How are market shifts impacting borrowing costs?

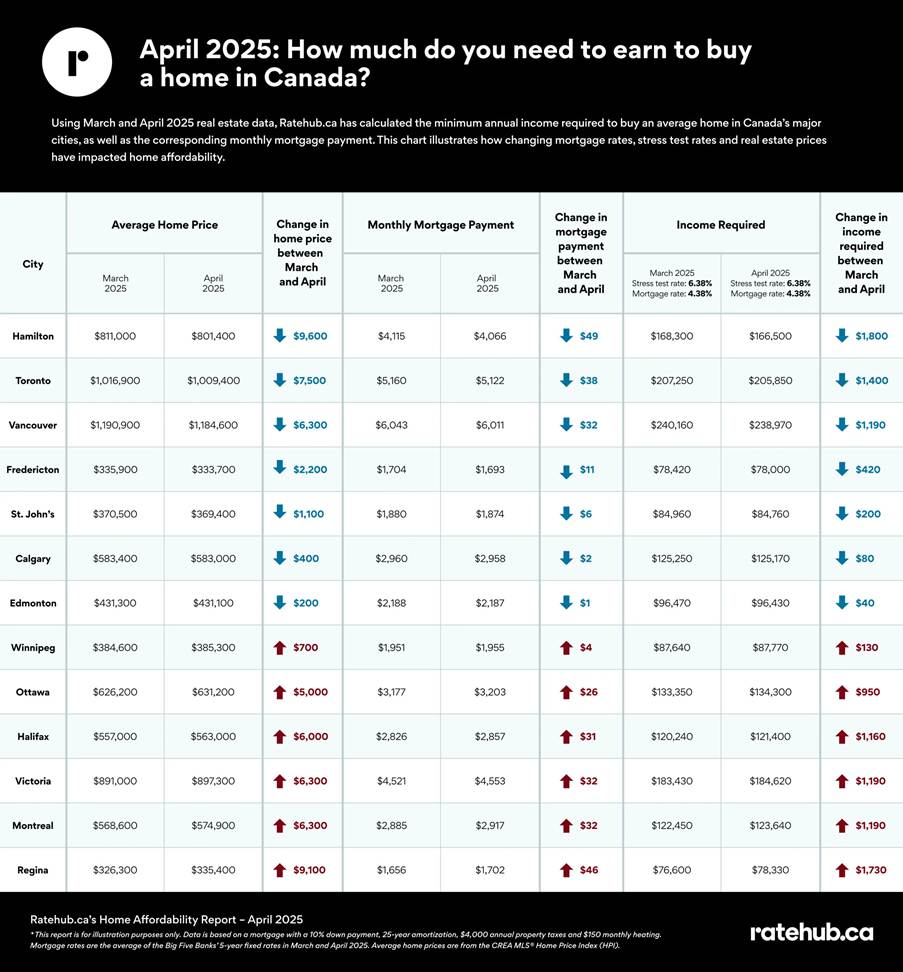

Seven of 13 major Canadian cities saw improved mortgage affordability in April as declining home sales led to lower real estate prices despite stagnant borrowing costs, according to Ratehub.ca’s latest affordability report.

The study found that while mortgage rates remained unchanged at 4.38% for five-year fixed terms, falling home prices in key markets helped reduce the income required to purchase an average home and lowered monthly mortgage payments.

Hamilton leads improvement, Regina bucks the trend

Hamilton experienced the most significant improvement, with buyers needing $1,800 less income to purchase the average home compared to March. Home prices in the Ontario city dropped by $9,600 to $801,400, the largest price decline among all cities studied. This translated to monthly mortgage payment savings of $49, or $588 annually.

Toronto followed closely, with average home prices falling $7,500 to $1,009,400. Prospective buyers there would need $1,400 less income to qualify for a mortgage, while monthly payments decreased by $38.

Vancouver, Canada’s most expensive market, also saw modest improvements with home prices dropping $6,300 to $1,184,600, reducing required income by $1,190.

“Month-over-month we saw a fairly even split between affordability worsening and improving amongst the 13 cities studied,” said Penelope Graham, mortgage expert at Ratehub.ca. “Since mortgage rates remained unchanged this month, home prices were what impacted home affordability in each of the cities.”

Regina recorded the steepest affordability decline, according to the report. Home prices there rose $9,100 to $335,400, requiring buyers to earn an additional $1,730 to qualify for a mortgage. Monthly payments increased by $46.

Other cities experiencing worsened affordability included Ottawa, Halifax, Victoria, Montreal and Winnipeg, with required income increases ranging from $130 to $1,190.

Sales decline impacts prices

The improvements largely stemmed from declining home sales activity. According to the Canadian Real Estate Association (CREA), national home sales dropped 9.8% year over year in April, with the steepest declines concentrated in Greater Golden Horseshoe markets including Toronto and Hamilton.

“A steep decline in home sales, coupled with building supply, has helped lower home prices in a number of Canada’s largest markets,” Graham said.

The Bank of Canada held its benchmark overnight lending rate steady at 2.75% in April, keeping mortgage rates largely unchanged. However, uncertainty remains about future rate movements as the central bank weighs inflation concerns against economic pressures from ongoing trade tensions.

Economists expect the Bank of Canada may implement two more rate cuts before the end of 2025, though the timing remains uncertain given mixed economic signals including rising unemployment and persistent inflation in some sectors.

What are your thoughts on recent market shifts the Canadian housing market is experiencing? Share your insights in the comments below.