Expert advice: Keep it on your 'to do' list for 2024

Despite a substantial number of mortgages refinanced since rate hikes began, many could still benefit from switching lenders to secure more competitive rates, according to RateCity.com.au research director Sally Tindall (pictured).

Tindall, commenting on the latest ABS lending indicator data, emphasised the importance of considering refinancing to exert pressure on banks for better rates.

“The latest ABS data shows a total of 756,395 mortgages have been refinanced since the start of the hikes. That’s an impressive figure, but it does mean there are still hundreds of thousands of mortgages, if not millions, that could potentially benefit from switching lenders,” she said.

“While we know many of these borrowers have negotiated directly with their lenders, refinancing is what really puts pressure on the banks to cough up competitive rates, so if you haven’t made the switch, keep it on your ‘to do’ list for 2024.”

Tindall also pointed out the decrease in the number of owner-occupier loans approved in January, which stood at 8,707 in seasonally adjusted terms. This figure, she said, suggests that many potential buyers are still struggling to enter the market, underscoring the need for additional support mechanisms beyond the government’s Help to Buy scheme.

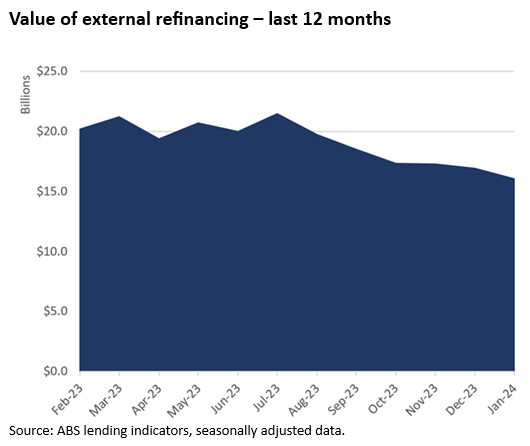

ABS reported that the value of refinanced mortgages fell for the sixth consecutive month to $16.07 billion in January. Despite being significantly above pre-pandemic levels, this figure represents a 25% decrease from the peak recorded six months prior.

January also witnessed a decrease in the value of new home loans, dropping $1.02 billion (-3.9%) from December. This followed a larger fall in December of $1.13 billion (-4.1%). The decline suggests a potential slowdown in the market, although new lending remains substantially higher than the previous year, especially in investor lending which saw an 18.5% increase in January 2024 compared to January 2023.

The share of new and refinanced loans choosing a fixed rate also increased for the second month in a row. However, with only 2.3% of these loans opting for a fixed rate, the preference remains significantly lower than in July 2021, when 46% chose fixed rates.

One silver lining, according to Tindall, was that the average new loan size for owner-occupiers broadly went down, rather than up in most states and territories, with the exception of South Australia, Western Australia and Victoria.

“That said, property prices across the country, for many first home buyers, are just too high, particularly in the face of rising rates and rising rents,” she said.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.