Jump to winners | Jump to methodology

The market gave Canada’s best mortgage brokers little room to coast in 2024. After two years of rapid rate increases, the Bank of Canada finally held steady, but the pause didn’t offer much relief.

Buyers stayed on the sidelines, uncertain about where the market was heading. Many homeowners who reached the end of their mortgage term were met with higher payments and a very different lending environment than when they first signed.

Cameron Strong, author of Retirement Reimagined and a retired CPA who has held senior leadership positions in the public and private sectors for over two decades, agrees that the real estate market has been in bad shape in Canada for the last two years.

He points to the following market challenges:

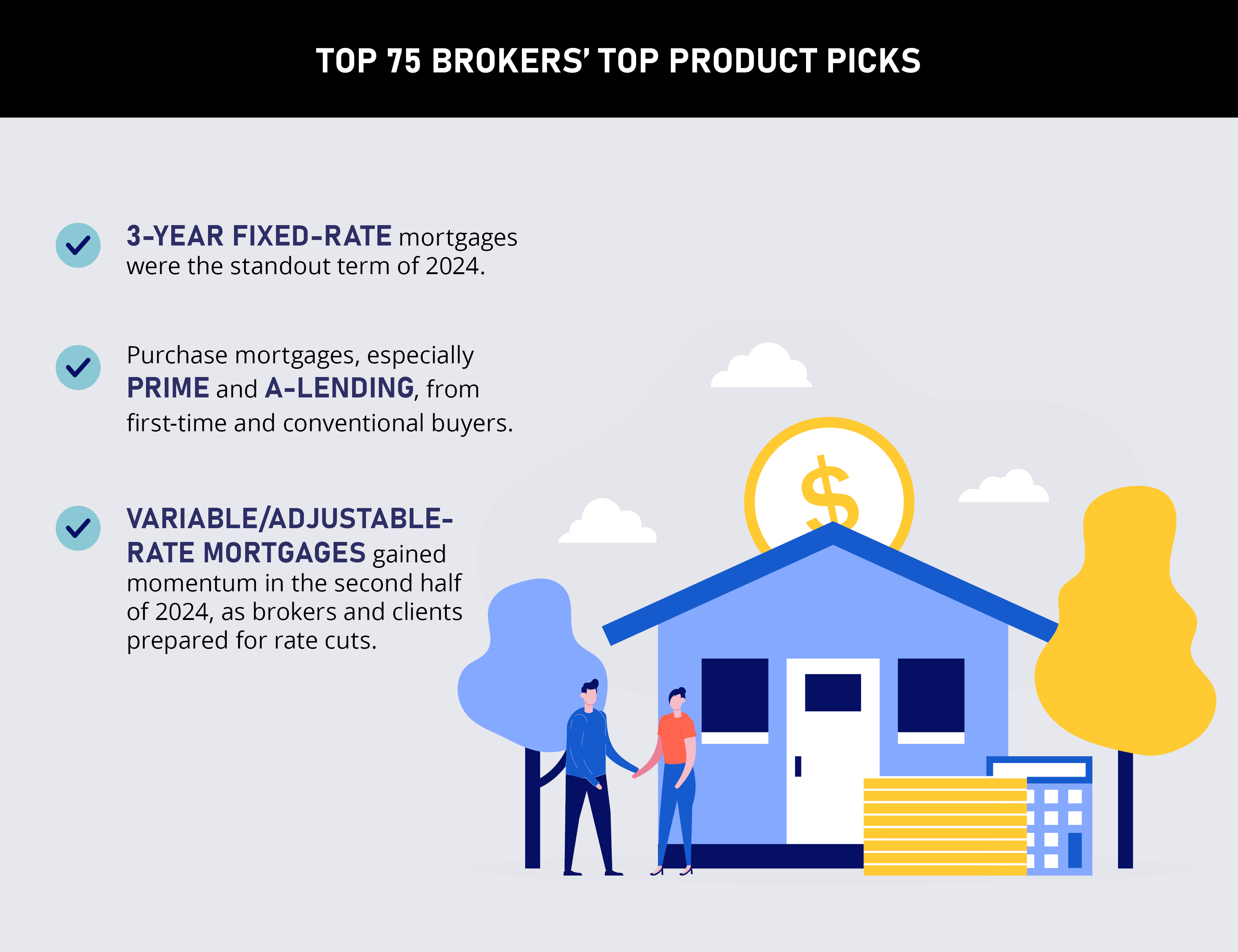

Affordability and supply issues for first-time buyers: With housing costs high and supply limited, many young Canadians are renting longer and waiting for rates and prices to fall before entering the market.

Refinances have become the main and most complex focus: Brokers are managing falling rates and borrower uncertainty around fixed vs. variable options, all while dealing with lower volumes and tougher lending conditions.

Brokers are stepping in where banks won’t: With banks declining more deals, especially on overpriced, delayed condo projects, brokers are increasingly sourcing private funds to help clients close or qualify in a tightening market.

