An inflationary period provides a great way for brokers to step in and assist SMEs by seeking funds from non-banks

There’s a lot going on when it comes to the nation’s estimated 2.3 million small businesses. They have enjoyed a post-COVID shot in the arm since state and international borders reopened and consumers took the opportunity to cast off the pandemic shackles, and get out and spend money.

From a consumer perspective, while spending remains strong, there is uncertainty as the cost of living rises and higher interest rates hit homeowners.

From a business perspective, SMEs are finding it tough to access goods efficiently as global supply chain issues persist. Cash flow constraints have now become a key risk for businesses’ operations.

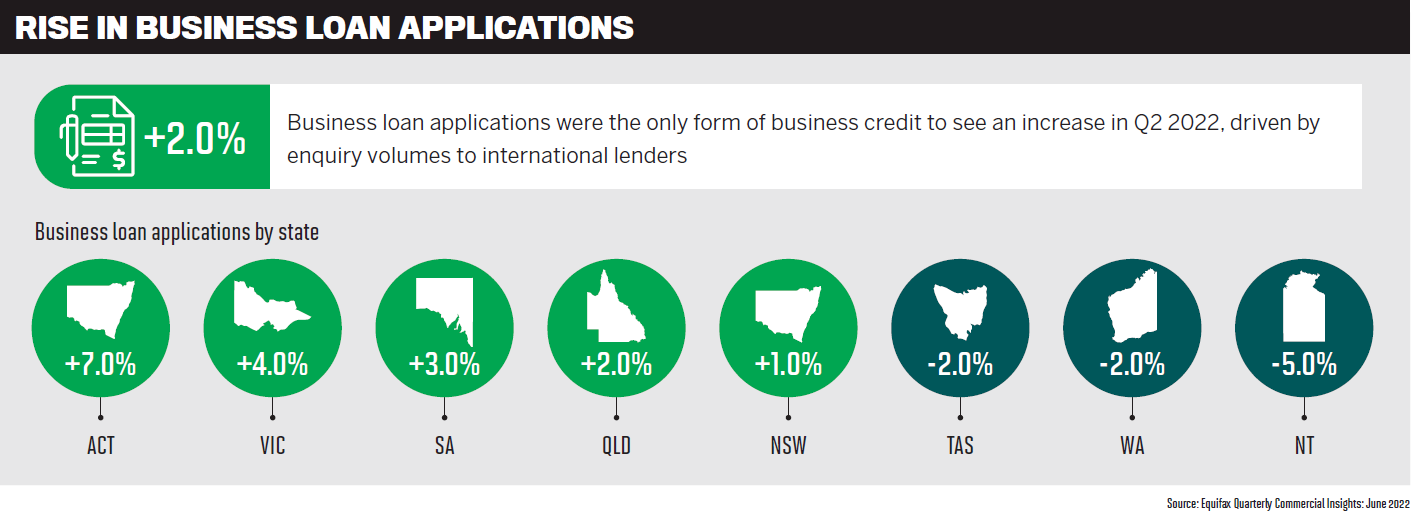

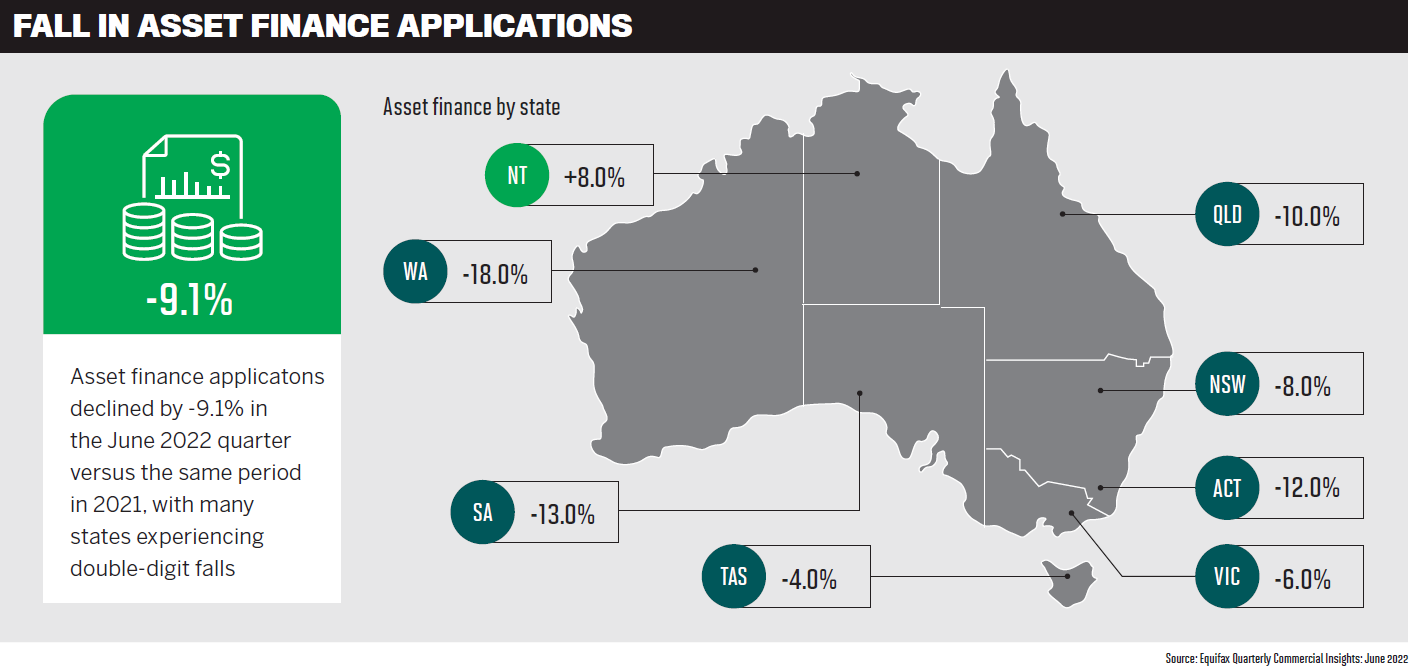

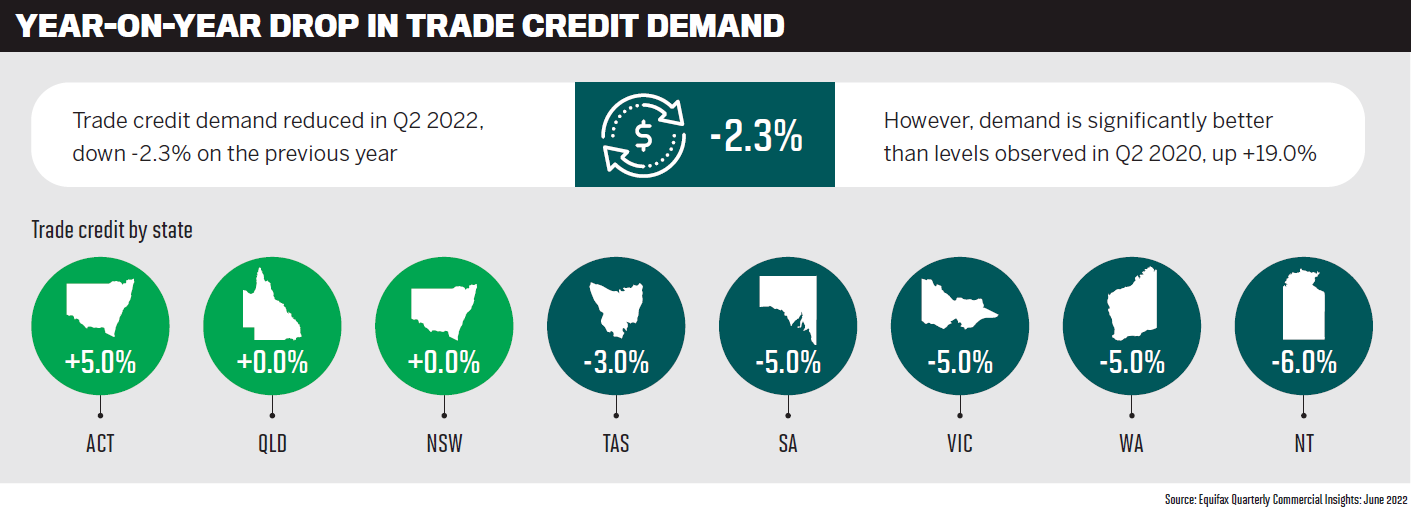

Equifax’s Quarterly Commercial Insights report for the June 2022 quarter shows that asset finance applications were down 9.1%, while trade credit applications decreased 2.3% and applications for commercial lending fell 2%.

