Jump to winners | Jump to methodology

Brokers across the country have spoken: the best mortgage lenders in Canada are those delivering consistent, high-quality broker support alongside competitive, high-performing products.

Canadian Mortgage Professional’s annual 5-Star Mortgage Products survey allowed brokers to share their preferences and priorities in order to rate lenders and their offerings across key mortgage segments.

Those recognized in the survey will play a key role, as 1.2 million mortgages across Canada are set to come up for renewal in 2025. A study by Statistics Canada and Canada Mortgage and Housing Corporation (CMHC) states, “Most of these will experience higher interest rates than when their term began – 85 percent of those were contracted when the Bank of Canada rate was at or below 1 percent.”

The survey also showed that residential mortgage debt in July 2024 had increased by 3.5 percent compared to July 2023, reaching $2.2 trillion.

CMP’s 19 winning mortgage lenders stood out to brokers for consistently delivering in three key areas:

service excellence and relationships: brokers repeatedly cite reliable, responsive BDMs, underwriters, and support teams as major differentiators

competitive rates and flexible products: pricing remains a core driver, especially when combined with practical product features or a lender’s willingness to be flexible

speed, common sense, and approvals: fast responses and straightforward underwriting are still high on the list; lenders that take a pragmatic, solutions-focused approach are more likely to earn repeat business

As Jared Stanley, Neighbourhood Holdings senior director of originations and chair of communications committee of the Canadian Alternative Mortgage Lenders Association (CAMLA), points out, “A great product isn’t just about a low rate; it’s about how well it fits with the borrower’s life and financial reality.”

Canada’s trio of reverse mortgage lenders earned top marks from brokers this year, including repeat winner HomeEquity Bank (HEB), which continues to lead as demand with this niche solution steadily grows.

“The shifting demographics are hard to ignore,” explains Rene Quercia, senior vice president of the broker channel at the Schedule 1 bank. “The aging population in Canada means more and more people will need our product. And because we are the only bank in Canada focused exclusively on serving customers aged 55+, we’re well equipped to respond to their needs. We’re specialists in working with that demographic.”

With the baby boomer generation entering or nearing retirement and holding more than $1 trillion in real estate equity, HEB sees the opportunity to tailor its products to evolving client goals, from lifestyle upgrades to intergenerational wealth transfer.

It has already launched HomeBridge, which enables parents to gift down payments to their adult children who are buying a home. They’re also developing other products to address unique needs, such as monthly income, major purchases, or real estate investments.

From Stanley’s point of view, the best products in the reverse mortgage space offer clear education, flexible withdrawal options, transparent costs, and factor in long-term planning to protect the borrower and their estate.

HomeEquity Bank shares a similar perspective on market evolution, with Quercia noting, “We’re looking at ways to tailor reverse mortgages to specific goals. Whether it’s lifestyle, income, or legacy planning. That’s how we see the product evolving and where we believe the real opportunity lies.”

To help brokers meet rising demand in the reverse mortgage space, HomeEquity Bank has expanded its operational capacity and is exploring new digital tools to streamline the process and improve broker support.

The bank’s initiatives include:

doubling the size of its broker-dedicated operations team, with more underwriters, funding officers, and client-facing staff to ensure speed and support, front to back

developing a new broker portal that allows brokers to track deal progress from submission through to completion, minimizing the need for manual follow-ups

introducing digital options to simplify the client onboarding process and improve efficiency for both brokers and borrowers

balancing short-term scale with long-term innovation as part of a broader strategy to automate and digitize the reverse mortgage experience

“The idea is simple: more people, better communication, and faster turnaround,” Quercia adds. “Brokers will start seeing the impact of that ramp-up this year (2025), especially in Q3 and Q4.”

As lenders respond to shifting market conditions and rising client expectations, brokers are also refining how they evaluate mortgage products and partners, placing increasing emphasis on the factors that impact their business.

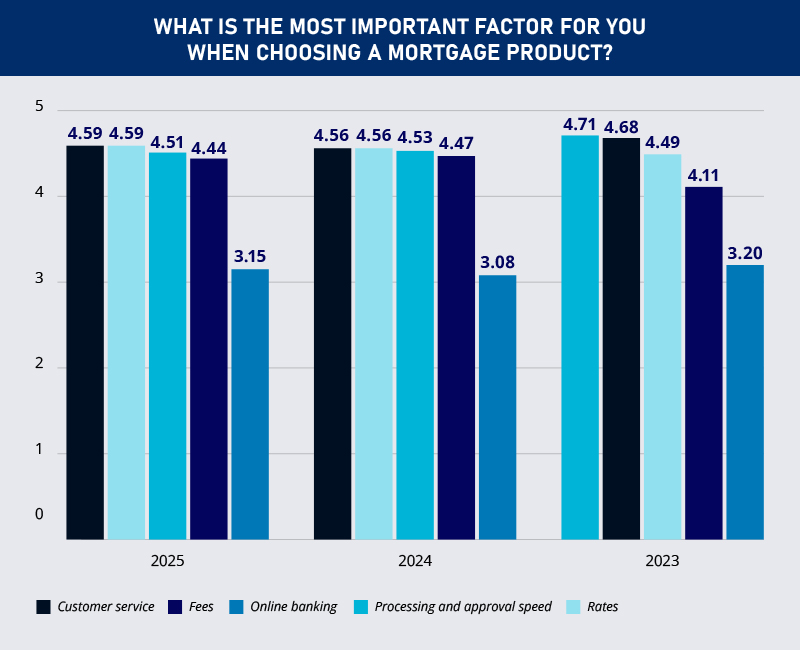

An analysis of CMP’s data from 2023 to 2025 reveals meaningful shifts in what brokers value most when choosing mortgage products for their clients. The insights highlight an evolution in broker priorities, with service, pricing, and process efficiency all playing critical roles in product selection.