“The top brokers have an extensive client list that they tap into with emails, social media, direct marketing, texts, and phone calls,” adds Strong. “They touch base regularly with clients who trust them to navigate this difficult market.”

That level of outreach became even more important as borrower priorities shifted. Clients also wanted help managing debt, weighing refinance options, and understanding how today’s decisions could shape their long-term plans.

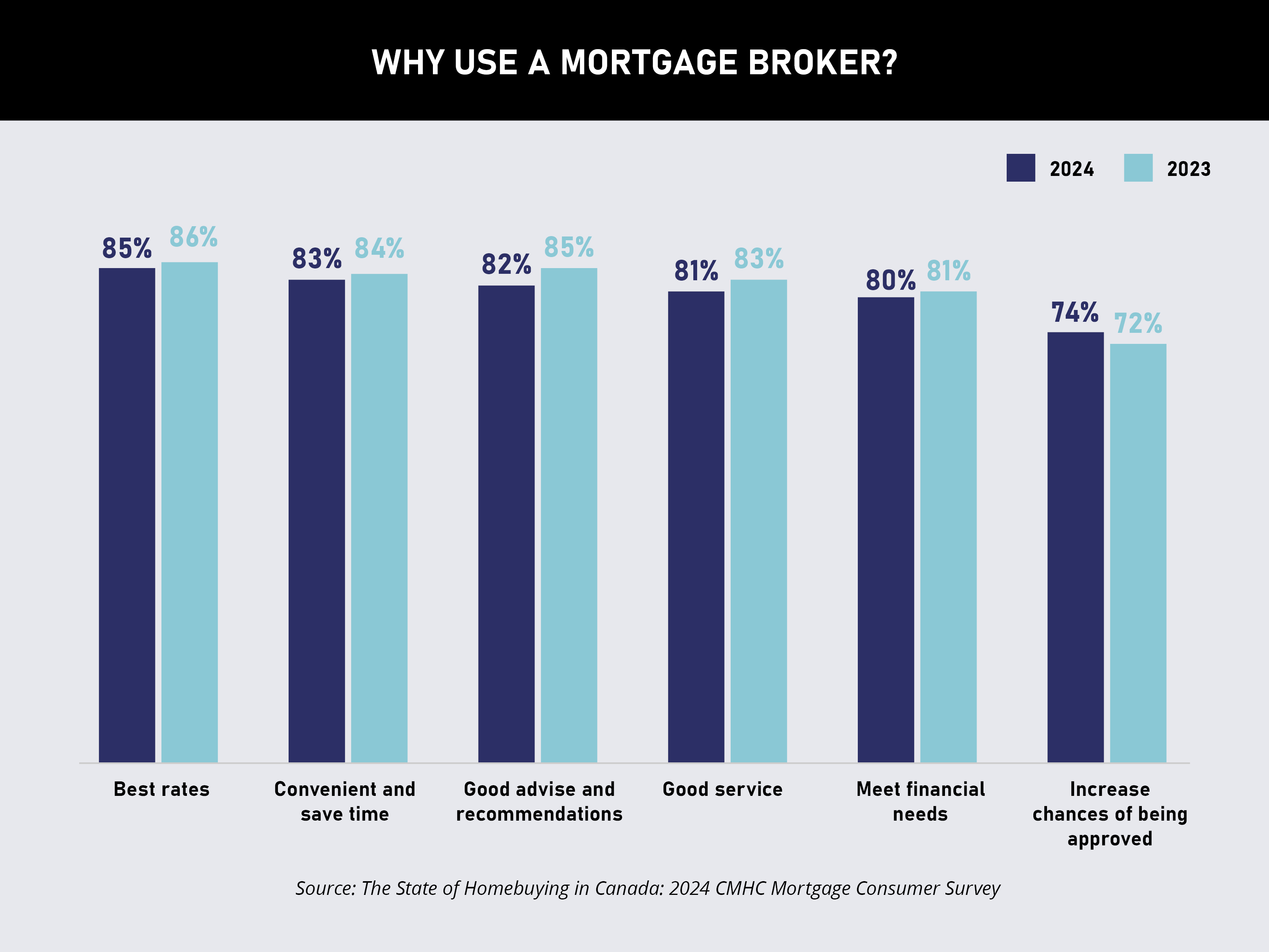

