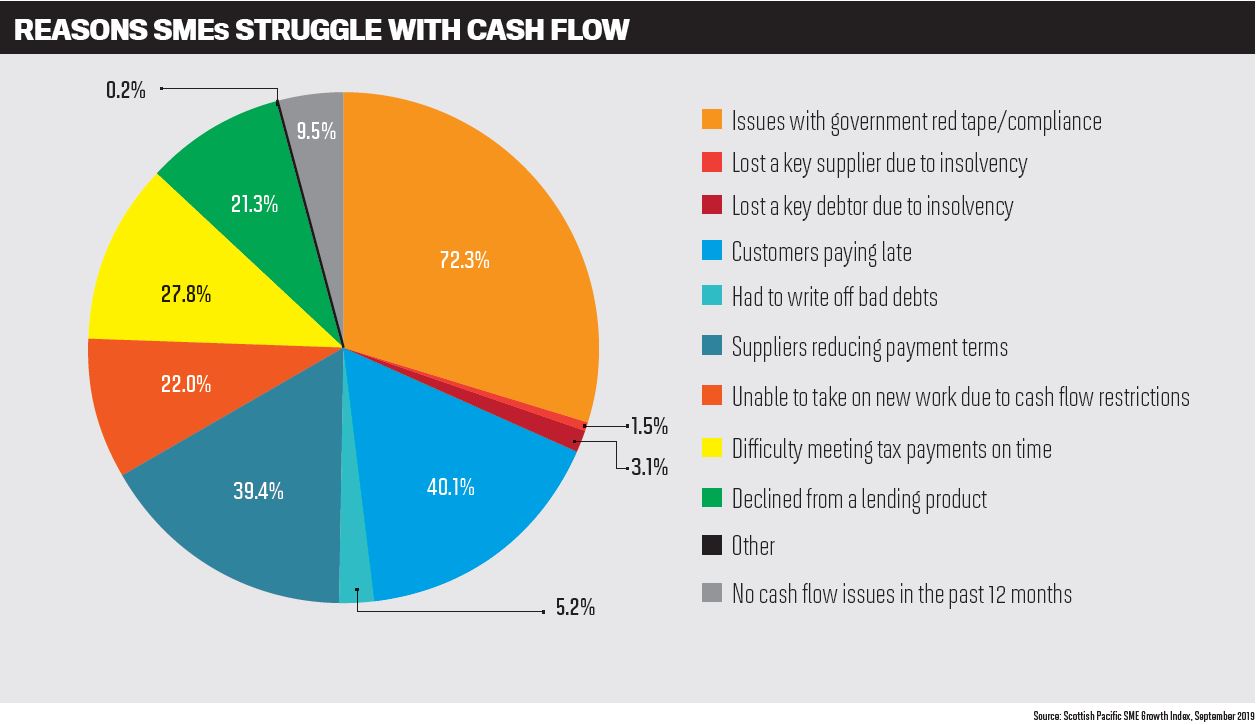

Businesses are more likely to be struggling with their cash flow during the COVID-19 crisis

'CASH IS KING!'

While this expression is thrown around all too often, for small businesses staring into the challenges of 2020, it is a very real truth they are having to face.

According to research by Scottish Pacific and East and Partners, the average time that SMEs wait to be paid is 56 days, and smaller businesses tend to wait longer than the larger ones.

“Money that could be used to expand revenue and invest in growth is being tied up for too long, as SMEs struggle to be paid within a reasonable time frame,” says Scottish Pacific CEO Peter Langham.

On average, the lender found that SMEs have almost a third of their revenue tied up in outstanding invoices, with 16% locked into those outstanding for more than 90 days.

Langham says the research highlights the importance of businesses finding the right funding to unlock working capital, and this is where debtor or invoice finance comes in.

Working much like an overdraft or line of credit that is not secured against the family home but against the money a business is owed, it generally provides up to 95% of the value of outstanding invoices, depending on the nature of the business, who the customers are and how much they pay.

The repayments come by way of collections when the customers pay their invoices, and the borrowing limit is based on how much you are owed at any point in time.

Langham says the finance can be used as main working capital for the business, or as extra cash to pay suppliers earlier or invest in growth, and has even been used for business acquisitions or change of ownership.

