The second phase of the Consumer Data Right was rolled out in November, meaning the big four banks are sharing their mortgage and personal loan data – but what does that mean for brokers?

With mortgage data now being shared by the big four banks as part of the second phase of open banking, a new report has revealed that 76% of mortgage brokers do not intend to actually use the data.

The Consumer Data Right was officially launched on 1 July, when the big four banks began to share current and savings account data. As of 1 November, this was widened to include data on mortgage and personal loans.

As we move into this next phase, The State of Open Banking in Australia, a report by technology providers NextGen.Net and Frollo, looks at what the financial sector thinks of the new banking regime, where it is headed and what the most immediate challenges and opportunities are for businesses.

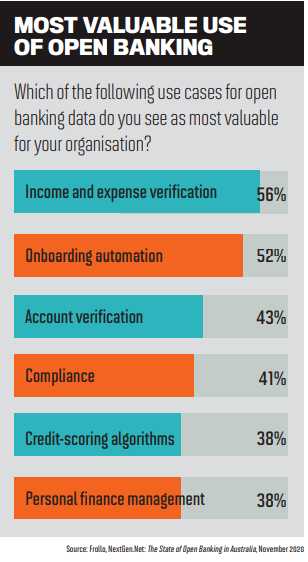

Based on interviews with industry leaders and a survey of 161 finance and broking professionals across Australia’s financial sector, the report highlights that most of the industry sees open banking’s ability to streamline the lending process through income and expense verification as its most popular use case.

More than 70% of industry respondents intend to use CDR data, with almost 58% stating that they intend to use it within the next 12 months – but this is not the case for mortgage brokers.

Streamlining the application process NextGen.Net chief customer officer Tony Carn said awareness of the CDR’s potential for players beyond the big four and other current and soon-to-be-accredited data recipients (ADRs) was low. According to the report, awareness among the broking community was 25% lower than the report average.

“Brokers fall into the same category as consumers in this regard, as we’re still in the early stages of rollout,” Carn said. “However, now that mortgages are part of the open banking ecosystem, I believe the broking sector will start to take note of its potential, especially as ADRs start to bring their openbanking-powered solutions to market.”

“There are more opportunities for banks, lenders and fintechs to build innovative propositions for consumers. This in turn will drive competition” Gareth Gumbley, Frollo

Carn explained that there were a number of different ways brokers would benefit from the proposed open banking regime changes. He said streamlining and digitising the loan application process would reduce the amount of paper used for verification and validation, save time for both brokers and lenders, and ultimately deliver a better experience for borrowers.

“This will then translate into a reduction in the amount of times a lender comes back with more/missing information requests, significantly reducing friction from the whole home loan process,” he said.

“The broader benefit for brokers is to leverage the opportunity to nurture their customers earlier and for longer and hold their hand to get them to the home loan application stage. Helping a customer get ‘fit for finance’ and ‘approval ready’ will enable brokers to deliver holistic lifetime value to their customers – way beyond just the home loan application.”

According to the report, the biggest challenges for brokers are to gain clarity around the CDR rules, and the need for customer education.

Carn said that outside of understanding the government’s stance on a broker’s role in the CDR ecosystem, once ADRs built the tools it would be easier to understand.

“At the moment, we’re all at the point of now being able to directly share and access consumer banking data with ADRs – and that’s great,” he said.

“But it’s what brokers and aggregators can do with that data that will really bring to life the promise and significance of CDR for the broker sector, and that’s what I’m most excited about.

“Now that mortgages are part of the open banking ecosystem, I believe the broking sector will start to take note of its potential” Tony Carn, NextGen.Net

Better solutions for borrowers

Finance management fintech Frollo invested in open banking before the company even began. It offers two distinct services using CDR data: its consumer app giving consumers an overview of their financial accounts, and an ‘outsourced ADR’ solution for businesses that want to use the data to compete.

“The additional products in the November scope make CDR much more interesting for lenders who use our outsourced ADR solution, as it provides them with a more complete financial picture to make credit decisions,” said Frollo founder and CEO Gareth Gumbley.

While the report shows that around a third of the industry is undecided as to whether open banking will create trust in the financial system or a level playing field in banking, Gumbley said it would mean good outcomes for consumers.

“Under the Consumer Data Right, consumers have more control over their financial data and who they choose to share it with,” he said.

“This means there are more opportunities for banks, lenders and fintechs to build innovative propositions for consumers. This in turn will drive competition and ultimately a better deal for consumers.”

The majority of respondents believed it would take around three to five years for Australians to begin using open banking, but Carn said that did not mean it was not exciting. “I think people tend to underestimate what can be done in three to five years,” he said. “Just look at the level of digital adoption that took place across the sector during COVID-19 lockdowns.

“From a NextGen perspective, we clearly see the potential that open banking has to revolutionise the way Australians engage with their finances. And we believe that those who’ll win in this new era of banking are those that assess their readiness, choose the right partners, move early to embrace this new technology, and really understand how it can transform the way they engage with their customers.”