A sober reminder amid negative gearing overhaul: Property is a low-yielding investment

Finding a positive cashflow investment property has become a "needle in a haystack" task for buyers, with a mere 0.8% of Australian suburbs currently delivering positive returns despite a recent nationwide uptick in gross rental yields, according to new data from Cotality.

Research from the property data and analytics firm identifies only 38 suburbs across the country where investors can expect net positive monthly cashflow, based on assumptions of a 20% deposit, a 30-year principal and interest mortgage at 6.34% — the current market average for new investor loans — and holding costs equivalent to 2.5% of the median property value.

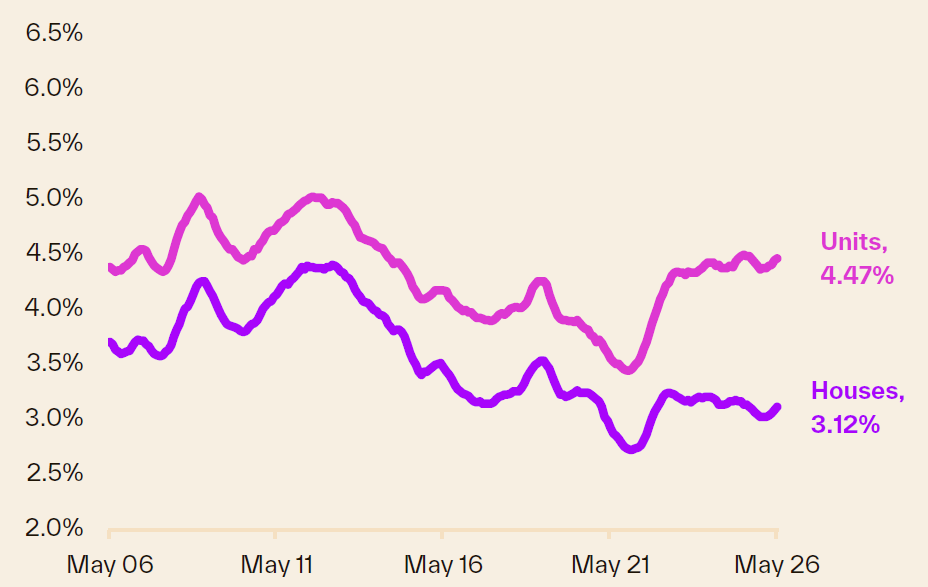

Australian housing remains a low-yielding asset class for investors. Across the combined capitals, the gross rental yield stood at 3.45% in May 2026 — 3.12% for houses and 4.47% for units.

Of the 38 suburbs identified as cashflow positive, 69% are located in regional Western Australia, predominantly in Pilbara mining towns such as Pegs Creek, South Hedland, and Newman. A further 10% are in regional Queensland, concentrated in Bowen Basin coal mining areas. Only two capital city suburbs made the list: Carlton in Melbourne for units and Berrimah in Darwin for houses.

Gross rental yields, combined capitals  Source: Cotality

Source: Cotality

The highest estimated monthly cashflow was recorded in Pegs Creek (WA) for units at $2,088, followed by South Hedland units at $1,626 and Bulgarra units at $1,370. Gross rental yields in these markets ranged from approximately 8% to as high as 15.5% in South Hedland.

"Gross yields tend to be higher in more volatile or riskier markets," said Tim Lawless (pictured right), research director at Cotality. "For example, gross yields in Darwin are significantly higher than in the other capitals, but this market has also shown significant volatility in housing cycles."

"Gross yields tend to be higher in more volatile or riskier markets," said Tim Lawless (pictured right), research director at Cotality. "For example, gross yields in Darwin are significantly higher than in the other capitals, but this market has also shown significant volatility in housing cycles."

The landscape for yields is shifting, driven partly by federal Budget changes to negative gearing on established homes. With investors facing reduced ability to offset rental losses against taxable income, rental income has taken on greater importance in investment decisions. Lenders are also factoring in reduced borrowing capacity for investors and higher holding costs.

Rental vacancy rates remain at historically tight levels, recorded at 1.5% nationally in May 2026, while rental growth has re-accelerated to 5.9% per annum. The combination of softening property values in some markets and rising rents is beginning to push gross yields higher, particularly in Melbourne, where yields have moved from near the bottom of the capital city rankings to the middle of the pack for houses and third highest for units.

However, yield compression persists in markets where values are still rising. Gross rental yields were at record lows in Brisbane and Adelaide for both houses and units, and for Perth houses, in May 2026.

Even under a relatively optimistic scenario, the yield uplift remains limited. "Under a scenario where capital city home values fell by 10% and rents rose by 10%, the gross rental yield would only rise by approximately 82 basis points, from 3.45% to 4.27%, which is still a long way off a positive cashflow scenario after allowing for costs," Lawless said.

Mortgage costs represent the largest component of holding expenses, accounting for around 71% of total costs under the assumptions modelled. Investors with greater equity or larger initial deposits would face lower sensitivity to interest rate movements and would be better placed to achieve a positive net yield.

Historically, Australian property investors have prioritised capital growth over rental income. In the most recent growth cycle, investor activity approached record highs, comprising 41% of mortgage demand, even as yields were low and declining. The federal budget changes are expected to reorient investor focus toward income-generating assets, though the data suggests genuinely positive cashflow properties remain exceptionally scarce.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.