Social media and AI cited as key drivers of growing mortgage knowledge gap

More than half (58%) of Australian homeowners do not fully understand key home loan terms, according to new research from financial comparison platform Money.com.au.

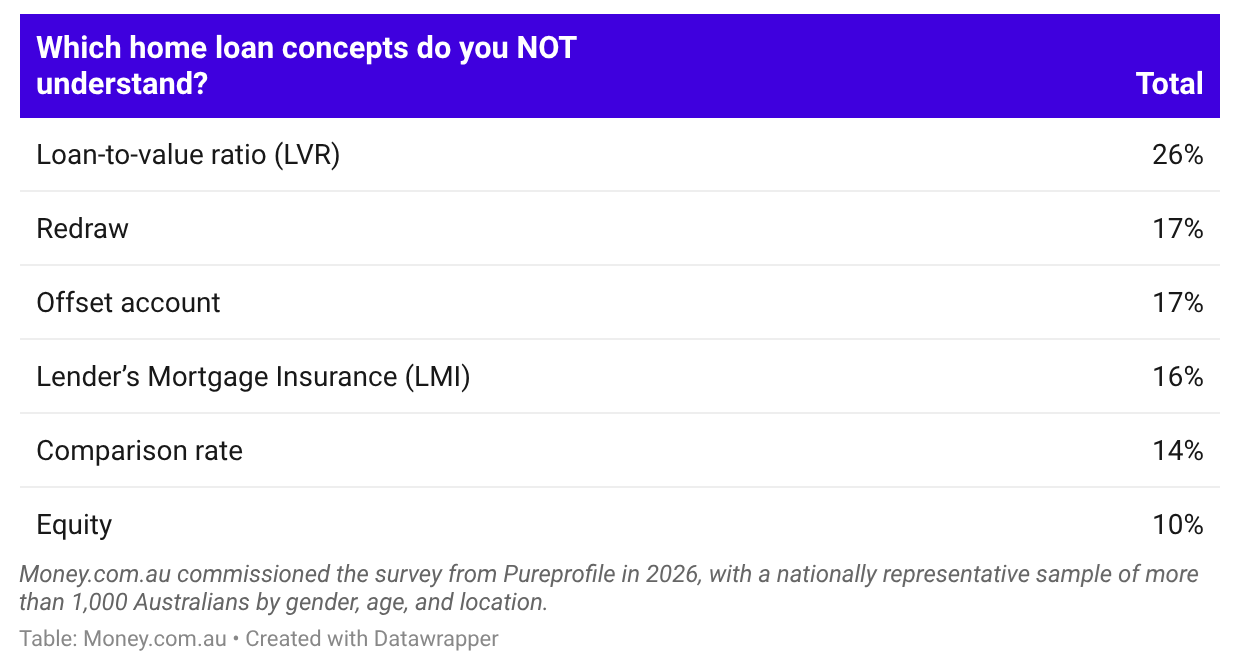

The survey, drawing on a nationally representative sample of more than 1,000 Australians, found loan-to-value ratio (LVR) to be the most poorly understood concept, with 26% of homeowners reporting they do not grasp how it works. LVR influences a borrower's loan eligibility, applicable interest rate, and whether Lender's Mortgage Insurance (LMI) is required.

Redraw facilities and offset accounts were the next most misunderstood features, with 17% of respondents unsure how each operates. LMI followed at 16%, comparison rates at 14%, and equity at 10%.

Confusion was broadly consistent across age groups. Gen Z and Millennials recorded the highest rates of uncertainty at 61% each, followed by Baby Boomers at 59% and Gen X at 58%.

Money.com.au's mortgage expert, Nick Burgess (pictured right), linked the knowledge gap to growing reliance on social media and AI-generated content for financial guidance.

Money.com.au's mortgage expert, Nick Burgess (pictured right), linked the knowledge gap to growing reliance on social media and AI-generated content for financial guidance.

"If you don't have a firm grasp on basic mortgage terms and features, you're likely not maximising your loan's potential and could end up paying more interest over the loan's life or dragging out your mortgage for longer than you need to," Burgess said.

"Too many borrowers are graduating from what I'd call the Facebook and AI university. They rely on generic online information to understand how a mortgage works, as well as social media opinions. Also, one in five Aussies say they trust AI tools like ChatGPT for home loan information, so the risk of misinformation is getting out of hand."

Burgess said the consequences of poor mortgage literacy are tangible. "I had a first-home buyer who got into the market in Sydney with a 5% deposit try to refinance a year later without realising their LVR was still above 80%, which would have meant paying LMI all over again," he related.

"I also had a middle-aged couple with kids and $200,000 sitting in a regular savings account instead of their offset account because they assumed the offset was just another transaction account. No one had properly explained to them that every dollar sitting in an offset works dollar-for-dollar to reduce the amount of interest charged on their home loan."

"I've also seen borrowers take out personal loans for major expenses like buying a car or renovating part of their home because they didn't know they could use the equity they'd already built up in their property to finance those costs at a much lower interest rate."

Burgess urged borrowers to seek professional guidance rather than relying on unverified sources. "Your mortgage is likely the biggest debt you'll ever take on, so it pays to understand key concepts like LVR, how the comparison rate differs from the advertised rate, and the difference between an offset account and a redraw facility," he said. "If you're unsure about anything, don't be afraid to ask your lender or broker to break it down for you."

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.