Industrial sector leads gains as confidence eases on interest rate uncertainty

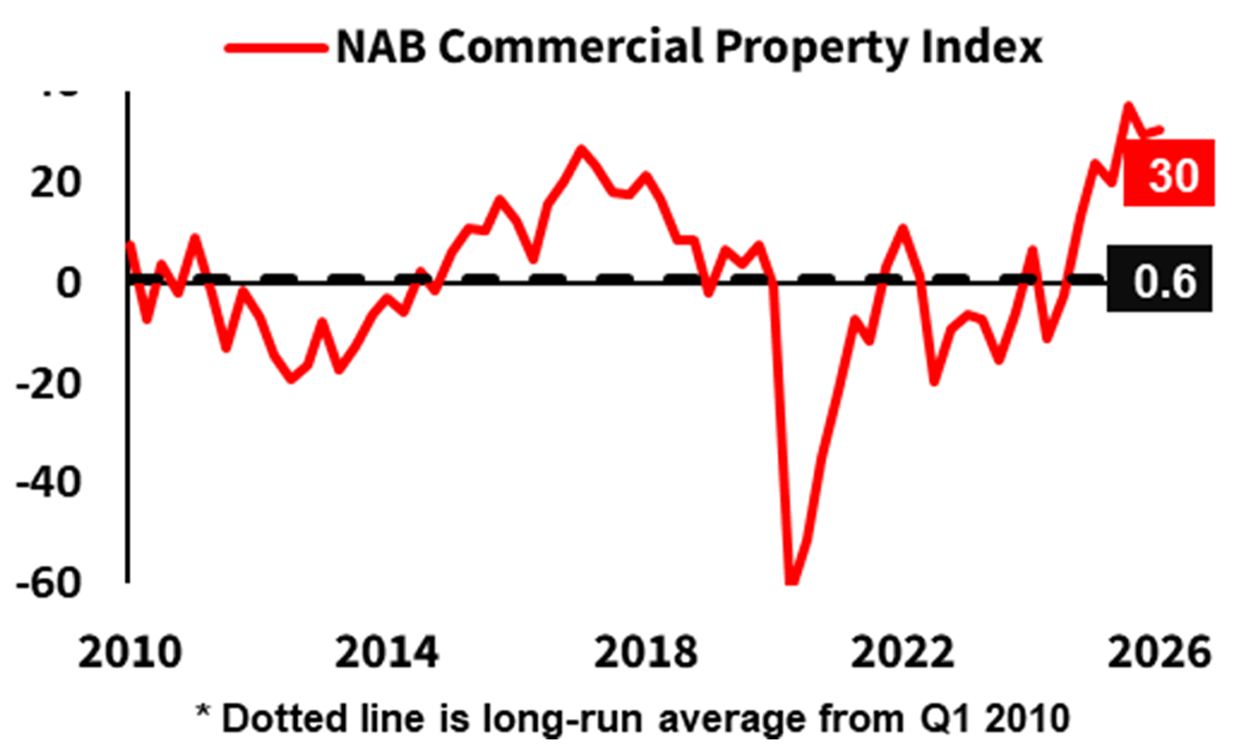

Australia's commercial property market posted a modest lift in overall sentiment during the March 2026 quarter, though confidence over the year ahead softened, according to the NAB Commercial Property Survey for Q1 2026.

The NAB Commercial Property Index rose one point to +30 in the March quarter, two points below the series peak recorded in September 2025, pointing to resilient conditions across the sector before the outbreak of the conflict in the Middle East.

The 12-month confidence measure fell to +39 from +46 in the December quarter, while the two-year outlook dropped 13 points to +45.

