13 lenders cut fixed rates in January

Interest rate experts say the mortgage market is moving away from the competitiveness of recent months with less focus on incentives.

Mozo banking and rates expert Peter Marshall said the home loan market in Australia was now shifting away from “the intense competition of the mortgage wars” after predictions there would be a surge in refinancing as home loan holders fell off the mortgage cliff in late 2023 didn’t come to fruition.

“Banks are withdrawing cashback offers, fee waivers, and other incentives and the expectation of a post-cliff surge in refinancing has dwindled,” Marshall said.

“It now looks like lenders are now redirecting their efforts towards enhancing profit margins in the face of potential rate cuts at the end of 2024.”

Marshall (pictured above left) said despite the drop in competition between lenders for mortgages, fixed rates continued to show a downward trend and longer-term fixed rates were being cut at a faster pace than their shorter-term counterparts.

Lenders cut fix rates in January

According to the Mozo database, 13 lenders have cut fixed rates in January, and while most have been small cuts of 10 to 15 basis points across the board, some are hiking some terms by more than half a percent

“The downward trend for fixed-rate options is making these home loan products increasingly attractive for mortgage holders,” Marshall said.

“But borrowers need to consider the impact of locking in a comparably low rate now when the RBA is predicted to start cutting the cash rate later this year.”

According to Mozo’s data, most lenders who are cutting fixed rates are doing so across all terms.

While various lenders have initiated cuts ranging from 10 to 30 basis points across terms, Macquarie has made substantial cuts, slashing fixed rates for three year terms by 0.56% and two year terms by 0.50%.

“Lowering two and three year fixed rate terms helps banks attract borrowers to increase profitability over the long term as future cuts could mean fixed rates surpass variable rates,” Marshall said.

“Even if cuts don’t come within that time frame or rates actually increase, the interest rate loss the bank is exposed to is only two or three years, so the risk is fairly limited.”

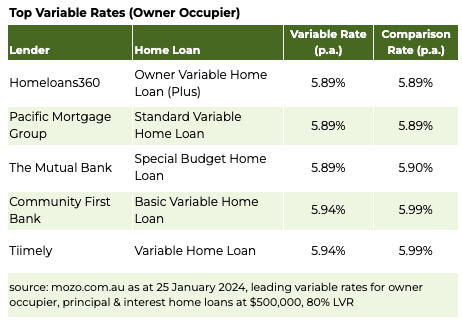

Variable rate moves

Marshall said when it came to movement in variable home loan rates, the trend had been predominantly up, averaging at about 10-15 basis points, and mostly from smaller lenders however, there were some lenders hiking by up to 30%.

Mozo finance expert Rachel Wastell (pictured above right) said home loan rates were roughly 3 percentage points higher than they were five years ago, which meant that the smallest difference in interest rates had a much larger impact in real dollar terms.

“Cashback offers and incentives may be exciting and lure in borrowers, but even when they were on offer for borrowers, the value was often only a few thousand dollars,” Wastell said.

“So, regardless of whether the mortgage wars are coming to an end and incentives and cashback offers have been taken off the table, borrowers that look for lower rates will still benefit the most over the long term.”

“Mortgage wars or not, getting a home loan that has a low rate with the least amount of fees and charges attached is how borrowers can get the most competitive deal.”

Speculation over interest rate drops

Wastell said there was an expectation that rates would be cut towards the end of 2024, following the last rise in November last year. Borrowers are likely to wait and see what they might be eligible for, rather than refinancing to a fixed rate now.

“However, there is still a big difference between the leading variable rates under 6% and the average variable rate of 6.85% on the Mozo database,” Wastell said.

“So, if borrowers are paying a high variable rate, and waiting to switch to a lower fixed rate when rates come down, they could be leaving money on the table by not switching to a lower variable rate while they wait.”

Wastell said lenders had been pricing in some cuts to fixed rates, so these rates looked competitive, but the risk remained that variable rates could drop below the fixed rates on offer now during those fixed rate terms.

When it came to when the first rate cut will occur, Wastell said the jury was still out, although many in the finance sector would be watching Wednesday’s quarterly CPI release closely.

“From looking at the slowdown in the monthly CPI figures, it does seem unlikely that we’ll see a move at the February RBA meeting as inflation is easing and getting closer to the RBA’s target range of 2% to 3%,” Wastell said.

“If there are any rate cuts this year, they’ll most likely be at the tail end, as monetary policy operates at a lag and the impacts of the 13 rate hikes since May 2022 are still filtering through the economy.”

Many commentators, including Bank of Queensland’s chief economist Peter Munckton, have predicted no more rate rises for this year.

Are lenders changing their approach to wooing borrowers? Comment below