Jump to winners | Jump to methodology

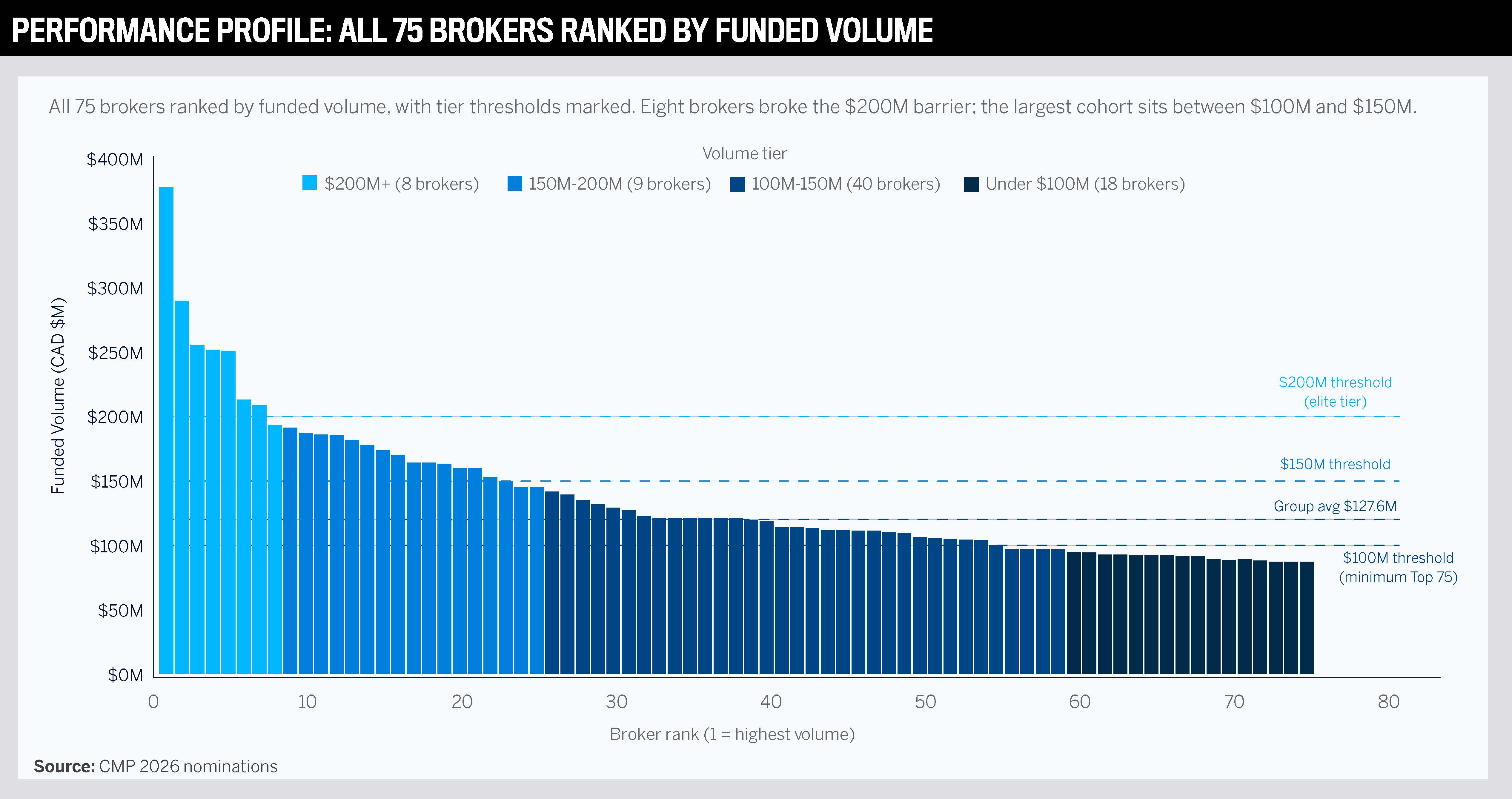

CMP identifies the best mortgage brokers in Canada for 2026: 75 professionals who moved more than $10 billion in a year of renewal pressure, bank competition, and

