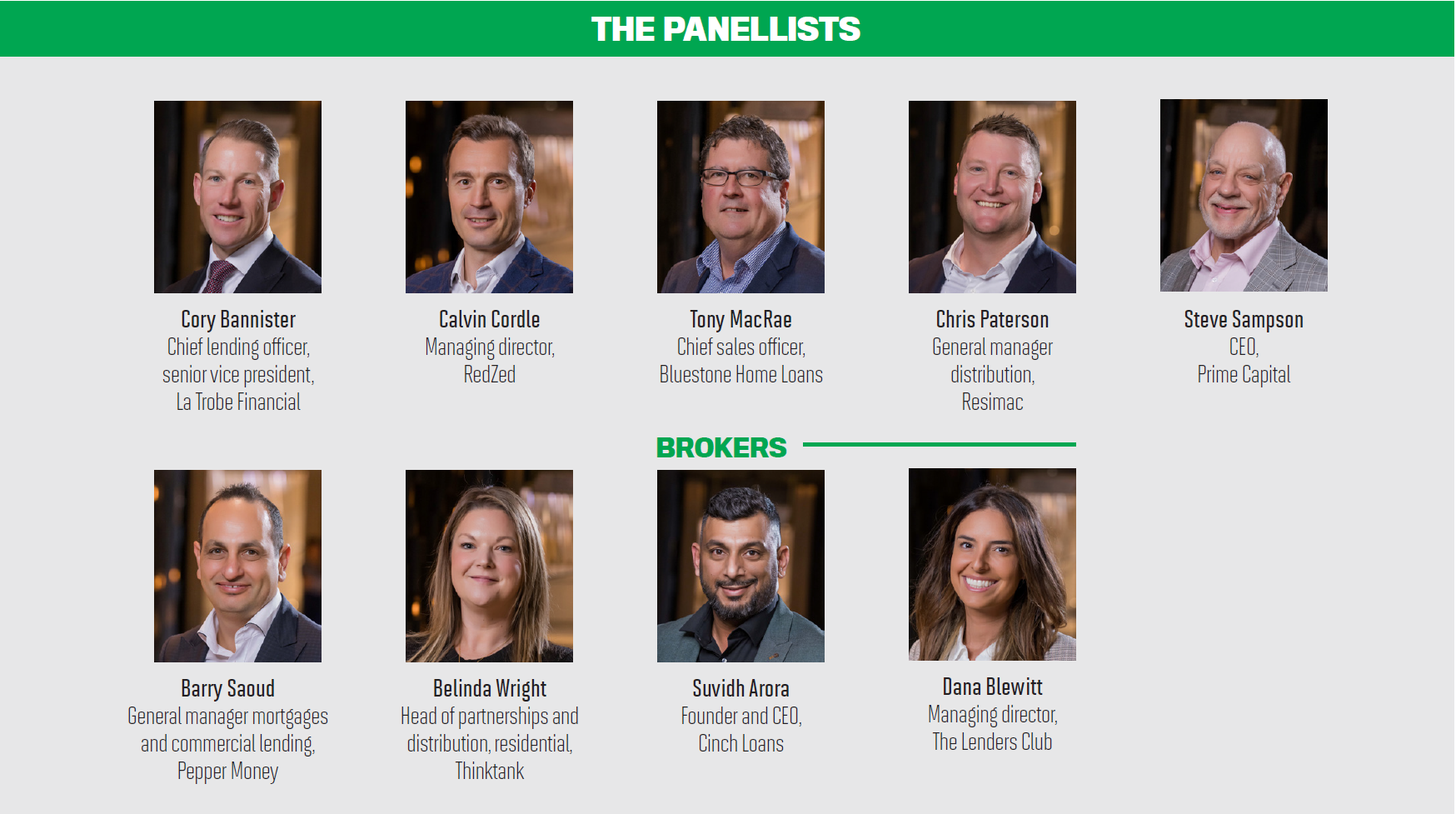

MPA's non-banks 2023 roundtable discusses challenges and opportunities

In a time when borrowers are feeling the effects of rising interest rates and higher inflation, non-bank lenders are adapting well to a changing market.

Faced with intense competition from the banks, particularly for home loans, non-banks have focused on what they always do best – helping specialist or non-conforming customers who fall outside the banks’ credit appetite.

Non-banks have also strengthened their partnerships with brokers, who they rely on for most, if not all, of their lending pipeline. This has meant encouraging brokers to branch out into commercial finance and SMSF lending to diversify their customer base as residential lending slows.

To gain an understanding of what’s happening in the sector, MPA held its 2023 Non-Banks Roundtable at Silks restaurant in Sydney.

Participants included Cory Bannister, chief lending officer at La Trobe Financial; Calvin Cordle, managing director, RedZed; Tony MacRae, chief sales officer, Bluestone Home Loans; Chris Paterson, general manager distribution, Resimac; Steve Sampson, CEO, Prime Capital; Barry Saoud, general manager mortgages and commercial lending, Pepper Money; and Belinda Wright, head of partnerships and distribu- tion, residential, Thinktank. Two brokers also attended: Dana Blewitt, director of The Lenders Club, and Suvidh Arora, founder and CEO of Cinch Loans.