However, business loan applications rose 2% and overall were still higher than in the March 2022 quarter and 13.8% higher than in the June 2020 quarter.

The news is also good for non-bank lenders. ScotPac’s SME Growth Index shows that the number of SMEs planning to borrow from non-banks has doubled in the past four years to 31%, growing 8% a year. The report also revealed that 55% of SME owners are planning to invest in their businesses in the next six months, while 41% said they would be seeking new funding options in 2022.

MPA catches up with non-bank lenders Thinktank, Prospa, OnDeck, Grow Finance and ScotPac to discuss opportunities in the SME lending market.

Demand from small businesses

Peter Vala (pictured below), general manager partnerships and distribution at Thinktank, says the majority of the non-bank’s borrowers are self-employed, so it hasn’t seen any drop-off in lending activity, despite rising cost and supply pressures.

“As a property secured lender, the demand for our products to assist with purchase, refinance or equity release has remained relatively consistent,” says Vala.

“However, there have definitely been stronger levels of consolidation of debts and structures to reduce monthly repayments and improve operating cash flow, which correlates with the reported increase in business credit applications.”

Thinktank has also seen a consistently strong flow of loan enquiries for commercial property purchases under alternative structures such as using an SMSF.

Prospa national sales manager Roberto Sanz (pictured below) says the lender’s recent survey results show that sentiment remains positive.

“Concerns around revenue instability have decreased even in the wake of rising interest rates and inflation,” says Sanz.

“This illustrates that business owners are feeling confident and well-equipped to deal with the tough operating environment.”

Small businesses are thriving by investing in their businesses, says Sanz. “Our research shows that 26% of businesses are expecting to access external funding over the next 12 months. Prospa’s performance reveals the same trend, with record-breaking originations for FY22 and July’s originations being up 58% compared to last year.”

Craig Michie (pictured below), group executive, client acquisition and asset finance at ScotPac, says there are very few, if any, SMEs that have not been directly or indirectly affected by rising interest rates and input costs, supply chain delays and inflation running above 6%.

“These challenges, along with government stimulus being wound back, have prompted most businesses to review their operating costs and their cash flow requirements and compare their access to working capital,” Michie says.

At ScotPac, SMEs and their brokers are looking for ways “to work smarter and make their money work harder”, so demand for the non-bank’s invoice finance and flexible business loan products has been strong.

“For customers impacted by supply chain delays, tailored trade and invoice finance solutions are creating a bridge between supplier payments and customer receipts, which relieves the pressure of day-to-day cash flow,” Michie says.

Biggest problems facing SMEs

Grow Finance co-CEOs Greg Woszczalski and David Verschoor (pictured below) say the biggest challenge for SMEs is accessing stock due to sustained supply chain disruption.

“This includes inventory to onsell, materials to manufacture, or hard assets to operate their business, which is placing tremendous strain on workflow, working capital and operations across a range of sectors,” the CEOs say.

In terms of the impact of RBA rate rises, Verschoor says that while business finance isn’t directly linked to the cash rate, there has been an increase in the cost of funds in the wholesale market over the same period as the interest rate rises.

OnDeck Australia CEO Cameron Poolman (pictured below) says the biggest challenge the non-bank sees is “the need for speed”.

“We’re seeing applications for small business finance across every industry sector right now, though retail, construction and hospitality are particularly well represented,” Poolman says. “The common thread is the need for fast lending decisions and accelerated delivery of funds.”

Speed allows small businesses to take advantage of time-specific opportunities such as discounts on trading stock, which are especially important as SMEs stock up for the festive trading season.