economic uncertainty

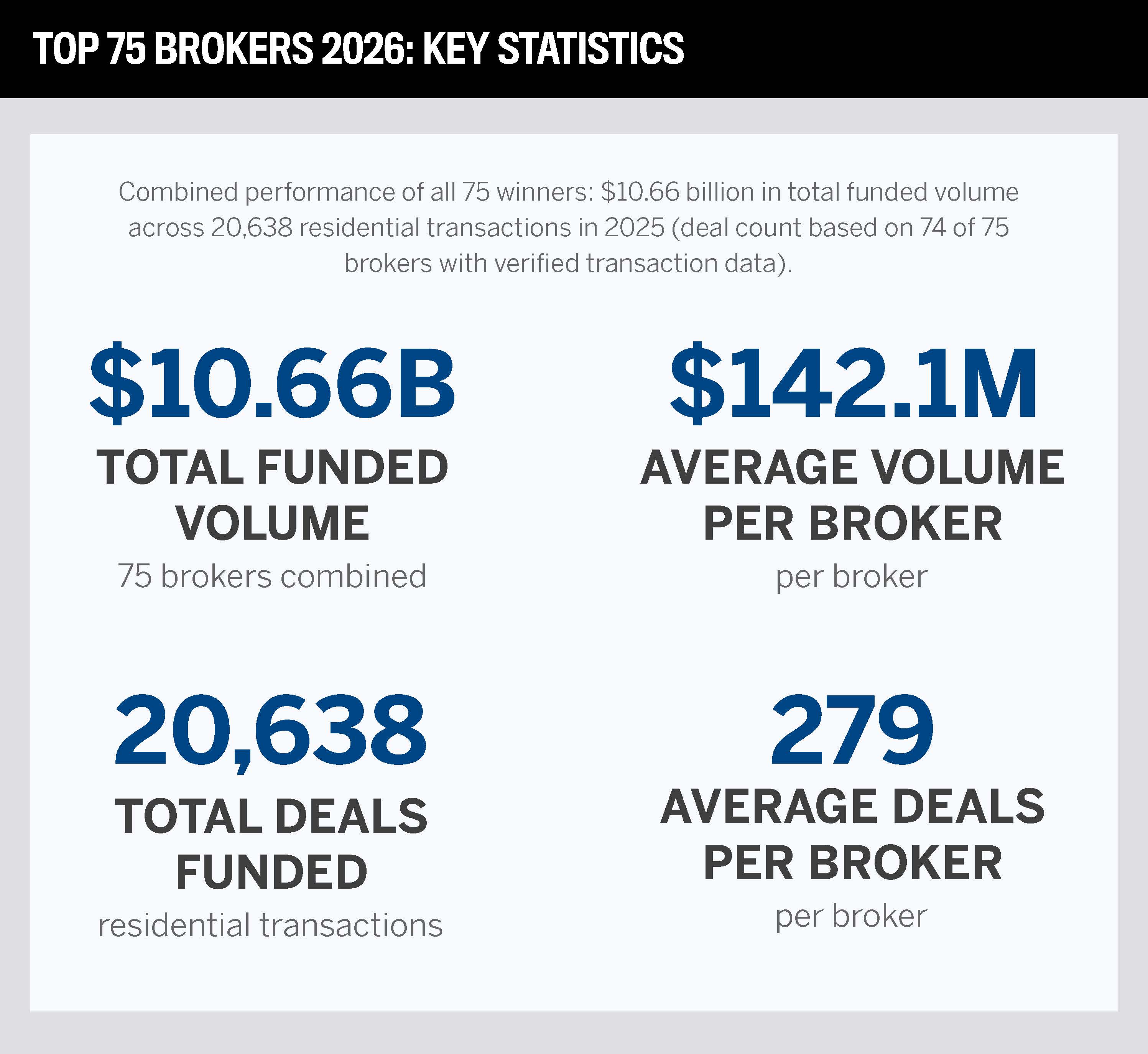

The numbers alone are staggering. Each year, Canadian Mortgage Professional identifies the best mortgage brokers in Canada through its Top 75 Brokers list – and the 2026 class is the strongest yet. These 75 professionals collectively funded more than $10.66 billion in residential mortgages in 2025, each volume verified by aggregators, franchisors, and lenders. But behind every figure is a story of relationships cultivated over years, systems built to survive market volatility, and a philosophy of advice-first service that has quietly been reshaping the relationship between Canadians and their mortgages.

The last 12 months have been easy to operate in. The Bank of Canada’s rate path created anxiety among borrowers. Banks competed aggressively to retain clients at renewal. The so-called renewal wave – a historic concentration of mortgages originated at pandemic-era lows now coming due at materially higher rates – generated financial stress for hundreds of thousands of Canadian households. And yet, within that turbulence, the brokers on this list grew.

To be eligible, nominees must have been licensed and employed as brokers throughout 2025. All mortgage deals had to be personally initiated, covering residential transactions only. Overall funded volumes were verified by aggregators, franchisors, and lenders. The Top 20 Small Market category recognizes brokers achieving exceptional volumes in markets where at least 80 percent of business derives from properties priced at $657,145 or below.

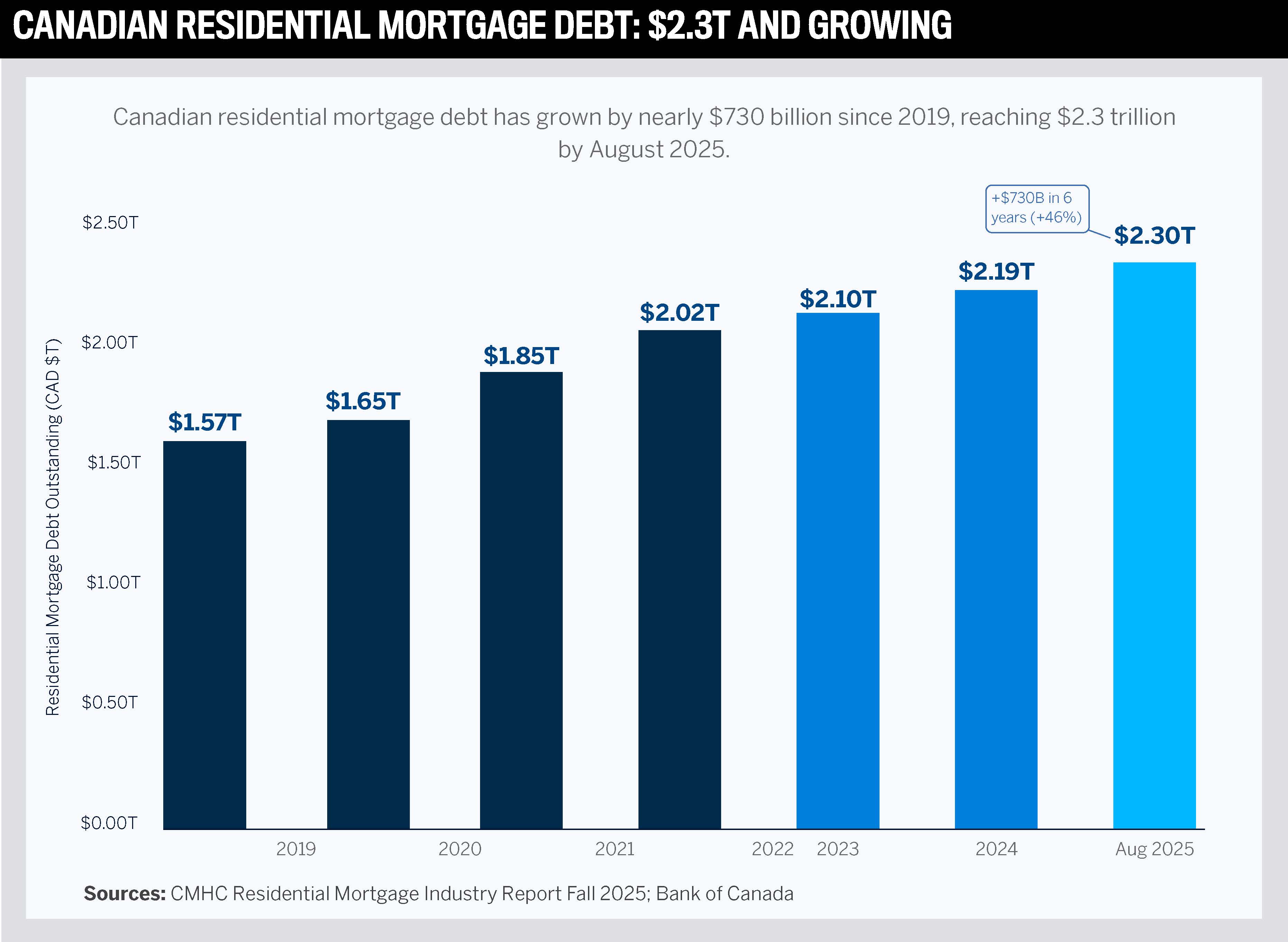

To appreciate what the best mortgage brokers in Canada achieved in 2025, it helps to understand the scale and dynamics of the market in which they competed. Canadian residential mortgage debt reached $2.3 trillion in August 2025 – up 4.8 percent year-on-year – in a market shaped by an extraordinary concentration of renewal activity, shifting rate preferences, and an evolving competitive landscape between banks and brokers.

