Higher rates and weaker demand weigh on capital city values

Australia’s housing market is showing signs of moving into a downturn as higher interest rates, weaker borrowing power and affordability pressure reduce buyer demand.

According to Cotality’s latest Housing Chart Pack, market conditions were softening after a strong growth cycle that has left many homeowners with a substantial equity buffer.

The property data firm’s Home Value Index analysis found that Australia’s combined capital city markets have recorded 10 downturns of at least three months over the past four decades.

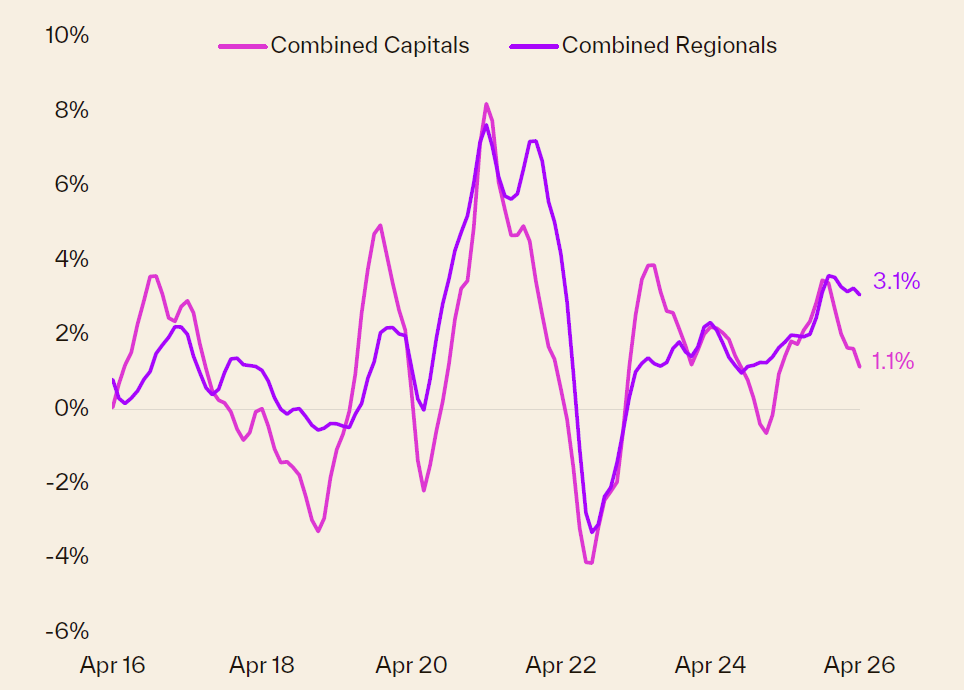

Rolling quarterly change in dwelling values Source: Cotality

Source: Cotality

Tim Lawless (pictured right), research director at Cotality, said past housing declines had been driven by several factors, including global shocks, rate rises, tighter credit, fiscal policy changes, affordability constraints and shifts in sentiment.

Tim Lawless (pictured right), research director at Cotality, said past housing declines had been driven by several factors, including global shocks, rate rises, tighter credit, fiscal policy changes, affordability constraints and shifts in sentiment.

“Sydney and Melbourne are already five months into the early phases of decline, while growth is slowing across the mid-sized capitals,” Lawless said. “Listings are picking up as demand softens, interest rates are rising while affordability and serviceability pressures are biting.”

Capital city home values rose by just 0.2% in April, with momentum continuing to weaken. Lawless said Cotality’s combined capitals index could move into negative territory in coming months if the current trend continues.

“This trend has been amplified by seventy-five basis points of rate hikes so far this year and the chance of another hike, or hikes, later in the year,” Lawless said.

“Importantly, the market was already slowing well before the hiking cycle commenced, highlighting the downside impact of waning confidence from late last year alongside rising inflation and worsening levels of housing affordability.”

The steepest combined capital city fall in the past 40 years occurred from 2017 to 2019, when values dropped 8.2% over 19 months. That decline followed a strong upswing and the introduction of stricter lending rules after the Royal Commission into the banking and finance industry.

A more recent downturn took place in 2022–23, when values fell 8.1% over nine months as interest rates climbed rapidly from pandemic-era lows.

Cotality said the current slowdown follows a period of large gains, meaning most existing owners remain in a sound equity position. The Reserve Bank has estimated that fewer than 1% of households were in negative equity at the start of the year.

The combined capitals Home Value Index has increased 33.7% over the past five years. Perth, Brisbane and Adelaide recorded gains of about 80% to 90% over the same period.

“Historically, housing downturns have been relatively short-lived, with all but three capital city downturns over the past 40 years lasting less than 12 months, although the length and magnitude have varied from city to city,” Lawless explained.

“For example, post mining boom, the Perth market navigated a 61-month downturn where values fell 15.3% from peak to trough. Darwin saw an even longer downturn with values falling over 69 months from mid-2014.”

Supply conditions, which have supported prices in recent years, are also easing. Cotality said this reflected softer demand and higher advertised stock, rather than a sharp increase in new listings.

In the four weeks to early May, 39,319 properties were added to the market nationally. That was 4.7% above the five-year average. Total advertised stock remains low across the country, but it is rising and is now above average in Sydney, Melbourne and Canberra.

Despite the weaker market, Cotality said a significant rise in distressed sales or mortgage arrears was unlikely. Mortgage arrears were about 1.45% at the end of last year, below the 1.69% peak recorded when interest rates were at similar levels in mid-2024.

“An expectation that labour markets will remain tight, as well as a history of stringent prudential standards, including the three percentage point mortgage serviceability buffer, should help to keep mortgage arrears low as interest rates rise,” Lawless said.

Recent purchasers may face greater negative equity risk if values fall, particularly borrowers who bought with smaller deposits. This includes some participants in the government’s 5% Deposit Scheme.

“Recent buyers are arguably at more risk of seeing negative equity, given they have had less time to accrue value in their property or pay down the principal of their loan,” Lawless said.

“However, mortgage repayments are typically prioritised, with borrowers more likely to adjust spending elsewhere before missing a payment,” said Tim Lawless, research director at Cotality.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.