ADIs post a 4.3% annual growth in residential mortgage lending

The Australian Prudential Regulation Authority (APRA) has reported a surge in new housing lending and a decline in external refinancing levels from previous highs in its latest quarterly publications.

The reports, which cover the quarter ending Dec. 31, highlight key trends in the banking sector, including the performance of authorised deposit-taking institutions (ADIs) and property exposures.

Despite the rise in interest rates, borrowers have shown resilience, though APRA noted an increase in financially stressed borrowers. The industrial sector’s strong demand has buoyed commercial property lending, even as non-performing commercial property exposures ticked upwards, remaining low overall.

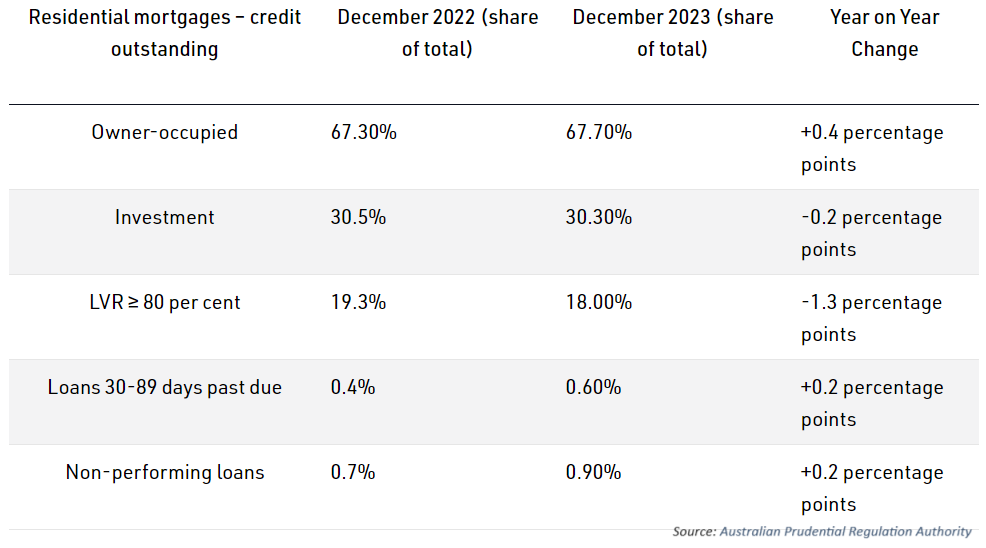

For the quarter, ADIs saw a 4.3% year-on-year increase in residential mortgage lending, reaching $2.21 trillion. Owner-occupied mortgages rose by 5.1% to $1.48 trillion, while investment property loans grew by 3.80% to $662.1 billion.

The share of owner-occupied loans inched up by 0.4 percentage points, contrasting with a slight decrease in investment property loans’ share. Loans with a loan-to-value ratio of 80% or more and non-performing loans both saw increases, highlighting a subtle shift in borrower profiles.

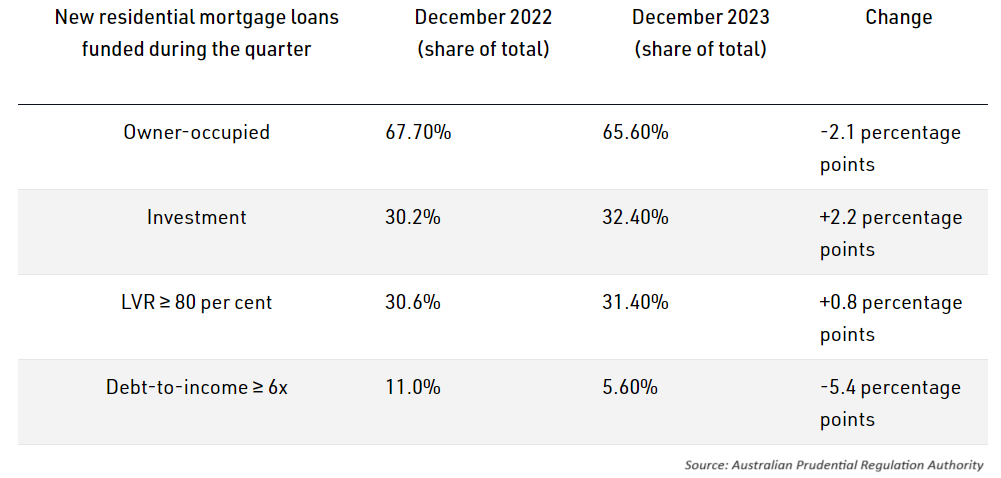

In terms of new residential mortgage loans funded during the quarter, there was a modest 1.6% increase to $152.5 billion. The distribution between owner-occupied and investment loans shifted, with investment loans seeing a rise in their share. Additionally, there was a notable decrease in loans with a debt-to-income ratio of six times or higher, suggesting a tightening in borrowing standards.

Commercial property lending statistics for the December 2023 quarter also revealed significant growth, with total commercial property actual exposures rising by 11% to $414.7 billion.

APRA also reported that overall, the banking industry remains well-capitalised, despite facing margin compression and a decline in profits. Profit levels are still high by historical standards, it added.

Liquidity and funding levels are well above minimum requirements, indicating that ADIs are in a strong position to manage potential credit losses and navigate the changing economic landscape.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.