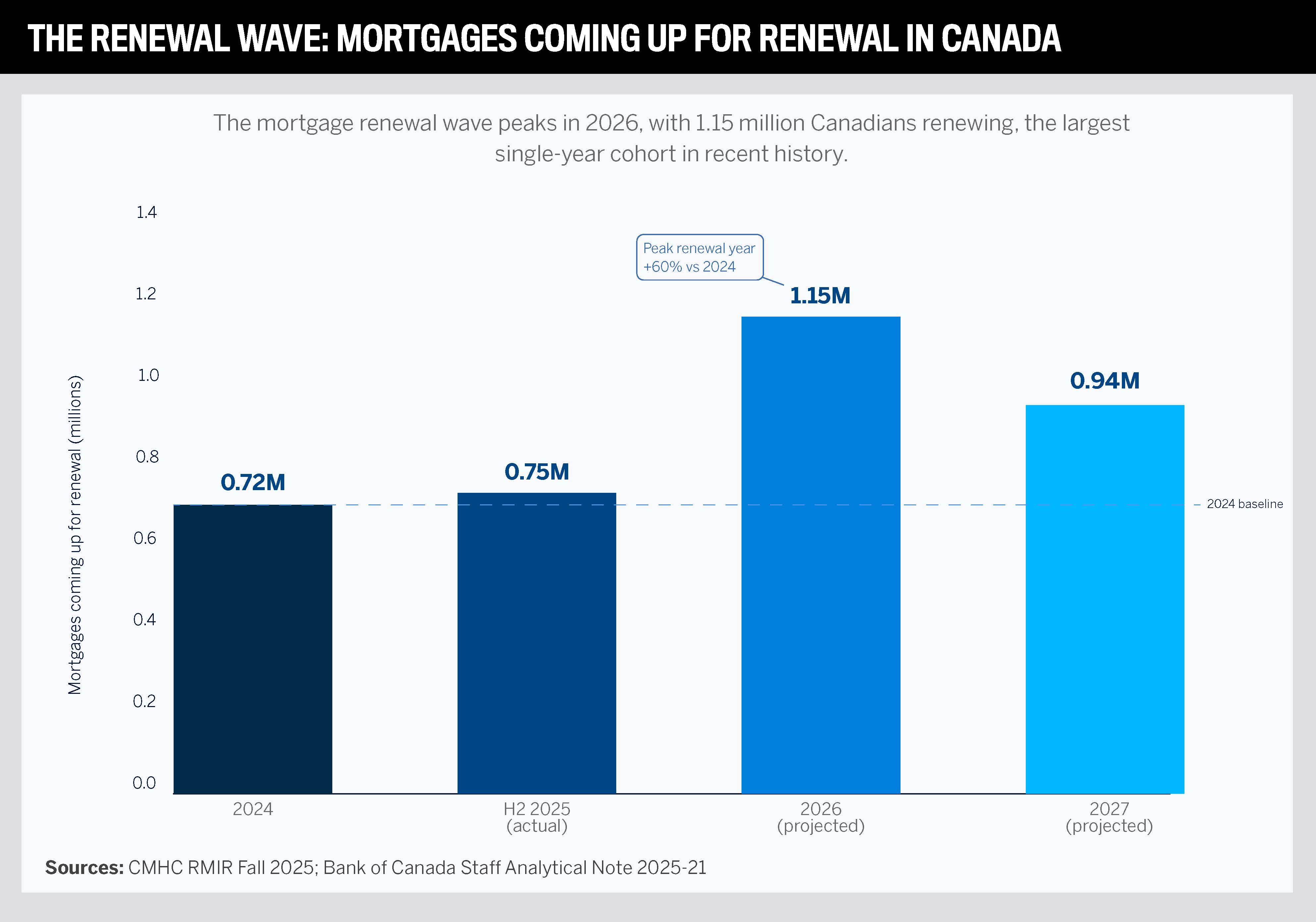

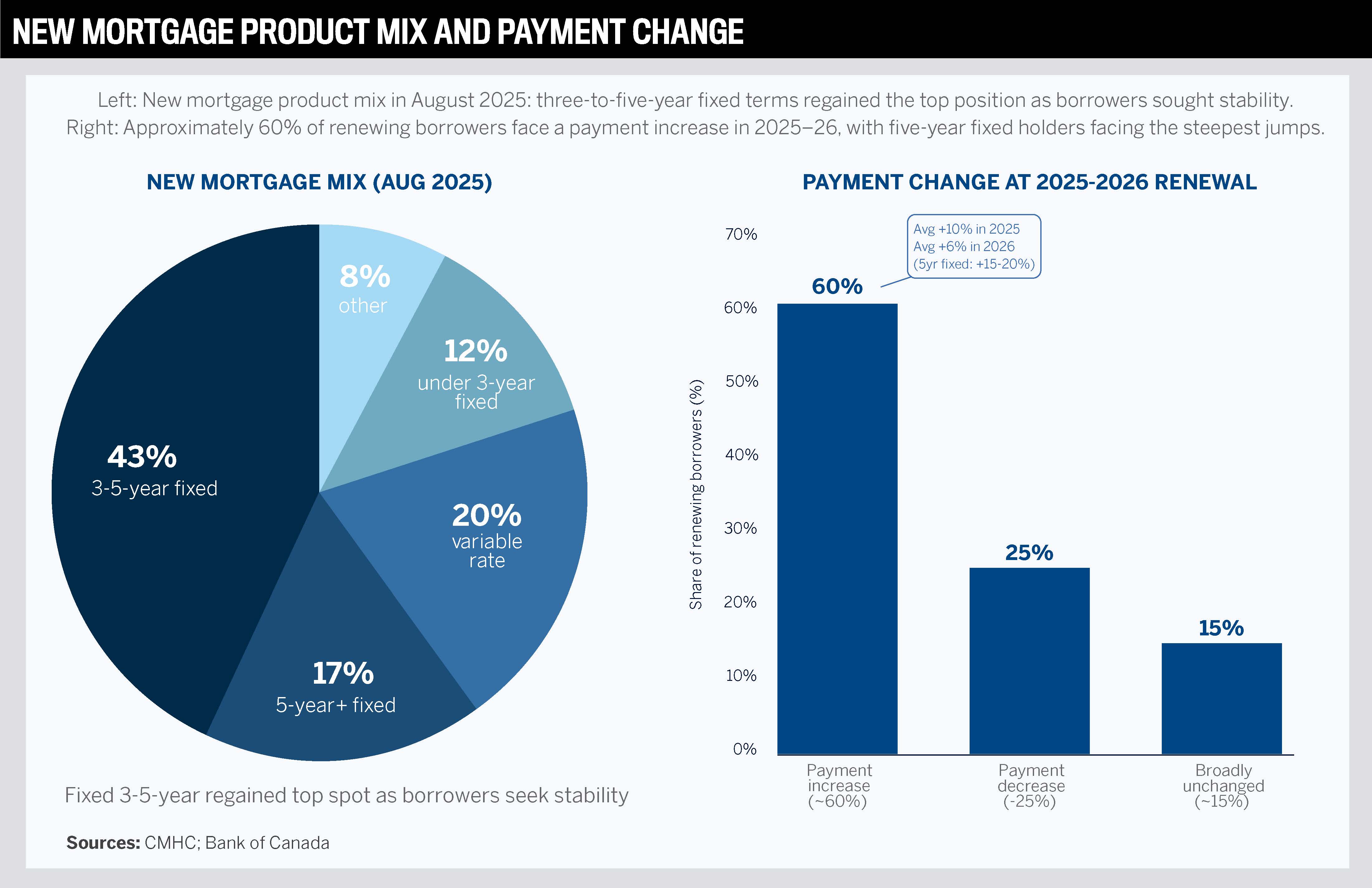

The single most consequential dynamic of 2025 and 2026 is the renewal wave. According to CMHC’s Fall 2025 Residential Mortgage Industry Report, over 750,000 mortgages came up for renewal in the second half of 2025 alone. That figure climbs to 1.15 million in 2026 — an increase of roughly 60 percent compared to 2024 — before easing to around 940,000 in 2027. These are borrowers who locked in at pandemic-era rates as low as 1–2 percent, and who now face terms in a materially higher-rate environment. According to Bank of Canada analysis, roughly 60 percent of those renewing in 2025 and 2026 will see their monthly payments increase – with five-year fixed-rate holders facing average increases of 15–20 percent, equivalent to approximately $5,100 more per year.