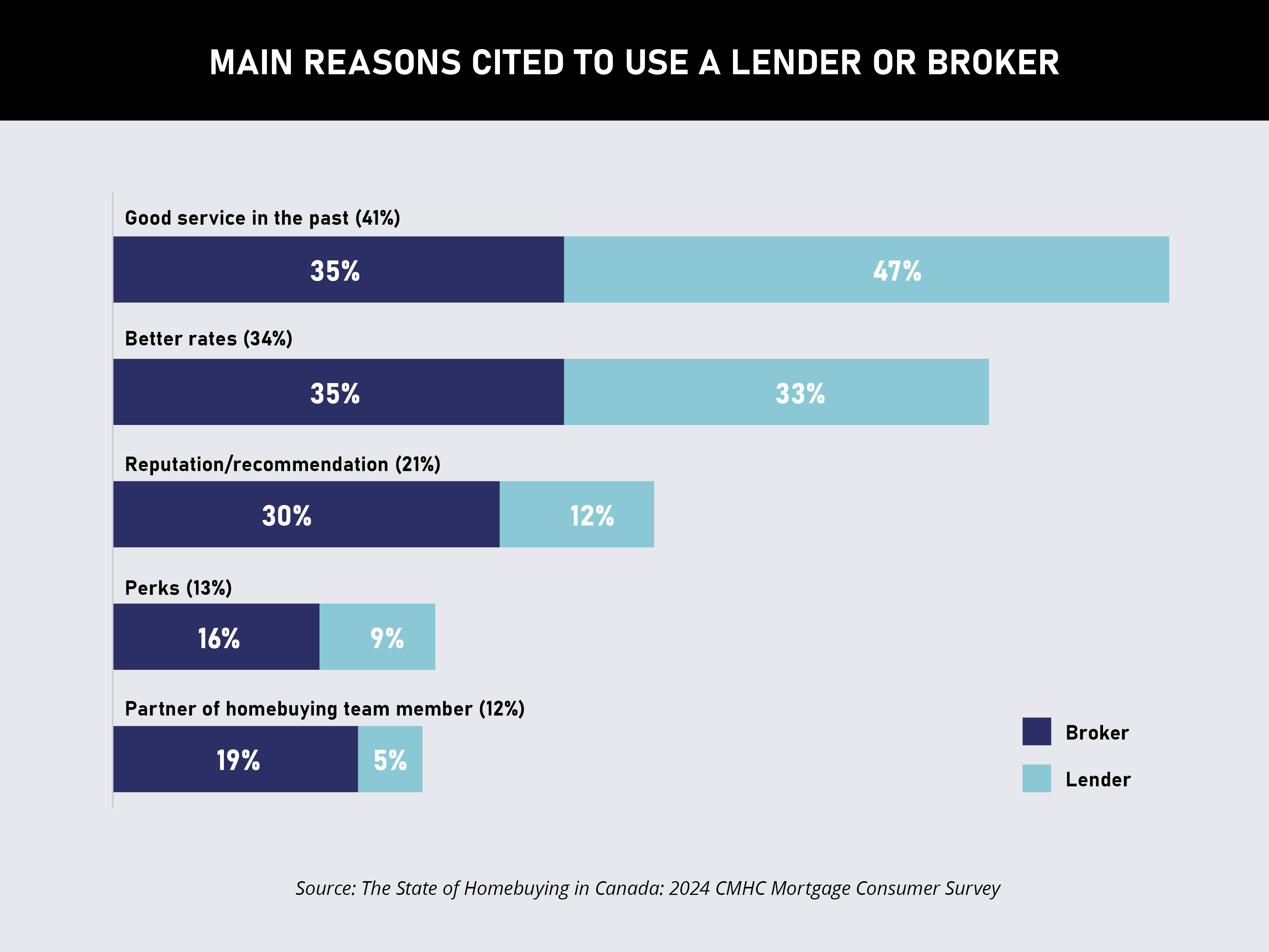

In fact, the broader mortgage sector reflected those changing expectations in real time. According to the 2024 CMHC Mortgage Consumer Survey, nearly half of all borrowers (48 percent) chose to work with a mortgage broker, up from 43 percent the year before.

That uptick in broker usage points to changing borrower expectations. A growing number of Canadians sought out brokers not only for better rates but also for strategic guidance, access to multiple lenders, and a more personalized approach.

