Finder says 40% found paying December mortgage a struggle

Experts are divided on the likelihood of an RBA interest rate cut in the next few months, but all agree borrowers are banking on it.

With inflation figures having fallen to the lowest level in almost two years, even the prospect of a cash rate rise in 2024 is up for debate.

Mortgage broker Helen Avis (pictured above left), director of Specialist Mortgage Finance, said her clients would breathe a sigh of relief if there were no further rate hikes over the next 12 months, with many feeling the pinch of the rising cost of living.

“Many buyers are concerned about the prospect of rate increases and their ability to service their mortgage,” Avis said.

“This is particularly evident within the first home buyer market who are often shopping at their maximum borrowing capacity, investors using property as collateral to secure finance, and our overseas clients who are often faced with higher rates than Australian residents.”

High hopes that interest rates won’t rise in first half

Avis said her clients are hopeful rates will remain on hold for the next six months, with most believing they won’t see rate cuts until 2025.

“Nearly all of our clients are choosing variable loans over fixed rates. This is in significate contrast to the height of the pandemic when borrowers were opting for low-rate fixed mortgages.”

Avis said clients’ sentiment towards the property market was still positive, “but they are approaching it with a little more caution”.

She said many clients were factoring in potential rate increases, often looking at property well under their maximum borrowing capacity.

Now is a great time for borrowers to take advantage of the competitive rate market.

“Our brokers are negotiating aggressively with our clients’ existing lenders to get the best variable rates, which is often preferable compared to switching to a new loan provider,” Avis said.

Buyers need to spend within means

aussieproperty.com buyers agent Julie Kelley said rate relief would instil confidence in the property market.

“As we all know taking on too much debt can lead to unnecessary stress; I always advise clients to shop in their comfort zone,” Kelley said.

“In such a competitive market, I understand buyers can feel frustrated by not being able to secure their dream home due to budget constraints, and they may feel pressured by selling agents to quickly submit an offer above their initial budget. But it’s important not to let emotions take over.

“We always advise our buyers that are considering pushing their borrowing limits to first speak with their mortgage broker and factor in all increased costs such as stamp duty, repayments and LMI before submitting an offer on a property”.

Financial comparison site Mozo’s money expert Rachel Wastell (pictured above centre), money expert at financial comparison site Mozo, said mortgage holders would welcome a rate cut, no matter how small.

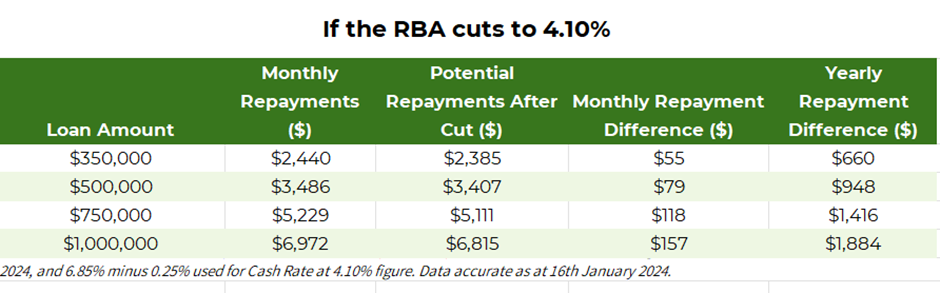

Mozo analysis shows someone with a $1 million mortgage, following a rate cut to 4.1%, will have an extra $157 a month in their pocket, equating to $1,884 a year based on the variable rate staying the same (see Mozo data below).

Source: Mozo

“I think borrowers will be cheering when a rate cut comes through,” Wastell said. “After one of the most aggressive rate hiking cycles since the early 1990s news about rates has unfortunately been quite doom and gloom.”

RBA on track to meet inflation goal?

Wastell said a rate cut will likely give borrowers some hope that the RBA is on track to meet their inflation target, and that more rate cuts could be on the horizon.

“In a cost-of-living crisis every cent counts; $100 more a month might not seem like much, but for those mortgage holders who have now resorted to credit cards or buy now pay later services to cover their everyday expenses,” Wastell said.

“That $100 could be the difference between clearing those monthly balances or being in the red.”

Despite what borrowers want, Wastell said a rate cut in the next few months was unlikely, as the unemployment rate was holding steady and inflation in services, particularly insurance, was still high.

“Later in the year, if there are no further rate hikes, and the CPI data for the June quarter shows we're much closer to the RBA's target of 2% to 3% we will probably see a rate cut or two, but I think it's important homeowners don't count their chickens before they hatch.”

Experts predict February cash rate pause

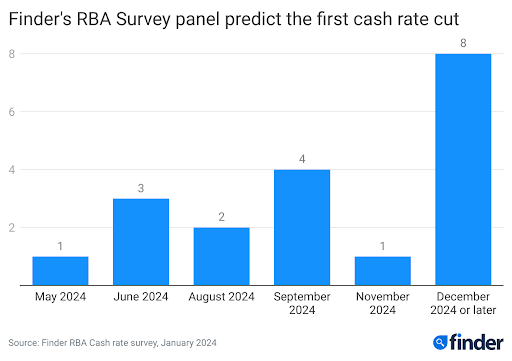

In this month's Finder RBA Cash Rate Survey, 19 experts and economists weighed in on future cash rate moves and almost all of the experts, 89%, said the RBA would hold the cash rate at 4.35% in February.

Head of consumer research at Finder Graham Cooke (pictured above right) said many Australians were in urgent need of reprieve following the last rate rise in November.

"Homeowners are still reeling from 13 rate hikes in the last two years,” Cooke said.

“Our data shows a staggering 40% struggled to pay their mortgage in December. Even though inflation is falling, I expect the RBA will hold the cash rate for most, if not all of 2024.”

While one in three Finder panellists predict a cash rate cut by at least August this year, almost half, or 40%, don't expect the RBA to start cutting rates until December 2024 or later.

The majority of Finder experts, or 71%, said they expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it's likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

Earlier this month, Bank of Queensland chief economist Peter Munckton said talk of rate increases by the RBA this year were “in the rear mirror” and said the big question for 2024 is when would interest rates start to fall.

Are you expecting a rate rise this year? Share your thoughts below