This is the environment in which the Top 75 brokers operate. For many of their clients, a mortgage renewal is not a routine administrative event but the most significant financial reassessment they will undertake in years. Anxiety is real, options are complex, and the need for expert advice is acute. That is precisely the terrain on which great brokers distinguish themselves.

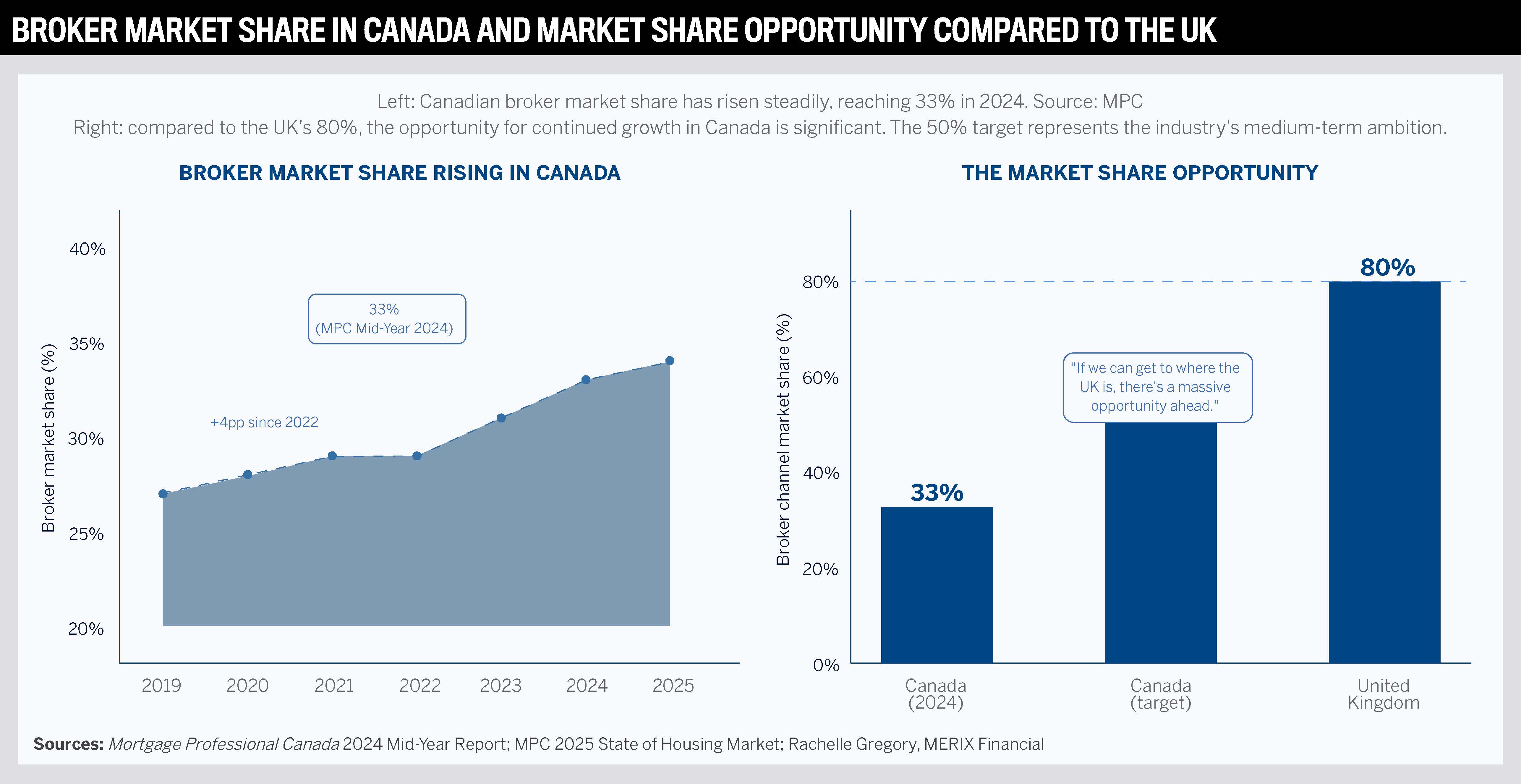

Against this backdrop, the broker channel has been growing its share of the Canadian mortgage market. Mortgage Professional Canada’s 2024 Mid-Year Report confirmed that brokers now hold a 33 percent market share – a four-percentage-point increase since the end of 2022 and a figure that underscores the structural shift underway in how Canadians obtain their mortgages.

“The best brokers are building around their ability to advise their customers; they’re not just order-takers, they build relationships and offer clear strategies,” says Rene Quercia, SVP of the broker channel at HomeEquity Bank. "They are great listeners, follow up regularly, and turn those check-ins into business opportunities."