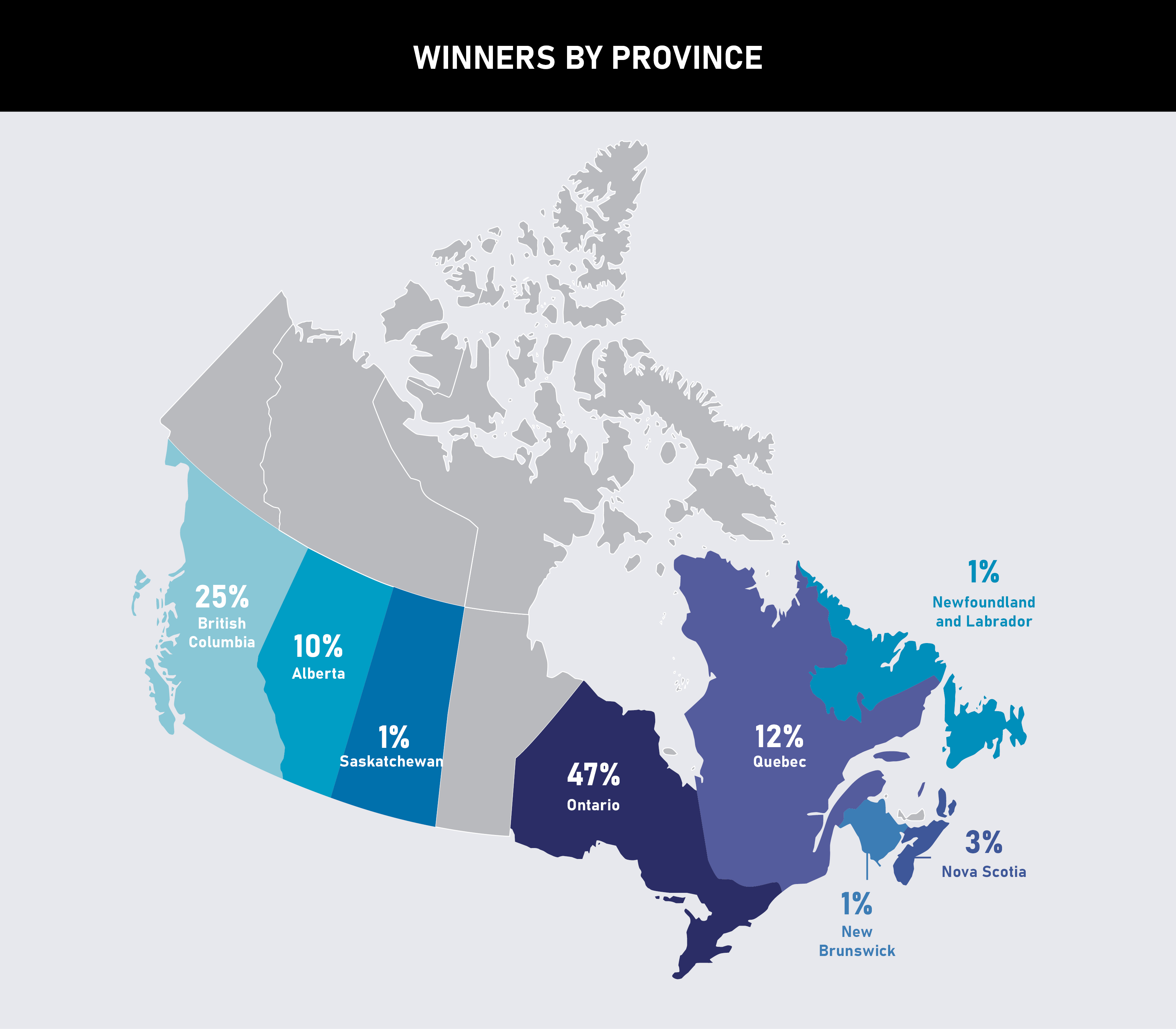

That marked the first time since 2019 that brokers were on nearly equal footing with traditional lenders. The jump was most pronounced among first-time buyers, refinancers, newcomers, and clients in Ontario, Quebec, and British Columbia, a demographic mix that often arrives with more questions and higher stakes.

As borrower needs become more diverse and complex, brokers are stepping up with tailored guidance and quick, informed responses.

“There are three traits that stand out when describing a top-performing broker: adaptability, knowledge, and client centricity,” says Akiff Kanji, business development manager at Community Trust. “They stay informed, communicate early, and prioritize the client experience at every stage. Their reputation is built not just on volume, but on trust and repeat business.”

Kanji added that the last 18 months have been marked by interest rate volatility, inflationary pressures, and political influences that have created more uncertainty in the market. “Brokers are facing more challenges that require more hands-on support on each file,” he says.

Meanwhile, brokers faced rising pressure on multiple fronts. Clients expected more options: on average, brokers presented 2.6 offers per buyer, a notable jump from 2.4 in 2023.

Anxiety around mortgage renewals surged, with 76 percent of borrowers bracing for payment increases as record-low rates from 2019 to 2021 began to expire. Regulatory changes, tighter underwriting, and intensified competition from banks added to the squeeze.

Brokers who continued to grow paid close attention to these needs. They adjusted their focus, strengthened their systems, and found ways to add more value during a time when clients needed it most. And that effort translated into results.