“As a guide, OnDeck recorded 43% growth in loan originations in the first six months of 2022 following the company’s management buyout by an Australian team in late 2021,” Poolman says.

He says a key driver of this growth was the increase in OnDeck’s Lightning Loan capability, allowing small businesses to access unsecured funding of up to $150,000 within two hours, with just six months of bank statements, up from $100,000 pre-management buyout.

OnDeck knows from past research that among those small businesses approved for finance by a traditional bank, around one in four will experience negative outcomes. This is due to the time taken to apply for a loan – and for that application to be processed and assessed by the bank. There is just no place for this sort of delay in today’s fast-tracked business environment, Poolman says.

OnDeck’s interest rates are bespoke to each customer and determined case by case, so there is no single standard rate that captures the impact of RBA rate hikes.

“This is good news for small businesses as they are not subsidising the rate paid by a higher-risk venture,” he says.

Read more: Opening new doors to growth in commercial finance

Michie says finding skilled employees and fast access to finance are the two biggest roadblocks to SMEs reaching their revenue targets right now. He says some measures from the Skills and Jobs Summit will help on the employee front, but recovery will still take time.

“We’re working hard to raise awareness among brokers and the SME community that access to finance doesn’t have to be a cumbersome, stressful and drawn-out process,” Michie says. “At ScotPac, we’re constantly working to improve speed and efficiency in delivering our solutions. We know that fast and flexible finance is important to brokers and their clients.”

Michie says interest rates for business finance have generally increased in line with the official cash rate, but “there’s never been a more important time for SMEs to work with their brokers to explore finance options”.

At Prospa, Sanz says small business owners have pointed to operating costs, inflation and fuel costs as their greatest concerns.

“Despite these challenges, we’re seeing small business owners display grit and creativity to work through the current environment and find solutions. That’s why seven in 10 still rate the health of their business as good or very good, and the majority expect growth,” Sanz says.

“We encourage brokers to reach out to their small business clients now, as we’re seeing more business owners looking to invest to continue growing and be prepared to take on the current environment.”

Sanz says funding solutions such as Prospa’s products allow businesses with fixed-cost repayments to confidently forecast cash flow.

Vala says some of the key issues, along with rising interest rates, are an anticipated reduction in discretionary spending, as well as increasing serviceability requirements to qualify for a loan facility.

“This is where the freeing up of cash flow is critical,” he says. “If there are also staffing and supply chain problems, then available billing hours and level of trade can also be impacted.”

Vala says that if all cash flow, staffing and trade pressure problems occur at the same time, this may lead to technical default issues, where a loan is not in arrears but may be in breach of reporting covenants such as maintaining certain serviceability or leverage ratios.

“Technical defaults may trigger a re assessment of current lending facilities and can be avoided by working with the right lender,” he says.

Loan products to support SMEs

Poolman says OnDeck has maintained close contact with its small business clients and their brokers, offering support where it’s needed.

“Even in the very early days of COVID, many of our small business clients quickly pivoted to alternative revenue channels, which helped many survive, and even thrive,” he says.

The technology behind OnDeck’s KOALA Score™ credit assessment algorithm uses a sophisticated blend of big data, predictive analytics and statistical techniques, along with data from credit reporting agencies, including illion and Equifax, to support more tailored risk assessment for small business lending.

Poolman says by using a mix of commercial and consumer credit history plus cash flow, KOALA builds a holistic risk profile. “OnDeck is able to lend rapidly but also responsibly, and we have a very low rate of delinquencies.

Our experienced team of BDMs maintain regular contact with all our small business clients and brokers, so any issues are addressed and managed at an early stage.”

Grow is increasingly being recognised as the “non-bank of choice” for business by providing funding that holistically meets SMEs’ cash flow needs, including business loans, asset, trade, invoice, floorplan, and insurance premium finance, says Woszczalski.

“Grow’s point of difference is its ability to respond to current and emerging market demand with sharply priced product enhancements, product extensions and new products – single and blended,” he says.

Verschoor says Grow encourages brokers to reach out to their local BDMs and tell them how business funding can help their SME clients.

“Grow currently employs over 60 staff, has offices in Sydney, Melbourne and Brisbane, and has BDM presence in all states,” he says. “Each BDM has a designated account manager to enhance efficiencies.”