The direction of travel is clear. The MPC’s 2025 State of the Housing Market report found that two-thirds of Canadians say they are likely to use a broker for their next mortgage. Yet, even at 33 percent, Canada remains far behind the UK, where brokers command approximately 80 percent of the market.

Chris Turcotte, president of Real Mortgage Associates, adds a landmark data point to this narrative: Dominion Lending Centres Group now funds more new mortgages in Canada than any bank, trust company, or credit union. That milestone, he argues, is not an endpoint but a demonstration of what the broker channel is capable of – and a signal of the momentum still to come.

Turcotte frames the defining challenge with characteristic directness. The two biggest headwinds of the past year and a half have been renewals and the banks’ determination to hold onto their existing clients. Brokers who win in this environment, he argues, do so not through superior technology but through superior process discipline.

“Banks are digging in and defending their existing clients. Brokers need to work hard to secure the business and find the solution that is truly going to help the client in their situation,” says Turcotte. “Luckily, that’s often not just a low renewal rate.”

He points to a telling example: the signing appointment. The best brokers record a seven-minute video walkthrough and send it alongside the signing package, so clients are fully informed before they open a single document. The average broker still books a one-hour signing call. Compounded across an entire year of clients, that difference in process efficiency is the difference between 8.5 signings and one, a ratio that tells you everything about how volume leaders build their edge.

Technology matters but what drives loyalty and repeat business is whether a broker can make the client feel understood. There's a belief that consumers stay loyal to brokers because of the human connection and an understanding of the entire landscape, more so than an efficient way of working.

Three markers of top performers are: selectivity in lender relationships (top brokers pick partners that match their business model rather than dealing with every lender in Canada); continuous engagement with the industry through events and education; and the ability to function as a trusted financial advisor rather than a transaction facilitator.

HomeEquity Bank is a specialist in reverse mortgages and notes that niches like this are crucial for broker success. Quercia says, “While banks can be rigid, brokers have options with alternative lenders that consider gross earnings, letting clients buy homes they can actually afford.” And he adds, “For example, brokers with a flexible toolkit that includes a reverse mortgage solution are better equipped to grab a bigger market share, particularly within the 55+ demographic.”