One area in which it can be particularly useful is when businesses are seeing increased demand, as they may be during the coronavirus pandemic. Debtor finance can provide extra cash when sales are growing and staff and supp liers need to be paid on time.

liers need to be paid on time.

“Most of our clients like the simplistic idea that, with debtor finance in place, if sales increase they know they have the extra working capital to support that growth,” Langham says.

Helping businesses through cash flow challenges

Cash flow is the most common cause for concern for business owners. According to a report by the Australian Banking Association last year, maintaining short-term cash flow or liquidity was one of the top three reasons businesses sought finance in 2017/18.

“Debtor finance can help business owners access more reliable cash flow so they can manage fast growth or deal with winning a big new client, long payment times and more,” Langham says.

In the current environment, maintaining strong cash flow is “more critical than ever”, he adds. In in the 30 years that Scottish Pacific has been around, Langham says it has seen debtor finance prove itself through all stages of business – in good times as well as during the GFC.

“Along with the challenges the COVID-19 pandemic is causing, many new opportunities may present themselves, and those businesses with cash will be able to take advantage of these opportunities,” he says.

Finance brokers are already helping businesses with things like debtor finance, thanks to COVID-19. James Macfarlane, director of HLB Debt Advisory, has been offering debtor finance for three and a half years and is being asked to help now that the pandemic is impacting cash flow.

“I have been mandated recently by a strong group for three of their businesses as they are expecting debtors to pay them more slowly and also maybe some of them will not survive, so having limits in place will reduce the need to raise equity or other forms of cash,” he explains.

Agreeing that cash has never been more important, Chris Slack from The Finance Consultancy says debtor finance is a great alternative for those businesses that are not eligible for the government-supported small business loans. He says the debtor finance option can give a business the sort of access and flexibility it needs and can arguably be implemented faster than alternatives.

“Debtor finance may be the most likely option to take advantage of the opportunities out there for other businesses that are growing quickly against the trend and are unable to source the funds at the speed of demand for their product or service,” Slack says.

Even outside of global pandemics, debtor finance plays an important role in supporting businesses through everyday challenges. Slack explains that this might look like businesses being able to access discounts for early payments to suppliers, or it might be the only way they can pay rent or staff due to the seasonality of some businesses.

Slack says the “secret” here is that it is very rare for someone to ask for debtor finance, other than those who already use it, and often it becomes an integral piece of a wider puzzle.

“Does a client source items from overseas? Do they have an equipment need? Are they looking to acquire another business but don’t have the available cash? Do they need a little term debt for their business?” he says.

“Debtor finance can tie any and all of these scenarios together, as lenders can gain more comfort with a transaction when they have that greater level of oversight and security. So, it’s more that I’m promoting it as part of the suite of options for solving a problem, rather than something that people come to me for.”

for.”

Opportunities for brokers

Beyond the benefits for SMEs, Langham says offering debtor finance provides a real positive for brokers that are looking to forge stronger relationships with their clients. Scottish Pacific looks after businesses that want to grow, and as they grow, so do the brokers’ businesses.

“That business has ever-increasing needs for additional funding to support that growth – be it for machinery, vehicles or even the owner’s personal needs, such as a home loan,” Langham explains. “As the business grows, so does the broker, and this creates a deeper relationship between brokers and their clients.”

To ensure that brokers identify the opportunities available and are able to assist their business customers, Scottish Pacific partners with them to help them understand how to spot clients who may benefit from debtor finance.

As a broker who has now written more than $95m in debtor finance loans over the past two years, Macfarlane encourages brokers to take lenders up on these partnerships and training sessions.

“The most important thing is to understand how to finance businesses, and the options that are available, as debtor finance is just one of the options and most often is not the only solution,” he says.

“The keys are understanding the business’s P&L, balance sheet and cash flow, what the business is, what it does, and then matching that with the products and solutions available.”

Slack adds that the BDM support across all of debtor finance is “superb” and is the only way he has managed to grow in the space so quickly.

On the opportunities for brokers, Slack says, “If you are looking at B2B clients and simply defaulting to an unsecured option when a bank says no, then you are doing them a genuine disservice by not presenting debtor finance as an alternative.”