In 2025, customer service and rates tied as the most important factors for brokers, both receiving a rating of 4.59 out of 5. This marks a subtle but important shift from 2023, when processing and approval speed led broker priorities.

The rise of customer service to match rate competitiveness suggests that brokers are increasingly focusing on end-to-end lender support, not just pricing. With the mortgage market remaining complex and highly competitive, brokers are placing greater value on responsive service and reliable communication in tandem with sharp rates.

When asked which lender they’ve given more business to in the last 12 months and why, brokers said this about this year’s winners:

“RMG is my go-to for quality products, competitive rates, and client and broker service. The BDMs are hands down the best in the industry”

“Equitable Bank because they have competitive rates and turnaround is pretty good”

“MCAP is very stable with the same underwriter for many years and is the best in industry”

“Calvert because they are best on Alt, private side, and their own quick appraisal system can fund in two days”

“Strive because the rates have been very competitive, and they do common-sense lending. Some lenders are far too ridged”

“TD because of lower rates and cashback and Scotia Bank due to their ratio exceptions on conventional mortgages, plus their rental offset”

As broker priorities shift in the products they recommend, what matters most in 2025 is clarity, confidence, and consistency, according to Stanley, along with:

fast, transparent approvals powered by modern technology

product reliability offerings that won’t shift dramatically post-closing

strong lender support backed by clear communication, accessible underwriters, and aligned values

“More than ever, brokers want partners, not just products,” he adds. “Lenders who invest in education, responsiveness, and co-branded support tools will stand out.”

At CAMLA, Stanley observed that the broker-lender relationship is a key driver of trust and success in Canada’s mortgage market.

While still a top consideration, processing and approval speed has seen a slight but consistent decline, from 4.71 in 2023 to 4.51 in 2025. This shift suggests that brokers are no longer chasing speed alone; they’re equally focused on working with lenders who deliver consistent service and reliable outcomes.