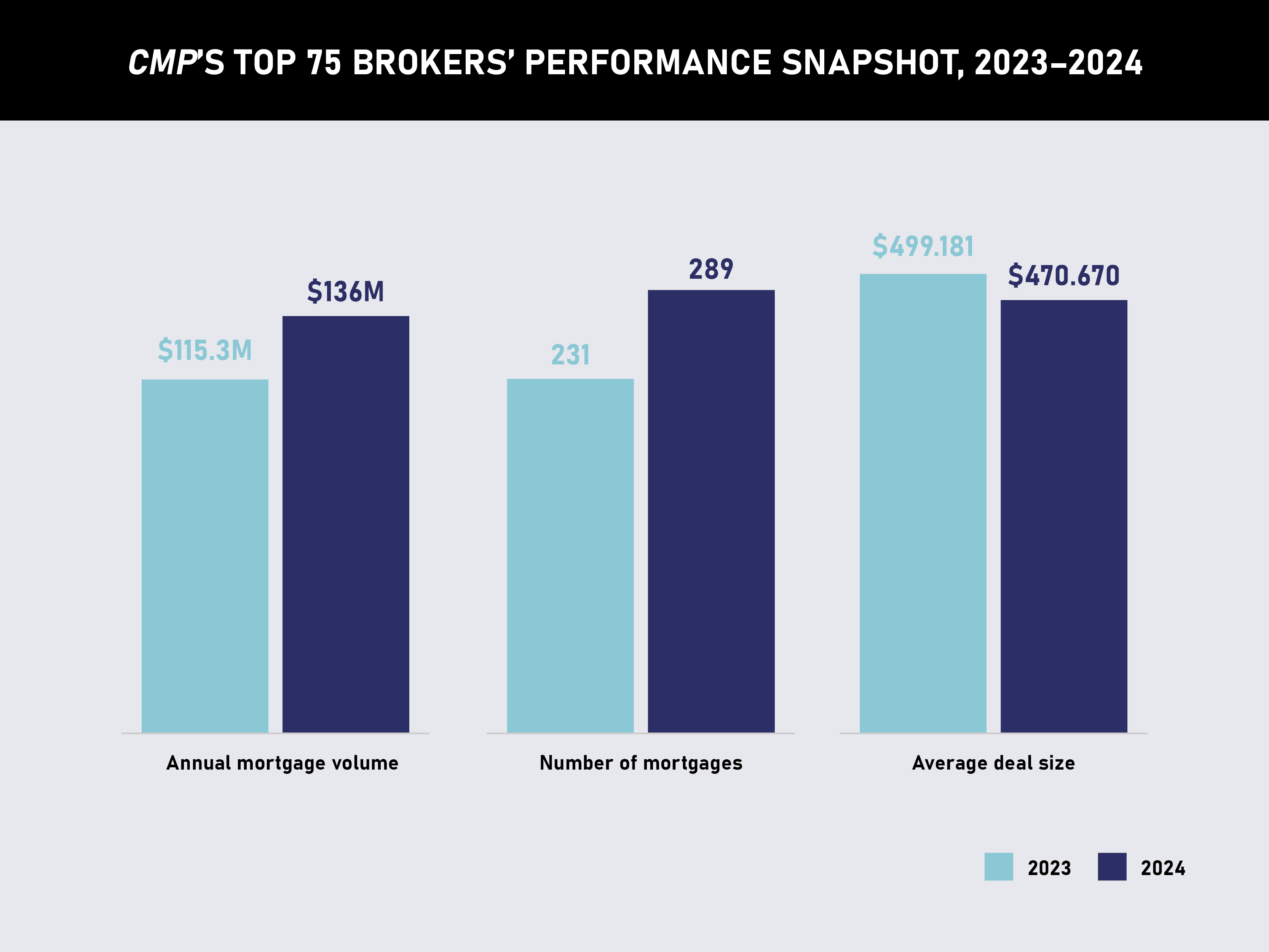

CMP’s 2023–2024 performance data reveal top brokers increased their average funded volume by 18 percent year over year and wrote 25 percent more mortgages compared to the previous year, a clear sign of robust pipelines and effective client retention.

Although average deal size edged down slightly, the overall lift in activity points to well-managed pipelines, data-driven systems, and a more intentional approach to client service.

This year’s Top 75 Brokers list was built on verified 2024 volumes, with all deals personally initiated by the nominees and focused on residential mortgages. To qualify, brokers had to be licensed and active in 2024, with final figures confirmed by lenders, aggregators, or franchisors.

CMP also recognized standout performers in smaller markets, where average home prices fell below $657,145, through the Top 20 Small Market Brokers list, highlighting those who pushed volume boundaries despite tighter conditions.

Despite working in different regions and markets, 2025’s best mortgage brokers found common ground in five key areas:

Client retention and service: Many brokers kept things simple: stay in touch, follow up, and actually listen. Annual check-ins turned into opportunities. Clients appreciated the attention, and brokers say that trust, built one conversation at a time, was what kept business coming in.

Referral partnerships: A lot of brokers said their strongest leads still came from the people they knew best. That meant keeping close ties with realtors, planners, and other key contacts. For some, it was regular updates; for others, client events or just being the person who always picks up the phone.

Database and CRM use: Some brokers took a hard look at the tools they already had. A well-maintained CRM, used properly, helped them spot renewal opportunities and reach clients before anyone else. A few mentioned using text, email, and even mailers to stay visible without being pushy.

Adapting to the market: With traditional approvals getting tougher, brokers who could offer alternatives, such as private, non-bank, and creative structuring, found themselves busier than expected. Being flexible helped them keep deals alive and gave clients options they didn’t know they had.

Visibility and marketing: Some went all-in on content. They hosted webinars and podcasts, posted educational videos, and built up their online reviews. Others focused on SEO or ran targeted campaigns. They focused on being present where clients were already looking for answers.

Industry veteran Strong underscores that top-performing brokers drive volume, possess market knowledge, and offer high-quality advice. “The top brokers are well acquainted with their local real estate and economic conditions in their markets,” he says. “They also have a keen eye on the economic news and Bank of Canada announcements that will affect present and future client outcomes and react accordingly.”

