Digital banks are entering the scene with the aim of disrupting traditional banking, but will they ever be able to take market share from the big four?

Digital banks are entering the scene with the aim of disrupting traditional banking, but will they ever be able to take market share from the big four?

A smarter way to help brokers with their borrower customers is coming as the Australian neobanking market heats up; but the major banks “won’t go quietly into the night”, says one research analyst.

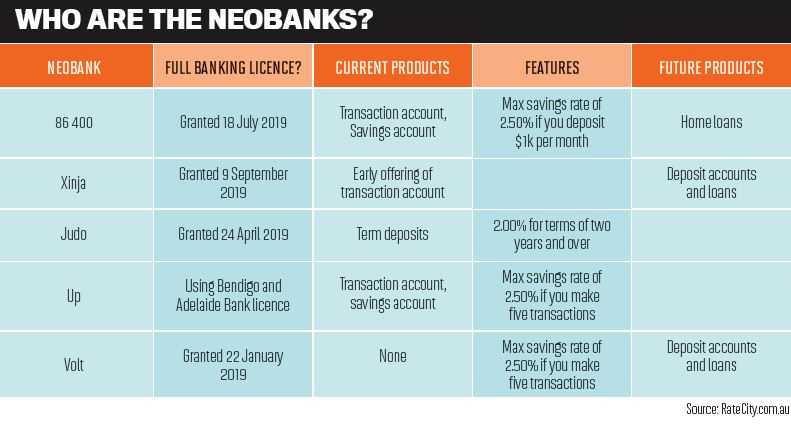

Last month, digital bank Xinja was granted its banking licence and rival digital bank 86 400 went live after receiving its own licence back in July. Both are aiming to disrupt the banking sector and improve consumers’ understanding of their finances.

Speaking to MPA, 86 400’s home loan lead, Melissa Christy, says staying on top of finances has become “too complex”, which has left people feeling stressed, anxious and frustrated. While the way consumers pay for things has changed dramatically over the last few decades – from physical cash to bank cards to phones and now to watches and even rings – banking has stayed the same.

According to the latest NPS results from Roy Morgan, the smaller banks are leading the way in terms of customer satisfaction. Westpac, ANZ and NAB all have scores in the negative, although satisfaction has been steadily growing since the release of the royal commission final report in February.

“We will eliminate key pain points for brokers by simplifying the income and expense verification process” Melissa Christy, 86 400

Changing the future of home loans

Currently, 86 400 has gone live with two accounts: pay, and save. These accounts will provide a more holistic view of a customer’s spending behaviour and through that will be able to help them with their future spending. They will provide a useful tool for brokers in helping borrowers track their expenditure.

“We’ve designed and built a bank which works a little differently. We enable our customers to look forward, as well as backwards, and help understand what’s actually going on with their money, surfacing the most relevant information about upcoming bills, subscription payments and direct debits so they feel in control,” Christy says.

“In the coming months, we’ll launch our competitive home loan offering, which takes the same smart approach as our pay and save accounts. This will be available through brokers.”

Explaining more about 86 400’s home loan product, Christy says that along with the rest of the bank it will be digitally led.

“We’re making it as easy as possible to fulfill a loan and reduce the amount of paperwork for both brokers and their clients,” she says.

“We will eliminate key pain points for brokers by simplifying the income and expense verification process and improving the borrowing experience, making it quicker and easier to get a decision from 86 400.

“Brokers currently waste too much time trawling through paperwork. We have the smart technology to do that for them, letting them prioritise the stuff that really matters: more time with their clients.”

Xinja is also hoping to change the way consumers interact with their finances, with its main purpose to help people make more out of their money and get out of debt faster.

Founder and CEO Eric Wilson says if Xinja sticks to that premise, it will succeed.

“We’ll use technology and data to prompt money-mindfulness, nudging people toward better everyday behaviour that can improve their finances,” he adds.

The technology includes hyperpersonalised, data-driven messaging, products and services to help the bank’s customers achieve their financial goals.

US-based banking futurist and adviser to the Xinja board Brett King recently told a banking technology seminar that banks that were using new technology to help their customers would retain those customers.

“We know that if we do the right thing by our customers, they will stick with us and recommend us to their friends,” Wilson said.

“I know we will make less money from our customers than traditional banks. We are fine with that. Our key performance indicators at Xinja bank include ensuring our customers do better. That’s an important difference between us and our competitors.”

“If the neobanks start gaining traction, the big four are likely to respond in spades” Sally Tindall, RateCity.com.au

Competition for the big four

In an age when consumers are looking for “disruptors”, they want an easier way to do things. But can the neobanks compete with the big four banks?

RateCity.com.au research director Sally Tindall says the big banks have deep pockets and do not like losing market share.

“The big banks are already investing heavily in retail banking technology. If the neobanks start gaining traction, the big four are likely to respond in spades to make sure they appeal to tech-savvy Australians,” she says.

While consumers are on the lookout for disruption and technology, they remain extremely loyal to their banks. Tindall says more than three quarters of savings are with the big four and their subsidiaries.

“Neobanks are unlikely to rock this boat any time soon,” she says.

To compete, neobanks like 86 400, Xinja and Up will have to be competitive on both technology and pricing. But Tindall says this is proving to be difficult.

“So far, 86 400 and Up are both offering a maximum savings rate of 2.50%, which is the equal-highest rate on our database, while Judo Bank is offering term deposits of up to 2.00%, which is one of the most competitive rates on the market,” she explains.

“If the neobanks start gaining traction, the big four are likely to respond in spades” Sally Tindall, RateCity.com.au

“When it comes to transaction accounts, the neobanks will find it near impossible to compete on cost. Up and 86 400 transaction accounts include some international fees and don’t waive all domestic ATM fees, when a growing list of banks do.”

But Tindall says there is “no question” that neobanks will drive innovation in the sector. Neobanks don’t have the cumbersome banking systems that are known to slow the bigger banks down, and they don’t have branches costing them money, she says.

“In order to be successful, neobanks will have to patiently chip away at the market. But the big banks won’t go quietly into the night.”