By using data from comprehensive credit reporting, Pepper Money is able to personalise its service for customers

MPA: We’ve been hearing about comprehensive credit reporting for a while now, but can you explain a bit about what it means for those who are still unsure?

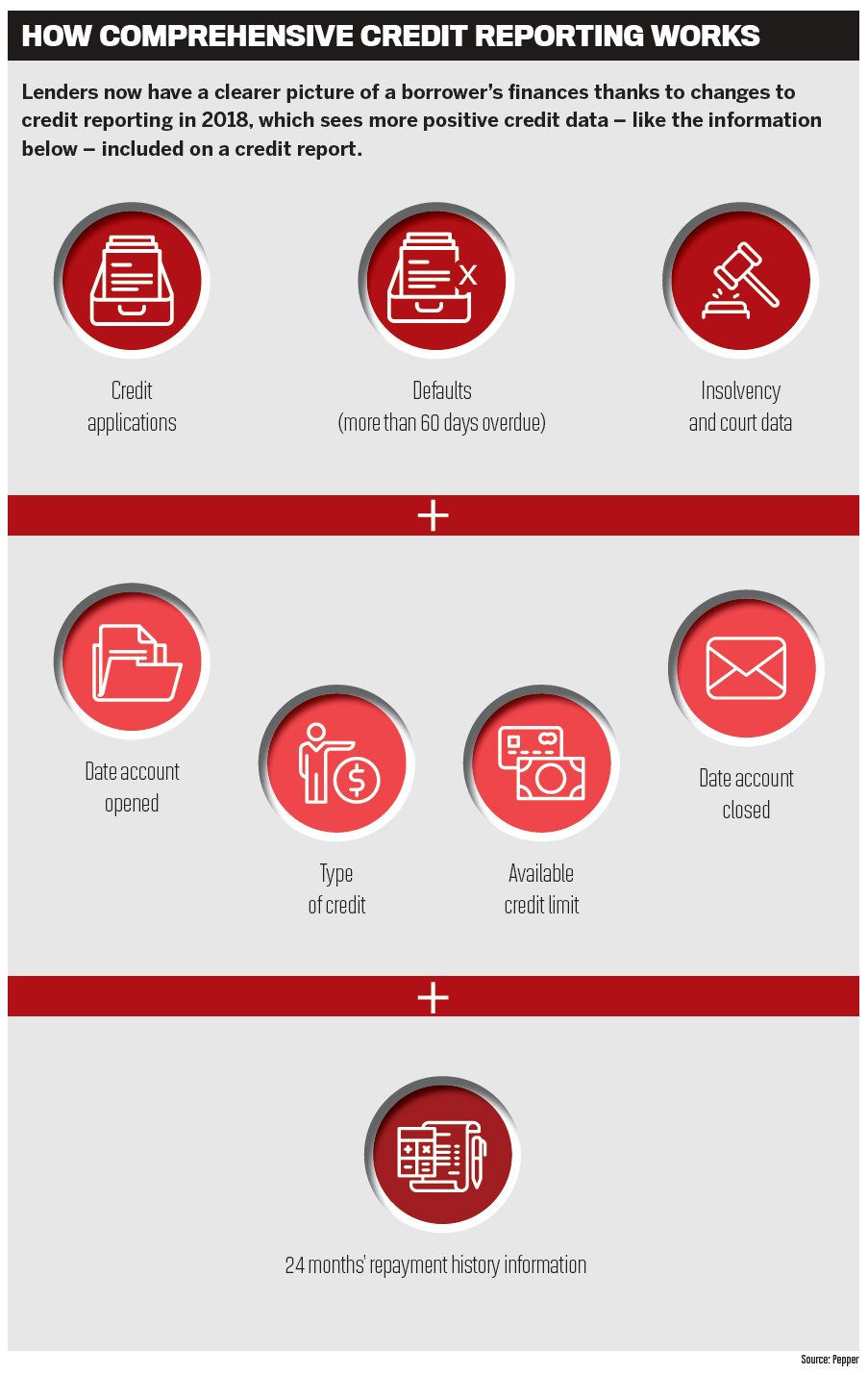

Neil Culkin, Pepper Money: Credit reports contain information that helps lenders like Pepper Money assess the risk of lending money to customers. In the past, a customer’s credit report mainly showed ‘poor’ credit behaviour, such as the number of times they had applied for credit, had been declared bankrupt or had defaulted on prior loans.

Comprehensive credit reporting (CCR) or ‘positive reporting’ provides additional information on loans that the applicant has, or had, and the actual repayment histories of those loans. This information now demonstrates ‘good’ and ‘bad’ credit behaviour on a customer’s credit report. This new information makes it easier for some people – or for others, harder – to obtain credit or a loan. It allows lenders to lend more responsibly and helps credit assessors make more informed decisions.