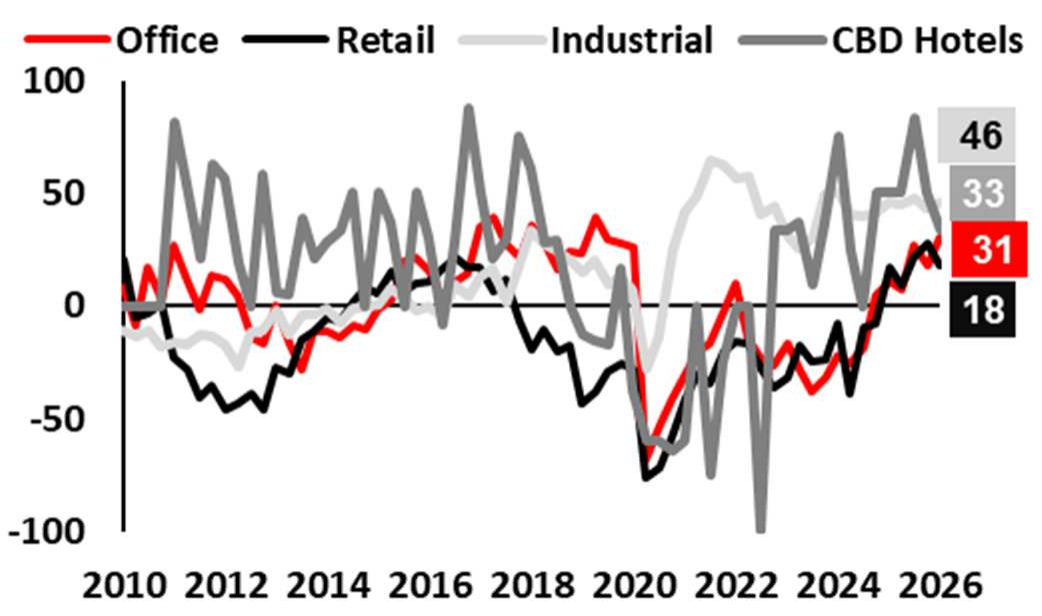

Industrial property remained the highest-rated sector, with the current index rising to +46, followed by CBD hotels (+33), office (+31) and retail (+18). Office sentiment improved notably from +18 in the December quarter, while retail slipped from +28. Industrial property leads confidence over both the 12-month (+58) and two-year (+64) horizons.

"The survey showed sentiment held up, with the overall index close to its recent peak," said Brien McDonald, senior economist at NAB. "Industrial remained the standout, while office improved and retail eased.

"Confidence moderated from very elevated levels as respondents reassessed the path for interest rates, but expectations were still positive over the next 12 months and two years."

Commercial Property Index by Sector

By state, Queensland led the overall commercial property index at +55, ahead of New South Wales (+34) and South Australia/Northern Territory (+44). Victoria improved to a neutral reading of zero, up from -8 in December, driven in part by a less negative assessment of the office market (-9, from -31). Western Australia fell to +22 from +32.

Queensland also led the office sub-index at +69, while WA remained the weakest at -10 — unchanged from the prior quarter and negative across all time horizons measured. For industrial property, Queensland recorded a reading of +88, with SA&NT next at +75.

On capital values, industrial property is expected to grow 2.1% over the next 12 months nationally, with Queensland projections at +6.5%. Office capital values were flat on average, with Queensland again the standout at +3% and WA the weakest at -3.4%. Retail capital values are expected to fall 1.0% nationally over the same period, with all states negative except WA (+1.7%).

Rental growth expectations were strongest for industrial property, with 2.9% forecast over the next year and 3.3% over two years. Queensland led the industrial rental outlook at 5.3% for 12 months, and WA at 5.4% over two years.

Office rents are expected to grow 2.9% nationally over the next 12 months and 3.1% over two years, with Queensland again topping state-level forecasts at 4.7% and 5.3% respectively. Retail rent growth expectations were more subdued at 1.1% for 12 months and 1.5% over two years.

The national office vacancy rate tightened slightly to 11.1% from 11.7% in December. Rates ranged from 9.3% in Queensland to 12.6% in WA. Survey respondents expect the national rate to ease further to 10.5% in 12 months and 9.4% in two years. Victoria was the exception, with its vacancy rate rising to 12.5% from 10.4%.

Retail vacancy edged up to 6.2% from 6.1%, marginally above the long-run average of 5.9%. Industrial vacancy widened to 3.8% from 3.3%, with rates ranging from 1.7% in WA to 4.4% in Queensland.

Developer commencement intentions for the next six months fell back to approximately the survey average at 47%. Residential projects were the most commonly cited target (61%, up from 49% in Q4), followed by industrial (24%, up from 20%). Office and retail each attracted just 4% of planned commencements. Land-banked stock remained the primary source of development activity at 74%, with new acquisitions cited by 34% of respondents.

Access to debt funding remained slightly constrained, with a net -10% of respondents reporting tighter conditions, a modest deterioration from -8% in Q4. The outlook for debt funding over the next three to six months was also more negative at -8%, compared with a neutral reading the previous quarter. Equity funding conditions similarly tightened, with a net -9% reporting greater difficulty, compared with -3% in Q4.

Pre-commitment requirements for new developments edged higher for residential projects (53.4%, from 52.6%) but fell slightly for commercial (55.2%, from 55.6%).

"The Q1 survey suggests the sector entered the period in a relatively resilient position, before the conflict in the Middle East escalated," McDonald said. "Sentiment remained, but confidence was already cooling and funding conditions were still reported as tight, so it will be interesting to see how this plays out in Q2."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.