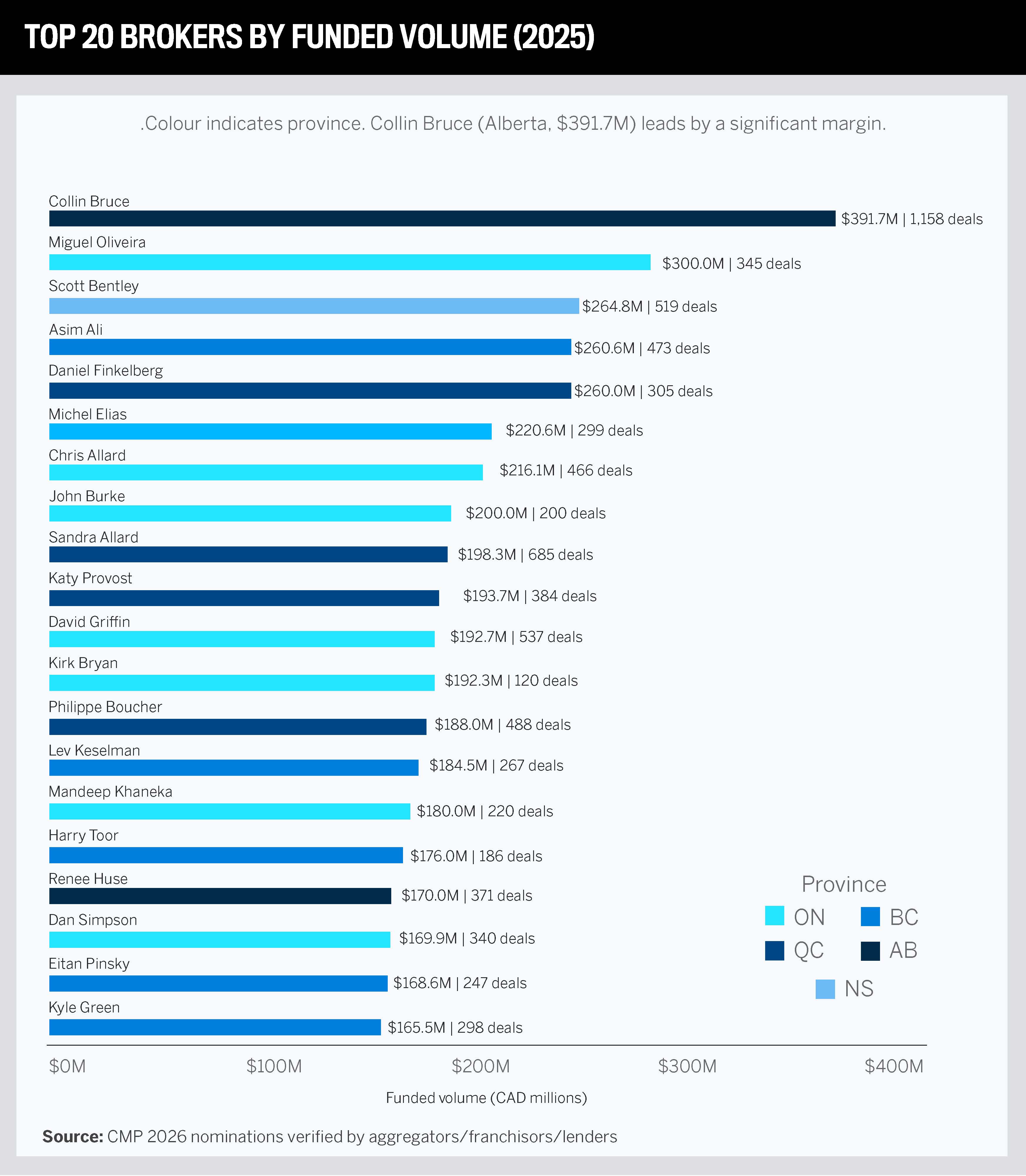

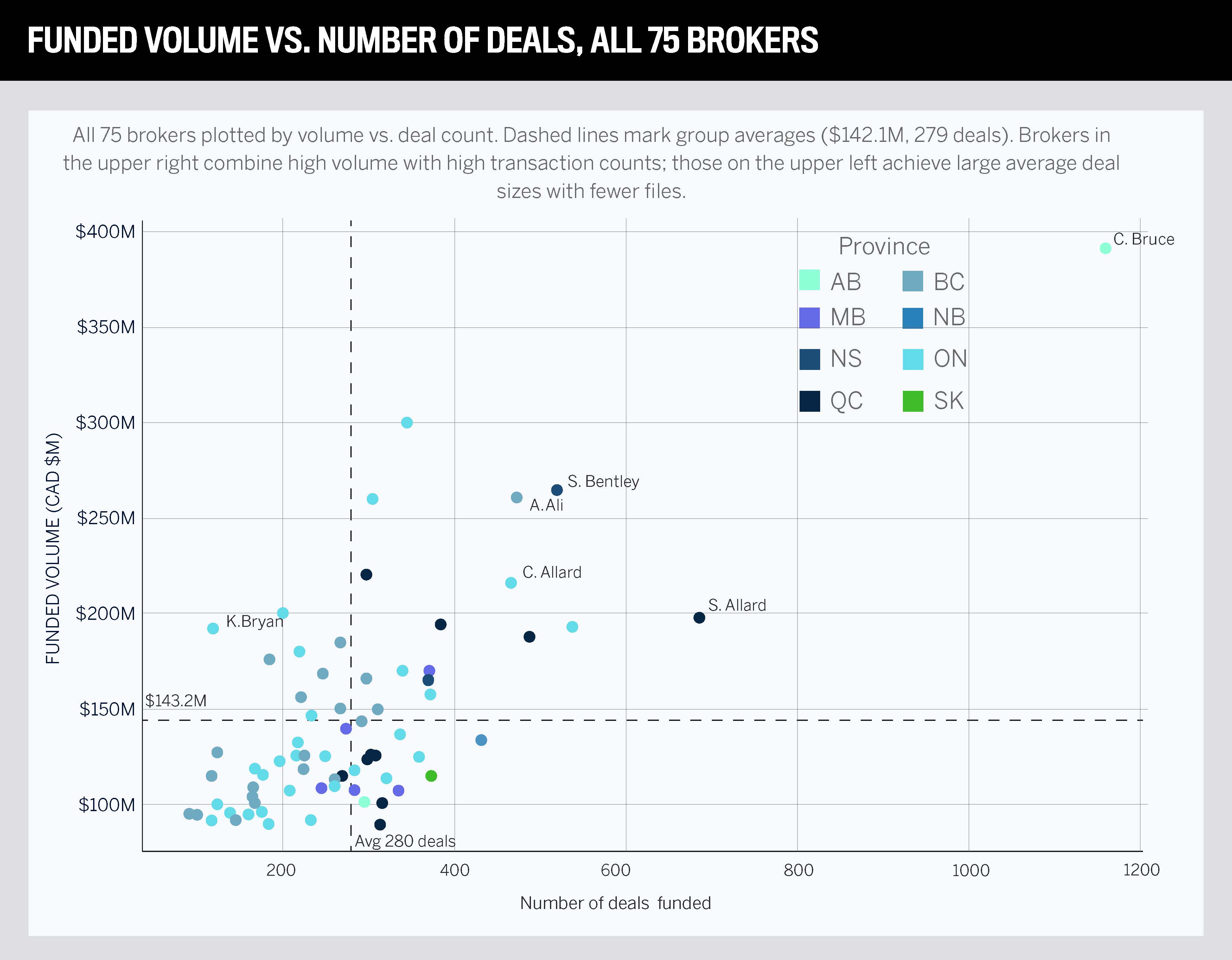

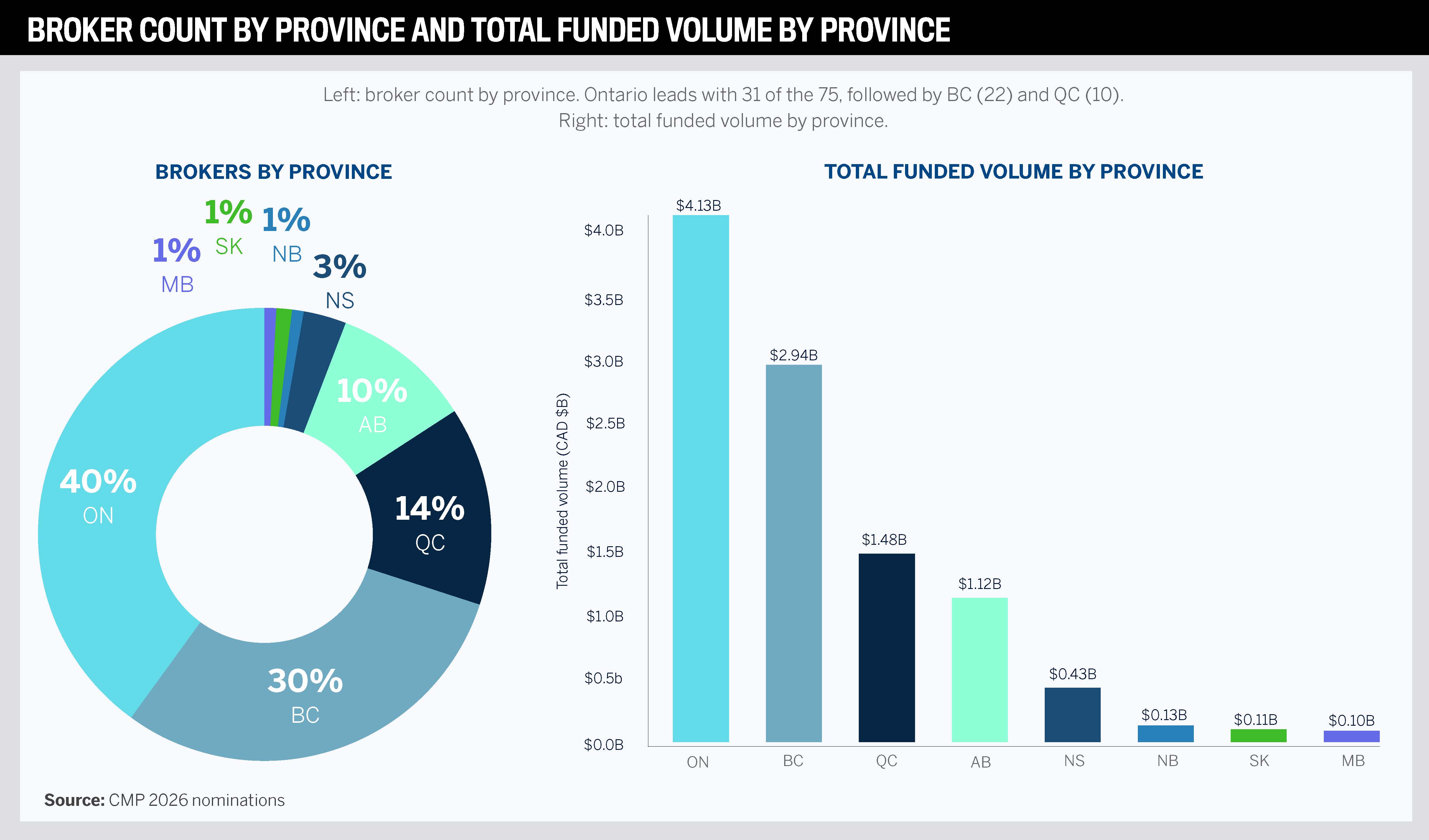

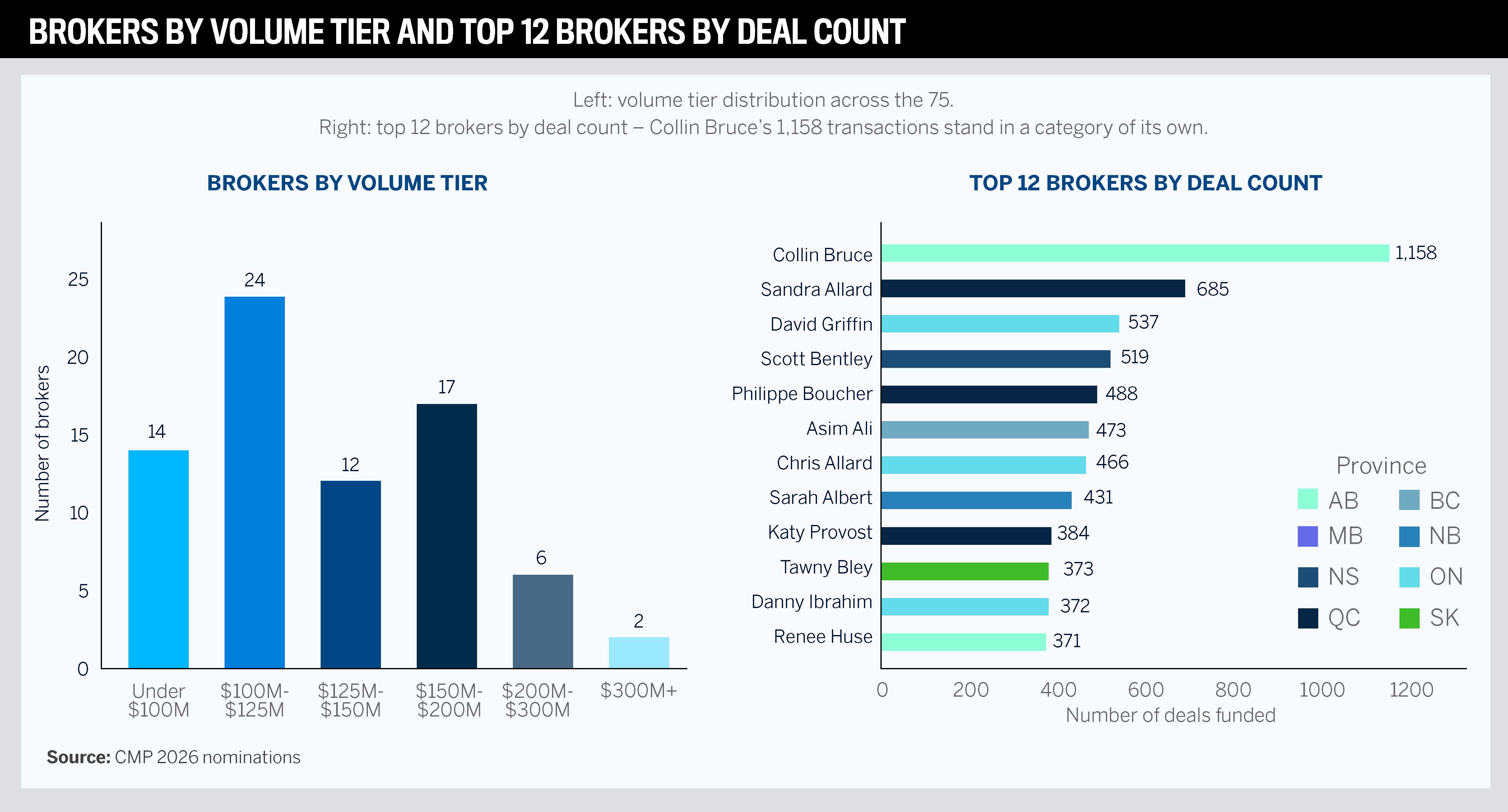

The charts below present the full picture of how Canada’s 75 best mortgage brokers performed in 2025 – across volume, deal count, geography, and competitive tier – and how their collective output sits within the broader Canadian mortgage market.

Among the best mortgage brokers in Canada recognized this year, five shared their stories. They operate in different provinces, serve different client bases, and have built their businesses through different methods. What they share is a clarity of purpose, a refusal to blame external conditions, and a belief that the job of a mortgage broker is about far more than moving paper.

No one in Canada funded more residential mortgages in 2025 than Collin Bruce. The Edmonton-based broker closed the year with $391.7 million across 1,158 individual transactions, placing him at the top of both the overall Top 75 and the Small Market category. He has previously completed the “trifecta” — first in the Top 75, CMP Broker of the Year, and Brokerage of the Year in the same year. He came to mortgage brokering by chance, arrived with a debt load from a previous business, and built from scratch. He has never forgotten that feeling, and credits it with an attitude that treats every lead as something that matters. His approach to client retention includes DLC’s Gold Rush CRM and a dedicated “Director of Wow” whose sole job is post-funding client experience.

Always doing what’s right for clients and not what is best for me. I have helped a lot of clients without making any money. I never have to worry about something coming back to me from a previous client.

We’ve been focusing on refinances as clients are feeling the higher mortgage rates coming out of those ultra-low rates. Also focusing on AI to help streamline our business and attract new leads.

John Burke built Burke Financial on a premise that sits at the heart of everything the Top 75 celebrates: the right people in the right seats can outperform any market condition. His 2025 volume of $200 million across 200 deals was driven largely by privates and B-lender transactions. His client experience philosophy is uncompromising: obsessive attention to empathy, from first contact to post-close. He focuses his team on what is controllable – the client experience, the lender network, and the quality of every interaction.

Prioritizing client experience and not allowing myself to make excuses for lack of results.

As borrowers become more educated, agents and brokers will need to be more knowledgeable and work with a higher level of professionalism, which is good for the industry as a whole.

