Lenders, LMI provider help brokers and clients navigate challenges

Resilience and adaptability – these are the traits small business owners must display as they grapple with a variety of pressures.

It’s tough for SMEs in the current economic environment.

Consumer spending is down and interest rates have risen considerably, while burdensome regulations and the higher costs of doing business have also taken their toll.

SMEs are also finding it difficult to secure finance from mainstream banks as their credit appetite for more complex lending wanes.

But in a nation dominated by small and medium businesses, owners have shown they can survive and adapt to new challenges – the recent COVID pandemic being a case in point.

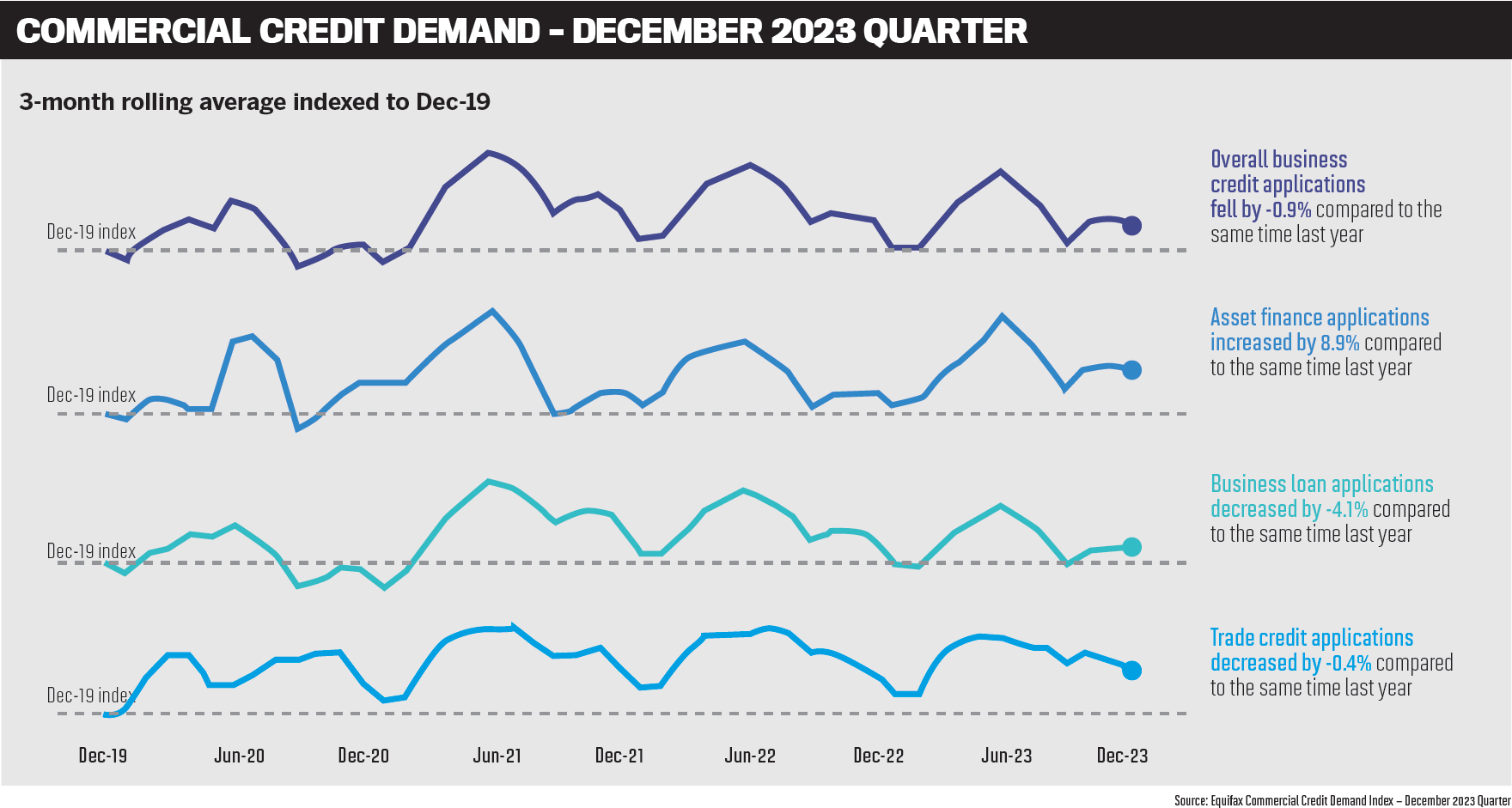

Equifax’s Quarterly Commercial Insights – December 2023 report revealed that overall business credit applications reduced by 0.9% in Q4 2023 when compared to the December quarter in 2022. Business loan applications fell by 4.1%, compared to the December 2022 quarter.