The co-CEOs say the non-bank will recommend the aligned product – whether it’s a straightforward single or blended solution. This model removes the requirement of the broker to be across the nuances of each asset finance or working capital facility.

“High-touch BDM support is backed by Grow’s highly sophisticated technology, which is intuitive, automated and expedites the loan application process,” they say.

Michie says ScotPac implemented a range of support initiatives at the peak of the COVID-19 business interruptions, most notably the $100m SME Bounce Back Fund, providing the first three months of working capital interest-free.

“We have also continued to expand our products and services to ensure SMEs and brokers get the support they need as the economy resets,” says Michie, and he gives three recent examples.

ScotPac’s acquisition of Business Fuel means SMEs now have the option of a fast, online application process for business loans up to $250,000, he says.

For clients who need a range of finance facilities, ScotPac can now provide business owners with property finance, using the equity in their home to provide business funding – combined with invoice, trade or asset finance to offer a complete solution.

Finally, Michie says the non-bank’s new Partner Portal for brokers is a “real game changer”, providing the marketing and research brokers need to maximise the potential of their businesses. More than that, its new online fast-doc process allows for almost instantaneous approval.

Thinktank’s relationship managers (RMs) offer total support to its brokers and their clients, Vala says.

“While Thinktank can’t provide financial advice, we can workshop alternative lending structures with the broker, which they can then discuss with the borrower and their professional advisers.”

This might include refinancing existing facilities to ease cash flow pressures, and accelerating rapid refinance and reset options for SMSF transactions.

Vala says Thinktank’s ‘set and forget’ loans provide added peace of mind for borrowers, removing the technical default risk aspect of commercial lending, with no annual reviews or covenant compliance measures.

For SMEs looking to refinance, apply for cash-out or arrange a purchase, 2022 financials are not required until March 2023, so 2021 financials can still be used.

COVID lockdowns and restrictions meant the nature of trading recorded in these financial statements may not accurately reflect and may understate the borrower’s current trading position. Vala says this presents a problem for SMEs who want to use their current trading performance but don’t have their 2022 financials completed.

“Our Mid Doc loan is the ideal solution, where we only rely on an income self-certification and just one other form of supporting verification,” he says.

Sanz says business owners want flexibility to help them manage cash flow, so Prospa provides a standard feature option on their business loans of no repayments for up to four weeks.

“This grants clients the ability to cover immediate costs and access funding up front to take on opportunities now, with breathing space on the repayments,” he says. “Prospa also offers fixed-cost loans for terms of up to three years, providing certainty around repayments and costs to allow them to fore-cast their cash flow.”

Sanz says Prospa’s award-winning team is readily available to help brokers gain a greater understanding of the commercial lending market. It regularly runs educational webinars to keep brokers across SME market insights, as well as how they can support their clients and find opportunities within their databases.

“We also provide additional tools and marketing resources to help brokers generate leads and promote their businesses,” says Sanz.

Conversations with clients

Michie says brokers should be sitting down with their clients to look at, (a) what growth opportunities they could explore if they had better access to working capital, and (b) whether their existing finance facilities are the best fit for their current business needs and future plans.

“And they should talk to ScotPac, because we have the experience and breadth of product to help more businesses in more situations than any other non-bank lender.”

Vala says that during challenging economic times it’s important for brokers to keep in constant contact with their SME clients, especially to review loan structures and discuss future lending requirements.

“The priority is to look out for any potential issues, as well as identify areas to free up cash flow for the business,” he says.

Doing this may help avoid difficult conversations with lenders in the future and improve the incentives or discounts received for on-time or ahead-of-time payment of creditors.

“Most important is for the broker to listen to and understand the needs and goals of their SME client so they can ensure the current or proposed lending solution is aligned with the planned strategy and execution,” says Vala.

Sanz says it can be simple for brokers to identify potential funding opportunities among existing clients by asking questions on, for example, how they manage cash flow, where they see opportunities for growth, and any potential challenges they anticipate over the next 12 months.

“You’ll be surprised by what comes up,” he says. “Leading up to Christmas, many small businesses need access to capital for stock and staffing.”