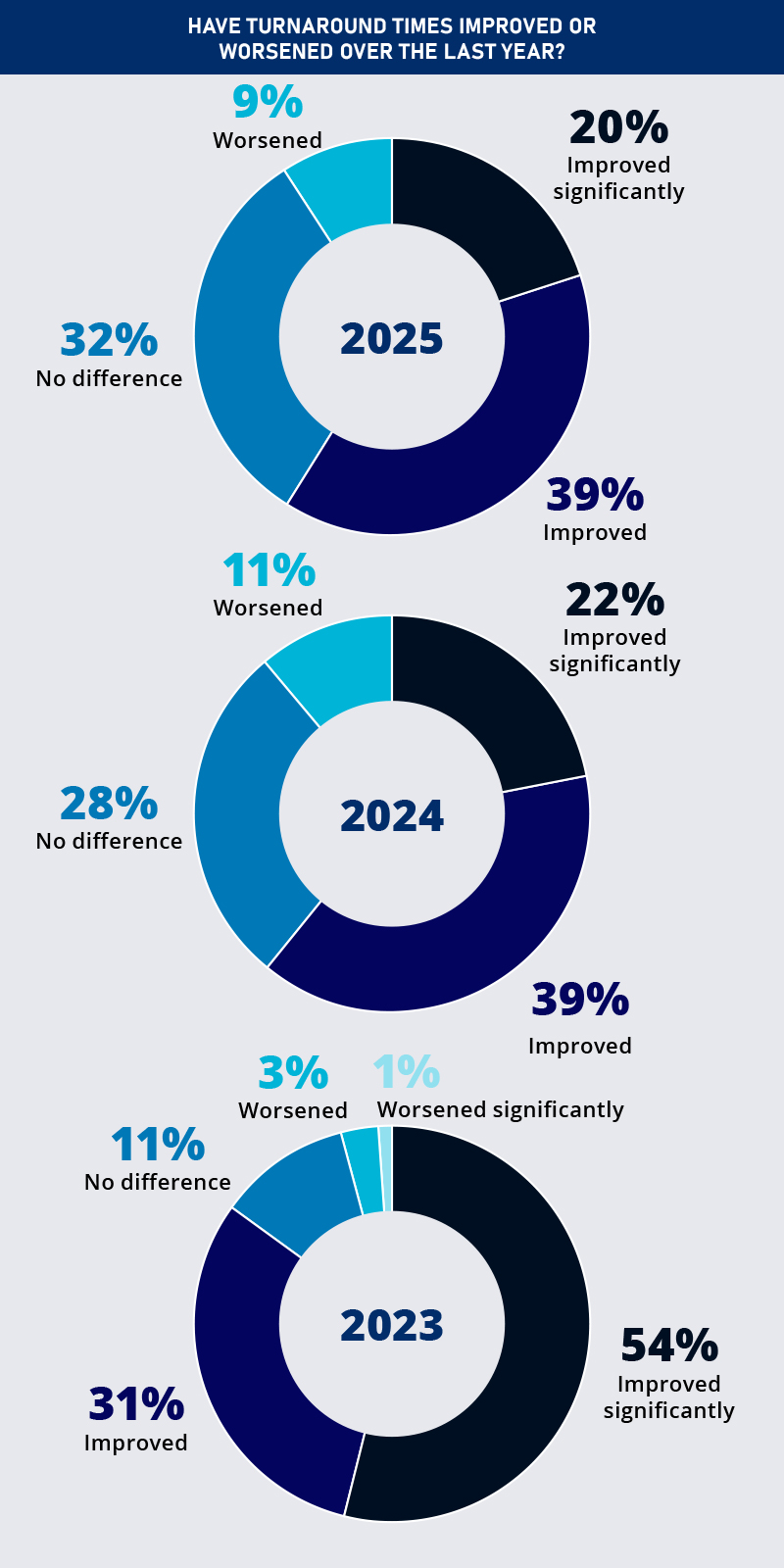

Broker sentiment around turnaround times has cooled considerably over the past three years. In 2023, a majority of brokers, or 85 percent, said turnaround times had improved, with over half reporting significant improvement.

By 2025, that number has dropped to 59 percent, with only 20 percent saying they’ve seen a significant improvement. Meanwhile, the share of brokers saying there’s been no difference has nearly tripled since 2023, and the percentage reporting worsening conditions, while still relatively small, has crept upward.

It’s clear that turnaround times still matter, but brokers don’t seem as optimistic about continued improvement. The numbers suggest that gains in efficiency may have levelled off, or at least no longer stand out the way they once did.

Lenders can no longer rely on speed alone as a differentiator; service consistency, communication, and flexibility are now just as crucial to winning broker trust.

This kind of support is central to HomeEquity Bank’s approach. With nearly 40 BDMs dedicated to the broker channel, the bank has structured its team to work as strategic partners.

“Our BDMs aren’t out there pushing product,” says Quercia. “Their job is to train, educate, and work shoulder-to-shoulder with brokers who want to focus on this segment. They help brokers look at their database at clients who may be retired, mortgage-free, and previously overlooked, and identify where there might be a real opportunity to help.”

That broker-first mindset, he explains, is what shapes the bank’s field-first approach.

“We don’t expect every broker to sell our product. We’re focused on the ones who want to specialize, who want to develop their business around this need,” Quercia says. “And for them, we roll up our sleeves and help. We support marketing, help with strategy, and ensure they’re not doing it alone.”

As competitors tend to match product features over time, HomeEquity Bank gains an edge with its singular focus on serving Canadians aged 55 and over. That specialization shapes its entire operation.

“This is all we do. Our teams are trained specifically to deal with older Canadians, and they understand the unique needs, challenges, and anxieties that come at that stage in life,” Quercia says. “We’re also a recognized brand. When you add it all up – specialization, service, brand trust, and smart innovation – we think we offer a value proposition our competitors simply can’t match.”

Fees have grown in significance, rising from a score of 4.11 in 2023 to 4.44 in 2025. In a market where clients are increasingly cost-conscious, transparency around product fees is becoming a differentiator. Brokers are paying closer attention to cost structures and how they impact the overall value proposition for clients.

Despite digital innovation across the lending space, online banking functionality remains the least influential factor in broker product selection, holding steady at around 3.1 over three years. This suggests that while digital tools may enhance the client experience, they are not a deciding factor in broker product choice.

fixed-rate mortgages, both three-year and five-year terms

investor-focused mortgage products, such as BRRR/Flip

flexible and niche products

Brokers’ top three mortgage product picks from the past 12 months reflected shifting borrower needs, highlighting key trends that shaped the market. Fixed rates, investment lending, and flexible qualification rules have emerged as factors influencing lender offerings.

As Stanley remarks, “The top alternative products offer speed, clarity, and compassion, bridging borrowers to stability or growth while maintaining strong risk management for investors.”

Regarding first home buyers who are facing unprecedented affordability challenges, he says what’s encouraging are products “designed to build long-term homeownership resilience, not just offer a short-term solution.”

“On the policy side, programs that support down payment assistance, tax incentives for new buyers, and financial literacy initiatives are also essential elements,” he adds.

To determine Canada’s best mortgage products, Canadian Mortgage Professional conducted an online survey asking brokers about their preferences and priorities when selecting mortgage products for their clients. The survey was open to brokers across Canada, who were asked to provide product recommendations across a range of different areas, including fixed and variable rate products, commercial, and refinancing.

For each lender they nominated, brokers were asked to rate the offerings they provided on a scale of 1 (poor) to 5 (excellent). They also identified the most important factors they and their clients consider when choosing a mortgage product, as well as their most significant area of growth this year.