The brokers on CMP’s Top 75 list for 2025 stood out by adapting early, staying close to their clients, and putting thought behind every interaction. Success didn’t come easily last year. Those who moved forward did so with focus, flexibility, and a strong understanding of what their clients wanted to accomplish.

With Canada’s employment landscape expected to shift over the next three years, particularly in finance and housing-related sectors, brokers who stay nimble will be well-placed to lead. The brokers on this year’s Top 75 list are already a step ahead.

Danny Ibrahim

Principal Broker and CEO,

KeyRate Mortgage

No. 6 – CMP’s Top 75 Brokers 2025

Danny Ibrahim takes a straightforward approach to success, showing up each day ready to offer sound advice, follow through on his promises, and keep his clients’ needs front and centre.

“The key reason behind my success over the past 12 months has been consistency in client service and the ability to adapt quickly to changing market conditions,” he says. “While interest rates and lending guidelines fluctuated, I stayed ahead by proactively educating my clients, offering clear strategies, and maintaining strong relationships with lenders.”

He credits that duo of preparation and flexibility with helping him stay one step ahead in an unpredictable market. Behind the scenes, he also prioritized simplifying how his team works, bringing in new tools to speed up the process while ensuring clients still felt supported.

Ibrahim’s approach to attracting clients fuses digital outreach with the trust that comes from consistently doing good work. “I use a combination of relationship-building, digital marketing, and value-driven education to attract clients,” he says. “That starts with delivering consistently excellent service. Clients who feel supported often become your best promoters.”

He also invests time in social media, blog content, and short videos that demystify the mortgage process and explain market trends. “This positions me as a knowledgeable, approachable expert,” he says.

But Ibrahim doesn’t stop online. He frequently attends local networking events and builds referral relationships with real estate agents, financial advisors, and community groups. “Ultimately, it’s about being visible, reliable, and genuinely helpful. People are drawn to professionals who provide real value, not just a sales pitch,” he adds.

For Ibrahim, the deal may close, but the relationship doesn’t. “My approach to retaining clients is built on consistent communication, trust, and ongoing value,” he remarks. “I see that as the beginning of a long-term partnership.”

He keeps in regular contact, shares timely updates, and checks in proactively. “Whether through annual reviews, follow-up calls, or thoughtful gestures such as holiday greetings or milestone recognitions, I make sure clients know they are not regarded as a transaction and that they are valued,” he notes.

That commitment to personalization is central to how he works. “People stay loyal when they feel heard, supported, and prioritized, and that’s exactly what I strive to deliver,” Ibrahim says.

Ibrahim believes the key to client satisfaction is understanding what they need, communicating clearly, and following through. “I start by listening closely to what the client truly needs, whether that’s a competitive rate, a fast turnaround, or extra support for a first-time buyer,” he says. “I prioritize transparency and keep clients informed every step of the way, so they’re never left in the dark.”

But what matters most, he adds, is delivering on your word. “What I say I’ll do gets done. Satisfaction doesn’t just come from closing a deal; it comes from the client feeling respected, supported, and confident that they made the right choice working with me,” says Ibhrahim.

Ibrahim is targeting smart growth, not just more deals but better ones that are handled more efficiently. “My main focus is integrating generative AI into our software systems to make our operations run more smoothly, improve the client experience, and help us grow more efficiently,” he says.

“This next phase involves automation, but it’s about building a smarter, more responsive workflow that gives clients and our team real-time insights and personalized solutions.”

And even as he pushes the limits of technology, Ibrahim is grounded in what got him this far. “By combining cutting-edge technology with the same personalized service that built my foundation, I’m aiming to increase volume, improve turnaround times, and offer a best-in-class experience that sets me apart in a competitive market,” he says.

Ryan La Haye

President and mortgage broker,

Group RLH – Planiprêt

No. 13 – CMP’s Top 75 Brokers 2025

(Small Market)

In a year of uncertainty, Ryan La Haye has sailed through the turbulence with conviction. A familiar name among Canada’s best mortgage brokers, he has ranked among the Top 75 for the past eight years in the small market broker category. He has taken an unorthodox, strategy-first approach to scaling his business, challenging industry conventions and pushing the boundaries of delivering exceptional value to clients.

In 2024, La Haye made that leap and moved decisively toward depth over breadth. “It’s pretty straightforward,” he explains. “For the last five years, we’ve been slowly moving our business away from rate-based sales and toward deep strategies.”

La Haye runs a major national organization, Smith Manoeuvre Services Corporation (SMSC), focused exclusively on mortgage strategy accreditations and trains brokers who want to scale their business.

SMSC strategies allow homeowners to convert their mortgage interest into tax-deductible investment loan interest, allowing for savings and optimization. “We’re getting some traction now after marketing it for many years,” he says. “We’ve mastered how we need to position ourselves to get the word out to Canadians on how these strategies can impact their finances, and certainly their retirement.”

That mindset shift came with bold operational decisions when the brokerage changed course last year and stopped doing renewals. Instead, La Haye’s team uses those moments to engage clients in a deeper conversation about various strategies that may benefit them financially.