Given current supply chain delays, Sanz says now is a fantastic time to reach out and add value to current and potential clients who may want to get stock ahead of time. “Our research shows that, on average, small businesses need funding and capital twice a year, so if you’re not asking the right questions, someone else will be.”

Verschoor says Grow recommends brokers conduct a “health check” with clients to review current facilities and their cash flow status and assess whether restructuring or refinancing may enable better access to capital and cash flow certainty.

“In a rate-rising environment, we suggest SMEs don’t delay equipment acquisitions, and fix interest rates now,” Verschoor says.

“We also encourage brokers to determine their customers’ capital requirements, both secured and unsecured, for the next six months; and, ideally, forecast in conjunction with accountants to help bypass blocks and enhance growth planning.”

Diversifying for growth

OnDeck research shows that one in four of a broker’s home loan clients are likely to be small business owners, says Poolman. “So there is every possibility that brokers have an untapped revenue channel right there in their current customer database.”

The non-bank offers a straightforward accreditation process and freely available marketing collateral for brokers to promote their commercial lending capabilities, so brokers “can be up and running with commercial lending in no time at all”.

Poolman says the benefits of expanding into commercial lending include brokers becoming a one-stop shop for all their clients’ financial needs, as well as diversifying their revenue stream, enhancing opportunities for repeat business, and encouraging referrals.

The feedback from OnDeck broker partners is that commercial lending is so much easier and faster than anticipated: loan applications just need several months’ worth of bank statements to be uploaded to the secure OnDeck portal.

Sanz says 70% of brokers are missing opportunities because they aren’t confident about taking on a new stream of business.

“[Prospa’s] simple application processes, fast funding and local BDM support can make it easy to create stickier relationships through diversifying into commercial lending, whilst also providing a potential new income stream,” he says.

Prospa also offers simple and effective marketing that is customised to reflect the broker’s brand, as well as regular educational resources to make things easier and help brokers succeed.

“Our brokers have frequently expressed amazement at the simplicity of SME funding with Prospa. Compared to a home loan, which can take weeks of work to complete, if they choose to, brokers can refer a client to Prospa, get a quick decision, and most of the effort can be completed by Prospa.”

Vala says more residential brokers are stepping into the commercial lending sphere, and Thinktank expects this trend to continue given the benefits that client and income diversification brings.

“By offering an expanded range of products to meet the ever-changing needs of the market, brokers are more likely to retain and increase their value proposition to their client base,” he says.

Diversification also provides brokers with multiple sources of income from different asset classes, strengthening their businesses and capturing additional opportunities across differing economic cycles.

Woszczalski says Grow is experiencing a distinct uptick in new brokers writing commercial finance, and greater deal flow frequency within the Grow network. He shares the following some tips on how brokers new to commercial lending could escalate their diversification into the sector:

- Start with your data: Review your book and identify PAYG vs non-PAYG customers.

- Start communicating: Let non-PAYG customers know you now offer commercial finance that addresses common challenges (ie purchase of advance stock, easing of working capital challenges, or buying a vehicle without a large upfront payment).

- Start scheduling: Create a schedule and stick to it (ie one email per week and two social posts per week).

- Start connecting: Build relationships with lender BDMs to get an understanding of the products/services available to deliver solutions beyond the client’s initial needs. Lean on your aggregator for support.

- Start upskilling: Brokers should actively upskill in commercial finance to enhance their understanding of business needs and funding solutions.

- Start extending your network: Consider aligning with a mentor or an established commercial broker to help guide your transition into commercial finance.

Michie agrees that more mortgage brokers are diversifying into commercial, and this trend is likely to continue as a housing market correction occurs and businesses look to replace government support measures.

“There are around 2.4 million businesses in Australia, the majority being SMEs,” he says. “For brokers prepared to take the time to understand their clients’ needs and advise them in their best interests, there are great opportunities. And with innovations like ScotPac’s Partner Portal available to brokers, diversifying has never been easier.”

Fast, efficient finance

Sanz says that at Prospa brokers can have as little or as much involvement in the application process as they choose. “They always have access to an online dashboard to track application progress and commissions and access our educational and marketing tools.”

