A number of factors will protect property values, says CoreLogic

CoreLogic said its 2023 outlook for the Australian unit market “remains skewed to the negative” as economic conditions remain on a downturn.

The report cited cumulative rate rises having now risen above the 300-basis point serviceability buffer that was used to assess recent borrowers, along with the upcoming expiration of a large portion of fixed-term loans throughout the year, which would bring borrowers from fixed-term rates of around 2% to over 5%.

Interest rates are also expected to continue rising throughout 2023, bringing added pressure to “a growing number of households,” the report added.

Despite these challenges, CoreLogic economist Kaytlin Ezzy (pictured above) said the market should still see tailwinds shielding unit values from “the worst of the current downturn.” These would include relative affordability, low supply levels, and the return of investors, who typically preferred the medium to high-density sector.

The CoreLogic Australian unit market update for January 2023 described the unit market’s 2022 trajectory as a “two-part performance” that began with “an easing in the monthly growth rate” during the first four months of 2022, followed by increasing interest rates, low consumer confidence and persistently high inflation that plunged values -5.2% below the peak reported in April.

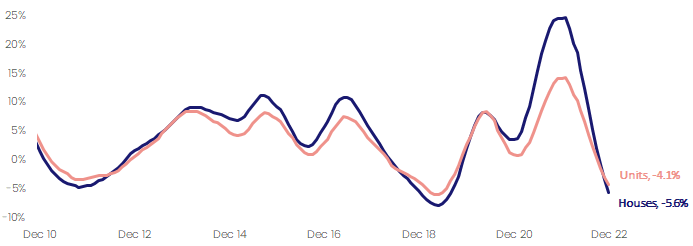

According to Ezzy, the downturn from May to December sliced about -$73,000 off the average Australian house value, versus the -$32,400 decline seen in the average national unit value.

“Historically, house values have been more volatile than units, recording larger gains through the upswing and larger depreciation during a downswing,” Ezzy said. “The current cycle has been no different.”

Ezzy said the resilience of the unit market has become evident as the downturn matures, “with the annual performance gap between house and unit values inverting for the first time since May 2020 in November (-50 basis points) and widening further in December (-150 basis points)”.

“This is in stark contrast to September 2021, when the annual performance gap between houses and units peaked at 10.9 percentage points,” she added.

Rolling annual growth rate, National houses and units

Source: CoreLogic

CoreLogic pointed to affordability as the “leading factor protecting unit values from steeper declines,” with the median value for national units being approximately $170,000 cheaper than the average house. Across combined capitals, this gap is even wider, at around $247,000.

“With eight consecutive rate rises reducing the average borrowing capacity by around 13.3%1, it's likely a number of prospective buyers can no longer borrow the amount required to purchase a house and are instead looking towards the unit market as a more affordable option,” said Ezzy.

While unit values were supported by their relative affordability, consecutive rate hikes still caused the overall affordability of units to decline, with previous CoreLogic research showing that the portion of the average household income required to service a unit mortgage had jumped to 35.8% in September 2022 from 30% in the previous year.

“Mortgage serviceability has likely continued to erode with further rate rises in October, November and December, taking the cash rate 300 basis points above the emergency lows in April,” said Ezzy.

“Assuming the November and December rises are passed on in full, the monthly mortgage repayment on a typical unit will have increased by $614, despite the mortgage principle decreasing by approximately $26,000.”

For the NSW unit market, the introduction of a land tax option for first-home buyers is another “potential tailwind”.

"It's not uncommon for many first home buyers to postpone looking for a property until they can afford a home that will meet their medium to long-term needs, rather than purchase a more affordable unit that would meet their short-term needs,” said Ezzy.

“As one of the largest transaction costs, stamp duty is a significant factor contributing to the cost of entering the housing market.”