However, non-bank lenders are seeing a rise in SMEs which have adapted to rising interest rates, are wanting to grow and need a range of finance options to do so.

To gauge the SME lending market and the opportunities for brokers, MPA sought the views of two non-banks and an LMI provider: Prospa director of sales and partnerships Roberto Sanz (pictured above left), Dynamoney CEO David Verschoor (pictured above centre) and Helia chief commercial officer Greg McAweeney (pictured above right).

Challenges facing SMEs

Sanz says macro-economic factors, including rising operating costs and inflation, are continuing to place pressure on SMEs, which has forced lenders to re-evaluate their credit risk appetite.

“As a result, there has been a decrease in overall business credit applications,” says Sanz. “However, Prospa has seen significant growth in partner engagement, with the number of partners actively submitting leads up 22% year-on-year, which suggests that SME lending demand persists.”

Sanz says in direct response to the challenges contributing to the fall in credit applications, many small business owners may feel their eligibility for finances is increasingly complex to understand.

“As a result, SMEs have been actively seeking advice from brokers to navigate these challenges and secure the funding they still demand,” Sanz says.

McAweeney says the decline in business credit demand has predominantly been driven by the construction, retail and hospitality industries.

“This is largely due to the decline in business activity and consumer spending and the rising interest rate environment,” says McAweeney.

“While overall business lending has declined in NSW and Victoria, the recovery of the mining sector has led to an increase in the demand for business credit in Queensland, South and Western Australia, as identified in the recent Equifax Quarterly Commercial Insights (December 2023).”

Verschoor says 2023 was a tougher year for SMEs, with increasing interest rates and the high cost of doing business being major themes, “but we’re seeing the sector adapt to these challenges”.

“Although the market may have seen falls, Dynamoney has experienced growth thanks to the launch of new products and securing additional funding for more loan capacity.”

SMEs usually maintain more direct relationships with their customers and suppliers, which allows them to work together on mutually beneficial solutions to challenging market conditions.

Verschoor says SME application volumes at Dynamoney have risen this year. “Asset finance solutions and business loans are the most sought after, showing a desire to invest in growing a business rather than refinancing previous loans.”

The non-bank lender has launched its Business Overdraft Mastercard Account, the first business overdraft account to come with an interest-only Mastercard credit card, giving SMEs maximum flexibility when accessing financing.

Market growth

Verschoor says SMEs are adjusting to the new interest rate landscape and looking to grow again.

“We’re seeing increased application volume for a number of our products, and encouragingly, from a wide range of industry sectors spanning transport and renewable energy, through to IT and retail.”

The applications, strongest across business loans and equipment financing, signal that SMEs are investing in expansion and growth instead of refinancing.

Verschoor says SMEs still require simpler access to capital to guarantee free cash flow.

“Dynamoney’s asset finance solution means you can purchase almost any business asset imaginable.”

Sanz says as challenging market conditions persist, Prospa has identified an SME growth opportunity called the Established Small Business segment, for SMEs with at least two years trading and an average monthly turnover of $100,000 plus.

“These businesses are more likely to explore the value of alternative lending through a financial adviser and are generally able to service greater loan amounts,” he says.

“We have attributed an increase in the average loan value of 14.7% written by Prospa Partners, year-on-year, to this segment.

“On top of this, we’re continuing to see a lot of traction within the professional services, retail and hospitality industries.”

As a lenders mortgage insurance provider, Helia currently offers an SME residential product which is being assessed by lenders, says McAweeney. It enables SMEs to use their existing residential property to access funding.

“These offerings can be structured either as a single upfront payment or as a monthly premium, mirroring the approach taken with Helia’s traditional residential LMI.”

Opportunities, partnerships

McAweeney says Helia has engaged with a range of business brokers and lender partners to assess the credit requirements of SMEs.