He says once leads are submitted, Prospa’s SME lending specialists can provide decisions in less than 24 hours, with approved applicants often funded within 24 hours and commissions paid within the week. He notes that this quick turnaround can help both brokers and their clients.

Vala says there are no minimum volume hurdles or educational requirements for brokers to start dealing with Thinktank. “We make the lending process seamless, with our dedicated team of RMs assisting the broker every step of the way.”

From scenario to settlement, Vala says the broker has the same contact point and advocate for their client’s transaction through the whole credit approval and settlement process. “Not only is this reassuring for the broker and their client; it promotes faster turnaround and approvals.”

Michie says ScotPac recently introduced a “revolutionary” Partner Portal for brokers, providing free access to a range of sales and marketing tools so they can more easily find clients and help them source the right finance solution.

The platform offers smart resources like finance finders to navigate ScotPac’s range of products, and loan calculators to quickly determine a client’s borrowing power.

“Client information can be uploaded very quickly to the portal, so even large and complex transactions can be processed efficiently,” says Michie. “Brokers who register free for ScotPac’s Partner Portal will be giving themselves and their clients a head start.”

Launched in 2021, OnDeck Australia’s KOALA Score™ is an innovative risk-predicting credit model believed to be unique in the Australian market, says Poolman.

Developed in-house by OnDeck’s team of data scientists, KOALA gives OnDeck the ability to analyse a mix of commercial and consumer credit history plus cash flow to build a holistic risk profile.

“This is a plus for newer enterprises, sole traders and partnerships, which typically don’t have the substantial volume of trading data required by traditional lenders,” Poolman says.

“Brokers simply need to upload six months’ worth of a small business’s bank statements to OnDeck’s secure online portal, and a funding decision can be provided in as little as one hour.”

Poolman says the combination of KOALA and Lightning Loans is allowing brokers to meet the funding needs of their small busi-ness faster than ever before.

Verschoor says Grow’s platform uses sophisticated profiling, analysis and AI to allow rapid credit decisioning to assess the applicant in real time.

“In addition, the low-doc product suite allows access to finance with limited supporting documentation,” he says.

Grow encourages brokers to reach out to their local BDMs and discuss their clients’ business needs, says Verschoor.

SME market looking forward

Pressure will remain on retail in the year ahead, says Vala, whereas logistics and other professional services may see an ongoing increase in trade. “This is likely to result in retail clients looking for ways to improve cash flow and take a defensive stance, as opposed to logistics seeking expansion and property acquisition.”

Thinktank expects refinance and equity release activity to continue to increase, as well as the purchase of commercial property in various tax effective structures such as SMSF lending. “Volumes for brokers are likely to increase as the natural market share for brokers diversifying into commercial lending expands,” says Vala.

ScotPac expects the market will grow, Michie says – both the number of businesses accessing finance, and the total value of loans being financed.

Read more: SME confidence showing green shoots

This is because businesses that had government support during COVID now require alternative capital, he says. Secondly, businesses that took a cautious approach during pandemic disruptions have now resumed activities that require working capital, including asset purchases and digital upgrades.

“Third, there is a growing awareness of the benefits of working capital to support growth through M&A activity. So the market SME finance outlook is healthy and exciting,” says Michie.

Wozsczalski says there is sustained demand for alternative working capital products to boost growth – particularly asset finance (new and used), invoice finance, and trade finance facilities to offset supply chain disruption.

“Capital-intensive businesses that require a large pool of assets or stock to operate are benefiting from multiple finance facilities to secure and procure stock, including bulk purchases,” he says.

“In the next six to 12 months, we expect strong demand for working capital as many businesses continue to thrive off the back of lockdown. We anticipate that this will correlate with an increase in demand for asset finance and working capital solutions.”

Sanz says trends in borrowing continue to follow market sentiment, with Prospa’s latest research showing that seven in 10 business owners and leaders rated their business’s overall health as good or very good. One in four business owners also expected to access external funds.

“Prospa’s loan originations accelerated to record levels in FY22,” Sanz adds, “and that growth looks set to continue into FY23, with July originations 58% higher than July 2021.”