: helping clients understand risk, structure decisions and move through increasingly complicated lending environments with confidence.

As Hakes says, “The advice profession is constantly evolving and responding to shifts in consumer expectations, new technologies, government policy and regulatory settings and the natural pressures of the competitive environment. What remains constant and mission-critical to our ongoing relevance is our commitment to putting the interests of the client before our own.”

The brokerages recognised in this year’s ranking are not succeeding because market conditions have become easier. They are succeeding because they have adapted more quickly to a market where advice, process, communication and operational consistency increasingly determine which deals reach settlement.

What does the NZA’s Top Brokerages 2026 report show? |

The NZA’s Top Brokerages 2026 report identifies the highest-performing mortgage advisory firms across New Zealand, selected from a pool of 52 nominees with 42 firms recognised as winners. Brokerages were assessed on settlement volumes, productivity per adviser, conversion rates and loan book performance across the 2025 calendar year. The report shows a market that has recovered in terms of lending activity – with new residential mortgage lending reaching NZ$9.498 billion in March 2026, up 12% year on year – but where getting deals through to settlement has become more operationally demanding. Loan book values among winners ranged from NZ$125,105 to NZ$6 billion, with average total settlements of NZ$339 million and an average conversion rate of 76.4%. Across the ranking, the firms performing best are those investing in front-end qualification, lender matching, workflow discipline and technology integration – translating brokerage capability into consistent settlement performance in a more complex approval environment.

What does a mortgage broker do? |

A mortgage broker acts as an intermediary between borrowers and lenders, assessing a client’s financial position, identifying suitable lending options across multiple banks and non-bank lenders and managing the application process through to settlement. Unlike going directly to a single bank, a broker provides access to a broad range of lenders and products and can structure applications to improve the likelihood of approval. In New Zealand, mortgage brokers are licensed financial advisers operating under the Financial Markets Conduct Act, with obligations to act in the client’s best interests.

How are mortgage brokers paid in New Zealand? |

Most mortgage brokers in New Zealand are paid by lenders through upfront commissions when a loan settles and trail commissions are paid on the ongoing loan balance over time. In most cases, borrowers do not pay fees directly to the broker. Brokers are required to disclose their remuneration arrangements to clients as part of their obligations under the Financial Markets Conduct Act so borrowers can understand how their adviser is compensated.

Why use a mortgage broker rather than going directly to a bank? |

Brokers provide access to a wider range of lenders and loan structures than any single bank can offer, which is particularly valuable when a borrower’s circumstances are complex or fall outside standard criteria. In New Zealand’s current lending environment, where DTI limits, LVR restrictions and tight servicing assessments are shaping which applications proceed to approval, matching the right borrower to the right lender at the right time has become a core part of the advice process. The brokerage channel originated around 60% of property lending in New Zealand in 2025, reflecting growing demand for independent guidance and broader lender access.

What is a conversion rate, and why does it matter? |

A conversion rate measures the proportion of mortgage applications or enquiries that progress through to a settled loan. It is a key indicator of brokerage performance because it reflects not just the volume of business coming through the door but also the quality of qualification, lender matching and file management that turns enquiries into completed transactions. Among the Top Brokerages 2026 winners, the average conversion rate was 76.4%, with stronger performers typically attributing their results to rigorous front-end assessment, structured workflows and early identification of servicing or policy risks before submission.

What are DTI limits, and how do they affect borrowers? |

DTI limits restrict the amount a borrower can borrow relative to their gross annual income. The Reserve Bank of New Zealand introduced DTI speed limits requiring that no more than 20% of owner-occupier lending can be issued at a DTI above 6 and no more than 20% of investor lending at a DTI above 7. In practice, this means some borrowers who can technically service a loan may still be declined if their total debt level is high relative to their income. For brokers, DTI settings have reinforced the importance of careful income verification, expense assessment and lender selection, as different banks manage their DTI allocations at different rates.

To establish this year’s line-up of the most prominent industry players, NZ Adviser invited brokerages in New Zealand to submit their accomplishments for the 2025 calendar year.

To be eligible, brokerages needed to have three or more loan writers in a single office headquartered in New Zealand. Aggregator information was also provided by applicants, and their aggregators were then required to verify the details submitted.

The application also asked for details such as the number of active brokers working at each company as well as the total loan book value and conversion rate. The nominees were evaluated across four areas: total loan book size, average settlements per loan writer, total settlements in the specified 12-month period and conversion rate.