His firm also implemented a consultation fee to ensure clients are genuinely committed. “If clients are uncomfortable, they might refuse that fee at the onset, then it’s clear they’re not committed to working with us,” he notes. “We realized that clients are willing to actually front money to meet us, which allowed us to be more efficient and scale.”

La Haye believes brokers should shape their business around the services they want to provide, then focus on finding clients looking for that kind of support.

As consumer anxieties grow in an unpredictable market, La Haye sees client expectations evolving in kind. “Canadians are increasingly concerned with their financial future and the market’s viability,” he says. “We want to be stepping into that space and making people realize that debt management is extremely important. You could vastly create more wealth by making your debt more efficient.”

In his view, many brokers have missed the opportunity to position debt strategy as a pillar of financial planning, something his team has capitalized on with strong client engagement and retention.

On the systems side, La Haye makes no bones about what’s necessary for brokers today. “Obviously, you must have integrated AI into your business,” he remarks, emphasizing that AI is not a replacement for expertise but a game-changer when used strategically.

“Imagine you have a staff of researchers sitting around a table; this is what AI brings to our business,” he notes. “But don’t stop thinking. Use it to help you accelerate the positive things that you’re doing. Don’t use it as a replacement for cognitive thought.”

La Haye’s advice is blunt but powerful for brokers aiming to break through volume plateaus and earn their place among Canada’s top performers. “To be able to drive volume, you need to have impact. And that’s not about you; it’s about making a difference for others,” he explains. “That starts with reimagining client outcomes, and if the answer is ‘I got them a great mortgage product,’ then that doesn’t mean having an impact.”

“You have to be obsessed, not only about driving the business, but about being creative in marketing and client engagement,” he remarks about the importance of a strong work ethic.

And for those who think they can sidestep the grind, La Haye says to think again. “If you’re thinking you’re going to work 30 hours a week and get onto the Top 75 Brokers’ list, where brokers have invested hundreds of hours a month, it’s not going to happen.”

La Haye doesn’t mince words when asked what lies ahead in 2025 and beyond. He sees plenty of upside, especially in automation. From social media campaigns and podcasting to mortgage application submissions, brokers now have more tools than ever to streamline the routine and scale their reach.

But the bigger play, he believes, is in specialization. As the easier parts of the job become increasingly automated, brokers who stick to straightforward purchases or renewals could find themselves outpaced.

His warning is unequivocal: brokers who fail to evolve into trusted advisors offering more tailored, human-driven guidance will be left behind. “It sounds grim,” La Haye admits. “But the truth is, there’s more opportunity than ever for the brokers willing to go deeper.”

Joanna Zhou

Mortgage broker,

TMG The Mortgage Group

No. 33 – CMP’s Top 75 Brokers 2025

As a broker working exclusively with real estate investors, Joanna Zhou adapted to the changing landscape and tripled her volume by anticipating what her clients would need next and getting ahead of the lending curve.

“The most important thing to realize is the market is always changing,” she explains. “And we need to work with clients to understand their financing requirements.”

A few years ago, her investor clients mainly refinanced and bought more rental properties. However, with residential opportunities tightening and condo markets cooling, Zhou didn’t wait for things to bounce back; she looked for the next opportunity.

“I succeeded even in a tougher market because I switched to a new financing program from CMHC for real estate investors to purchase with a commercial mortgage instead of a residential mortgage,” she says. “And then I grew my business alongside my clients.”

Zhou has built her niche by offering investor clients a roadmap to scale their portfolios without hitting financial walls. “When I first got my clients, I started exploring how they could grow their portfolio without hitting a financial wall,” she says. “I found that residential mortgage guidelines were more stringent, with more regulations, and from there I started to explore commercial mortgages for those investors.”

Specialized brokers who understand nuanced borrower profiles, such as self-employed clients, are in high demand.

Kanji says, “Self-employed borrowers are an enormous part of any alternative lender and represent a segment that requires a deep understanding of the business, including the ins and outs of the bank statements, source of income, seasonality within the industry, and more. As entrepreneurship becomes more prominent in Canada, brokers who can serve them will stand out.”

Zhou’s pivot required significant investment in her own development. She started learning everything she could about commercial mortgages, studied, and attended events to connect with lenders.

Zhou sees education as a two-way street, staying informed while ensuring her clients are ready to seize opportunities when they arise. “Always prioritize learning new things, looking at the market, understanding your clients, where they’re going, and the financing choices,” she adds.

When asked about the routines fueling her performance, Zhou quickly pointed out that learning isn’t optional but built into her mindset.

“I always push myself to perform at the highest level. I always find a good role model,” she explains. “I attended commercial real estate forums, got to know people, learned who the top players were, and tried to form a relationship.”

Zhou entered the mortgage space in 2018 and dove into education immediately, with webinars, training sessions, and strategic networking with top brokers and lenders. That early effort gave her the confidence and capability to specialize in a new market.

For brokers looking to grow in today’s market, Zhou’s advice is not to cling to what used to work.