Under CCR, all the ‘negative’ behaviour remains on the report; in addition, any information about the credit accounts that the customer has taken out, including the date the account was opened, the type of credit, the available credit limit and the date the account was closed. This information stays on the report while the account is open and for 24 months after it is closed.

This new information will contribute to the customer’s credit score, improving for those who may have been diligently paying off existing debts. Conversely, a customer’s credit score may be negatively impacted where they may have missed payments.

The result is that some customers who were previously considered prime loan customers may now not qualify because the lender can see new information such as a poorrepayment history on existing loans.

Customers who were not considered prime customers before may now be able to take out credit at a better interest rate.

Pepper Money supports positive credit reporting because it makes it fairer for the customer and reduces effort for the broker. The customer’s credit score is based on their actual and recent payment history and existing credit arrangements rather than whether they have had a default in the past.

As more lenders join the regime, through choice or via regulation, more customers’ credit history becomes available, simplifying the lending process for everyone.

MPA: Where are we at with CCR at this point in the timeline?

NC: Currently, there are about 50 lenders participating in CCR. Pepper Money began participating in the regime two years ago as an early adopter of CCR, not just in the non-bank space but across the lending industry.

We’ve always been in the business of pricing for risk. We look more deeply into a customer’s circumstances than the banks, with a view to understanding their situation. Treating people fairly and finding loan solutions that work for them is what we are all about.

We see CCR as a more evidence-based formalisation of our existing assessment processes. Where other lenders may use this data solely to determine an outcome, at Pepper Money it provides our credit assessors with a broader, more accurate picture of the applicant’s financial position. Essentially, it allows us to accurately and efficiently determine which Pepper Money product the customer would be eligible for.

MPA: What benefits can Pepper Money provide as part of the regime?

NC: Having been in the regime for two years now, we’ve been able to fully incorporate CCR into our credit decisioning processes in a way that supports our commitment to reasonable turnaround times and leads to less effort for brokers and their customers.

Taking it one step further, Pepper Money is now relying on the CCR repayment history information [RHI] data for credit assessment purposes. This means we will no longer need to collect loan statements up front to refi nance a home or consumer loan where a customer’s current lender is participating in CCR, and data is available.

Simply by automating certain steps that require a customer’s RHI makes the application submission and credit assessment process more e cient. For instance, a broker and customer will no longer need to provide, nor will Pepper Money’s credit team have to manually review, up to 18 pages of loan statements to assess loan conduct on a typical debt consolidation home loan application.

MPA: How will CCR make a difference for customers?

NC: I see it as a real benefit for customers. By doing away with the need for loan statements on a refinancing application, we are making it easier for customers to get their desired outcome faster, and at the same time saving them time and perhaps money.

As long as their current lender is part of the CCR regime, they won’t have to go to the extra effort to supply piles of loan statements. The information will already be available to Pepper Money when we start to assess the application.

MPA: How will it make a difference for brokers?

NC: The good news is that mortgage brokers benefit too. If a customer already knows their credit score before meeting their broker, it potentially makes positioning a non-conforming loan with the customer an easier conversation to have. Using their score as evidence may help them understand why they’re not going to be able to get the interest rate they’ve seen advertised on TV, and will allow the broker to identify a more appropriate lender for them, given their credit report.

Happily, it can also mean a broker might be able to offer a customer a better outcome too, if their score is better than expected.

Another benefit is that brokers will no longer have to chase up outstanding loan statements from their customers if we can rely on CCR for that information, making the whole transaction more efficient.

When it comes to dealing with Pepper Money, we are optimising how we use CCR data for loan applications and assessments. It’s all part of improving our digital journey and making it easier to refinance a home loan with Pepper Money.

Tools such as the Pepper Product Selector can simplify the identification and research process for brokers. By providing access to a customer’s credit score and other bureau data, including repayment history information, a broker will see what we, as credit assessors, see, allowing them to have a deeper discussion about their client’s real-life situation. Brokers can make a lender recommendation with confidence, knowing there is a viable solution to offer their customer. Better still, it’s at no cost to the borrower and takes less than two minutes.

MPA: What else do brokers and borrowers need to know about Pepper Money and CCR?

NC: The broker has a really important role to play in helping the customer to understand the implications that their credit report – both positive and negative – can play in getting them a loan. Websites like www.creditsmart.com.au are dedicated to educating the general public about comprehensive credit reporting, and brokers can recommend that customers visit the site, or refer to it in their customer communications.

Ideally, understanding the implications of CCR will happen before the customer has started the purchasing process, but if it hasn’t, and the customer chooses not to proceed with a loan because of their credit score, the broker can provide them with some tangible ways to improve their credit score, which could lead to repeat business in future.

Tips like pay your bills on time, automate payments if possible, close unused credit facilities and regularly check your credit score for any anomalies are all simple, yet valuable advice that a broker can provide today and see the customer in a position to buy their home sooner, without resorting to expensive credit repair companies.