This identified a growing demand for enhanced access to credit, allowing banks to broaden their lending capacity by extending limits on LVRs and loan sizes.

“Helia’s collaboration with brokers in the SME lending space expands their market reach and allows them to offer innovative products and services to a wider audience of small to medium-sized businesses to support them in achieving their goals and drive economic growth,” says McAweeney.

Sanz says broker partners can tap into SME finance opportunities by building awareness, creating appetite, and providing access to funding solutions to their network of existing and new self-employed business clients.

“We have a dedicated team of BDMs that get to know your clients’ businesses and provide fast, tailored solutions, and offer resources to help partners find and win more business in the market.

“We understand the value of relationships in finance and the 22% growth in partner engagement, year-on-year, tells us the support we offer to our partners is working.”

Sanz says Prospa remains committed to empowering its partners to strategically engage with clients and grow their business.

Read next: Ways to get real estate leads

“We are continuing to invest in the broker channel, with a new tool to improve and ease the experience of writing of business loans coming soon, just in time for EOFY.”

Verschoor says SME financing is built to fit the lives of SME decision-makers, meaning it is decentralised and easy to access, so it’s convenient for business people always on the move.

“Brokers are very accustomed to working with clients in an agile way, so Dynamoney has always invested in developing the most effective online lending platform in the market to fit both client and broker needs.”

Verschoor says the non-bank’s products are listed with most aggregators, and “we are always investing in education initiatives to help mortgage brokers expand into SME lending services”.

“Our lending platform is safe, convenient, fast, easy for brokers to use, and we’re constantly enhancing it, having just added new security and application processes that further reduce loan approval times.”

Loan approvals take a few minutes, and Dynamoney’s large BDM team can help brokers with their applications.

Broker diversification

Sanz says SME lending offers brokers an easy path to understanding and writing business loans and building protection around their existing loan book.

He says many small business-owners feel their finances are complex and are more comfortable dealing with a broker than with a bank or finance company.

“Leading lenders, like Prospa, provide tailored support and experience-driven advice to help brokers tap into hidden value, creating stickier relationships, and building new revenue streams.”

McAweeney says given the dynamic nature of business lending, brokers can leverage their relationships with borrowers to offer holistic finance support.

He says diversifying into SME lending is compelling for brokers for a number of reasons, including:

- expanded market opportunities. There’s a growing demand for financing solutions tailored to suit unique SME needs, and brokers can tap into this large and under-served market segment;

- additional revenue streams;

- expanded existing client base – many SMEs already have established relationships with brokers for other financial services. By offering SME lending, brokers can deepen these relationships and become a trusted partner for their client’s financial needs;

- providing value-added services to their clients beyond traditional mortgage brokerage services; and

- competitive advantage – brokers who offer SME lending services can differentiate themselves from other brokers solely focusing on residential.

“With business lending being the second-largest lending market in Australia after residential lending, catering to SMEs presents an excellent opportunity for brokers to diversify and expand their business,” McAweeney says.

Verschoor says the 2.5 million SMEs in Australia are the lifeblood of the economy, making up more than 97% of registered businesses.

“They are looking for faster, easier, safer lending solutions and are seeking the support of finance professionals like brokers to helpthem navigate the market,” he says.

Diversifying into SME lending can increase the value brokers can provide to their clients, helping enhance client retention and revenue per contact.

“With a large number of home and property buyers having a small to medium-sized business, the opportunity for brokers to build stronger pipelines into mortgage lending is very real.

“Additionally, successful SME loans maintain upfront brokerage and commission payments for brokers, a consistently strong revenue channel.”

Lending solutions

Verschoor says that Dynamoney has a comprehensive suite of working capital and asset finance products for SMEs designed to be better for business, including its new Business Overdraft Mastercard Account.

He says the non-bank can help SMEs with all their financial challenges, from ensuring free cash flow, financing new equipment, covering the cost of overheads such as insurance and accessing capital for growth.

“Our system is built for SME lending, with an experienced team focused on ensuring brokers and customers secure financing as fast as possible.”

Sanz says Prospa has delivered more than $4 billion in funding, helping over 54,000 small businesses manage their cash flow and fund growth opportunities with business loans up to $500,000 and a business line of credit up to $150,000.

What finance needs are SME clients discussing with you? Comment below