Hugo Fortier describes his professional philosophy with a metaphor that is both disarming and precise: he practices his craft like a big brother – listening, supportive, present, and ready to help. Sixteen years into a career built in Blainville, QC, he still feels the same excitement at an approval that he did at the beginning. His market demands that he be something more than a rate-comparison engine, and he has built his reputation on doing precisely that.

Clarity, trust, and consistency. First, making sure they fully understand their options and the strategy we’re putting in place. Second, building trust through honesty and guidance. Finally, consistency in the experience, from the first conversation to the final approval and beyond.

My focus will be on maintaining continuity in our growth while staying true to what has made us successful – putting people first. When a team feels supported, aligned, and motivated, it naturally reflects in the quality of service we provide.

Carlo Del Giudice arrived in mortgage brokering through banking – a TD background that gave him a strong foundation in underwriting, structure, and risk – and a conviction that he wanted more control over outcomes. He closed 2025 with $100 million across 125 deals, a ratio that speaks to the complexity and ticket size of the files he handles. His specialty is execution under pressure: pre-construction closings with appraisal challenges, complex income structures, high-friction files that require strategic positioning from the very first submission.

Discipline and focus. We didn’t chase. We focused on doing a few things exceptionally well. Consistent process, consistent communication, and consistent relationships. Over time, that compounds.

A combination of strategic partnerships and content-driven positioning. We work closely with realtors, developers, and financial professionals who trust us to handle complex files. The focus is simple: demonstrate trust and value before the client ever reaches out.

Micky Khaneka does not describe the hardest parts of his job as the complex files. He describes them as the clients who arrive carrying decisions made in better times that now feel like burdens. Over hundreds of files and four years in the industry, he has built a reputation as a broker who can stand beside clients in precisely those moments. His $180 million in 2025 volume, across 220 deals, was driven by a foundation he describes simply as trust – the kind built when clients from five years ago now send their children and friends.

Constant communication and genuine care. Financing a home is one of the most significant things most people will ever do financially, and the questions don’t stop at closing. Life shifts, circumstances change, markets move, and renewals arrive. Clients deserve to have someone who knows their full story.

It’s the end of a file that didn’t come easy – when a client who came to us having been told no, or carrying a situation that felt like a dead end, reaches an outcome they genuinely didn’t think was possible. When a client thanks you with real relief in their voice, that’s the measure of the work. Everything else is secondary.

The best mortgage brokers in Canada share a set of qualities that transcend market conditions. They are trusted advisors first and transaction processors second — professionals who invest in long-term client relationships, remain selective with their lender partnerships, and show up with consistency whether the market is easy or hard. They combine process discipline with genuine human empathy, understanding that behind every file is a family navigating one of the most consequential financial decisions of their lives. Volume, it turns out, is not the goal. It is the reward.

If this year’s class of Top 75 Brokers shares one conviction about the year ahead, it is this: 2026 will be defined by renewals. The data bears this out. CMHC projects 1.15 million renewals in 2026 alone – more than in any recent year – and a significant majority of those borrowers will be transitioning from rates well below those available today. The financial anxiety that creates is real, and the demand for expert guidance has never been higher.

The best mortgage brokers in Canada are ready for what comes next. They have spent the past year – and in many cases, the past decade – building the relationships, the systems, and the reputations that make them the first call when a client needs help. And with broker market share now at 33 percent and the UK demonstrating what 80 percent looks like, the runway ahead is long.

The CMP Top 75 Brokers report is Canadian Mortgage Professional’s annual ranking of the highest-performing residential mortgage brokers in Canada, measured by verified funded volume. Published each year, it is the definitive benchmark for excellence in the Canadian mortgage brokerage industry, identifying the professionals who have personally originated and funded the most residential mortgage business over the preceding calendar year.

Nominations open in January each year. To be eligible, brokers must have been licensed and actively working in Canada throughout the year of measurement. All mortgage deals must have been personally initiated by the broker and must consist exclusively of residential transactions. Crucially, funded volumes are not self-reported alone — they are verified by the broker’s aggregator, franchisor, or lender before any placement on the list is confirmed. This verification process is what gives the rankings their authority and credibility.

The 2026 report reveals a market in transition. Canadian residential mortgage debt has reached $2.3 trillion, the broker channel now commands a 33 percent market share, and 2026 is set to be the largest renewal year in recent history with 1.15 million mortgages coming up for renewal. The data show that the best mortgage brokers in Canada are not simply riding a buoyant market — they are winning business by outperforming banks on service, advice, and client experience in an intensely competitive environment.

According to the brokers profiled in this report and the industry experts consulted, the common thread is a shift from transaction-focused thinking to advisor-led practice. Top brokers invest in long-term client relationships, build disciplined internal processes, maintain selective but deep lender partnerships, and treat every renewal and refinance as a strategic opportunity rather than an administrative task. Volume at the level of this list — some brokers funding over $200 million personally in a single year — is the outcome of years of consistent, client-first behaviour.

The Top 20 Small Market Brokers is a dedicated category within the CMP Top 75 that recognizes outstanding performance outside Canada’s major urban centres. To qualify, at least 80 percent of a broker’s residential funding must come from markets where the average home price is $657,145 or below. The category exists because exceptional brokers operate across the country — not just in Toronto, Vancouver, and Montreal — and their achievement deserves to be measured on an appropriate basis.

Broker market share is a proxy for the health and relevance of independent mortgage advice in Canada. At 33 percent in 2024, brokers now originate roughly one in three new mortgages in the country — up four percentage points since 2022. Countries like the UK, where brokers hold approximately 80 percent of the market, demonstrate how far the channel can grow when consumers understand the value of independent advice. Every percentage point of market share gained by brokers represents more Canadians accessing a wider range of lenders, products, and genuinely independent guidance.

The report serves multiple audiences. For mortgage professionals, it is a benchmark – a clear picture of what the top of the profession looks like and the strategies that drive sustained high performance. For lenders, it identifies the broker partners generating the most volume and provides insight into what those brokers need to thrive. For consumers seeking the best mortgage brokers in Canada, it is a verified, independently assessed guide to the professionals who have demonstrated the highest levels of funded residential volume. And for the industry as a whole, it is an annual record of the standard of excellence in Canadian mortgage brokerage.

The nominations opened in January for CMP’s 2026 Top 75 Brokers. To be eligible, nominees must have been licensed and employed as brokers in 2025. All mortgage deals and volumes had to be personally initiated and could only include residential-based mortgage deals. Overall funded volumes for 2025 that were verified by aggregators/franchisors/lenders formed the basis of the Top 75 selections.

In the Top 20 Small Market Brokers category, CMP also showcased those who are breaking new volume barriers in markets where at least 80 percent of the broker’s business is from average home prices of $657,145 or under.