“The market shifts constantly,” she reflects. “Right now, we have a good program for financing commercial mortgages. I did residential mortgages for the first three years in this business, but about 80 percent of my volume in the last three years came from commercial. Markets go up and down; we need to keep in touch with clients and find opportunities.”

She sees the ability to identify financing trends early and build relationships with the right lenders as a major differentiator. “It’s not about finding the cheapest rates, but the best solutions for our clients,” Zhou says.

For 2025, Zhou’s biggest opportunity and vulnerability both revolve around financing programs and government policy. “My success is due to good programs in the market,” she says. “What happens if the programs shut down or are funded less?”

Zhou is already broadening her options and exploring conventional commercial mortgages other than the CMHC program to protect her business. She’s also keeping a close eye on lending policies. “Always keep your client base as broad as possible; don’t focus on just one program,” she notes.

Walid Mutahar

Team lead – Mortgage agent,

Get A Better Mortgage

No. 75 – CMP’s Top 75 Brokers 2025

Walid Mutahar stayed focused, steady, and grounded in the basics, building success in a high-pressure, rate-sensitive market through consistent communication and careful attention to detail.

“There’s no kidding that last year wasn’t easy for anybody,” he says. “We really leaned into communications, ensuring our clients knew they had our support and making sure our referral partners knew we supported them.”

Kanji agrees with that approach, noting, “A leading broker should aim for a 24- to 48-hour response time for inquiries and a clear, step-by-step communication plan once a file is in motion. A top broker will always set clear expectations, follow up proactively, and keep clients informed. Acknowledging a question and advising that it is being worked on makes a big difference in the client experience.”

Mutahar and his team backed up their outreach with action. They introduced targeted promotions for key referral partners and made sure strong performance didn’t go unnoticed. “If it worked out, we rewarded them accordingly,” he says.

Mutahar points to clean, well-managed data as a key performance driver on the operations side. By maintaining a meticulous CRM, his team can identify opportunities and re-engage clients, especially during slower periods.

Mutahar focuses on addressing clients’ current needs while helping them plan for key decisions such as renewals.

“Everybody is dealing with increased inflation and higher prices on day-to-day living,” he reflects. “Whatever we can do for the bulk of our clients to minimize the payment shock, the interest shock, whether that’s consolidating debts or refinancing, extending amortizations, we always keep their future goals in mind.”

That forward planning happens well before renewal time. “We show them what that will look like in the future as of today,” Mutahar explains. “Help set the expectations and how we can prepare and get them to their goals, ultimately.”

When asked about the habits and systems that keep him operating at a high level, Mutahar pointed back to his tools and training. “Our CRM is the biggest tool. We can generate reports and identify opportunities to serve clients better, such as getting them lower rates. That’s number one,” he says.

Strong agrees that for brokers with the right systems and qualified clients, speed is an expectation. “With the latest technology and established, reliable income, good credit client(s), approval can be done in minutes,” he says. “If the client has poor credit, not enough income, and other factors and cannot qualify at a regular bank, the process could be the next day.”

The second element is knowing the math cold. “Leaning on other technologies to calculate penalties from a mortgage statement and having that information readily available is huge,” he says. “It helps you identify opportunities and understand the costs so that you can give clients better advice on the back end.”

Mutahar’s roots are in retail banking, where he got his start before becoming a mortgage broker in 2018, which still pays dividends. He says, “More than anything, it helps with my customer service and ability to speak to clients.”

Mutahar knows exactly what helped him get ahead and what can support others on the same path. “If you’re a brand-new agent, I believe joining a team, where you have files to work on and the support to get those files to the finish line, is instrumental to growth,” he notes. “Without it, I wouldn’t be where I am today.”

He suggests that more experienced brokers be super organized regarding their database. “It actually works – having the information always available to you. When times are slow, you can dig in, find those opportunities, and save your clients some money, and they’ll be appreciative,” he adds. “Then who knows what comes of that – another referral, maybe a realtor notices all the extra work you’re doing, and so on.”

Mutahar sees a prime opening and a familiar threat as the market evolves. “The biggest opportunity will be renewals, refinances, and debt consolidations. 2020 and 2021 were busy years, and we’re approaching a gold mine of renewals. You’re not going to win them all, but there are opportunities there,” he remarks.

At the same time, many Canadians are carrying high debt loads. That makes proactive outreach essential, such as checking in, understanding clients’ situations, and offering thoughtful solutions.

“The biggest risk is going to be competition, as it always is,” he says. “But you have to find ways to differentiate yourself. If you’re an order taker and make the process transactional, it will be very difficult to get new business and retain the clients you’ve helped in the past.”

The nominations opened in January for CMP’s 2025 Top 75 Brokers. To be eligible, nominees must have been licensed and employed as brokers in 2024. All mortgage deals and volumes had to be personally initiated and could only include residential-based mortgage deals. Overall funded volumes for 2024 that were verified by aggregators/franchisors/lenders formed the basis of the Top 75 selections.

In the Top 20 Small Market Brokers, CMP also showcased those who are breaking new volume barriers in markets where at least 80 percent of the broker’s business is from average home prices of $657,145 or under.