It’s been a challenging 12 months with higher interest rates and inflation affecting mortgage holders, especially those coming off low fixed rates onto higher variable rates. How have you worked closely with brokers to assist these customers?

Steve Sampson (pictured below) of Prime Capital started the discussion by saying that the increased cost of living and rising rates had created a challenge for the non-bank lender’s customers and brokers.

He said, “Some customers have endured rate increases that have gradually crept up and up. It’s not only those that are coming off the mortgage cliff, it’s those that have been on a variable rate that have also suffered. So every month their repayment changes, and I think that’s as much of a challenge as the mortgage cliff.”

Prime Capital was proactive in communicating with brokers and customers, Sampson said.

“We rejigged our whole customer contact program to let customers know before their repayments came up what it was going to be. If they hadn’t made that changed payment amount, we were SMSing and emailing customers and our brokers to make sure they were aware of that new payment amount.”

Sampson said IDR (internal dispute resolution) was also “pumped up” to make it stronger for the customers’ benefit.

At RedZed, Calvin Cordle (pictured below) said the impact of higher interest rates and inflation on customers had been more benign than expected.

“That’s not to say there aren’t a lot of borrowers who have been challenged in the last 18 months in a stressful and difficult time, but equally, you plan for the worst,” he said. “We’re still going through the cycle; it’s got a way yet to play out.”

Cordle said RedZed didn’t offer fixed interest loans, only variable. As a result, borrowers were experiencing interest rate increases on a regular basis, giving the non-bank a better view of mortgage stress.

“You can be proactive and on the front foot with that. For brokers and borrowers, the key is to engage with your lender early so we can do something about it; we can help and support.”

Tony MacRae (pictured below) said Bluestone Home Loans also reiterated early engagement when communicating with both customers and brokers.

“I agree [with Cordle] – it’s been more benign,” he said. “The first principle for us is that we’re a non-standard lender and we’ve looked at how we can help more people who find themselves in that space.”

MacRae said Bluestone had expanded its credit policy so it could work with more customers. “The reality is in the changing economy and with people under stress, more and more customers are falling into that non-standard space, where the banks just won’t or can’t help them.”

He said Bluestone had tried to open up avenues to help those customers and then regularly communicate with brokers about the non-bank’s offering, working outside of the lending restrictions that banks face.

Cory Bannister (pictured below), of La Trobe Financial, said the benefit of the non-bank solution was that it was tailored.

“It’s going to be individualised; you can’t take a flat approach to any customer, whether it’s an existing customer or a potential new customer,” he said. “You need to understand their needs and requirements and tailor that solution accordingly.”

Bannister agreed with the other speakers about early engagement with customers, saying La Trobe Financial “targeted who we thought was at the highest risk of stress and were proactively calling them before they called us. That was a really successful approach”.

Belinda Wright (pictured below) said Thinktank had been actively supporting its existing customers to assist in the changing market conditions and repricing where needed.

“If a customer does contact us for a review, we make sure we action the request within 24 hours. Some lenders can take days or even weeks, which is extremely frustrating for the broker and customer.”

Wright said that, on the commercial finance side, when the Reserve Bank first started to move rates, Thinktank recognised a strategic opening to review existing policies. Consequently, the business was able to lower its ICR cover, improving servicing opportunities for customers who were refinancing.

“For customers who have a genuine sale need due to financial hardship or other personal pressures, we’ve reduced or waived our early repayment fee to support them with this event.”

Barry Saoud (pictured below) of Pepper Money said it was a difficult time for borrowers and brokers.

“It all comes back to what non-banks stand for, and for Pepper Money it’s about trust and transparency,” he said.

The focus at Pepper Money had been on how it supported brokers, looking at product innovation and policy expansion and providing an accessible credit team to deliver a unique service proposition.

“During these difficult times, you’ll see

“As an industry, we continue to look beyond the traditional borrower to support brokers with their real life.”

At Resimac, Chris Paterson (pictured below) said that when considering new business, the non-bank looked at different solutions that could help customers with access to finance.

“This includes reduced serviceability buffers and removing the loading on interest-only loans,” he said. “We also tailor our lending solutions to look at things like debt consolidation, overall repayments and the customer’s lifestyle, as opposed to just their mortgage debt.”

He said some customers had been prepared for rising interest rates, while others hadn’t.

“It’s about looking at customers as more than just a credit score. We take a holistic view and for instance look at what they’re spending versus what they’re willing to borrow. This way we can really help them with their requirements.”

Suvidh Arora (pictured below) said Cinch Loans had gone through its entire customer back book and proactively repriced over the last 12 months. “That’s helped the lenders retain those customers but also the customers avoid coming off the rate cliff or at least be able to manage their repayments and not have as much mortgage stress as was anticipated.”

Dana Blewitt (pictured below) of The Lenders Club said her brokerage had found some banks were taking a long time to do repricing. “They’re taking 20 days to come back to you with a new rate, and then when you’re sending in a discharge, they’re taking 30 days to discharge a loan when it really shouldn’t be that, and you’re charging high interest rates.”

Customers found this frustrating, Blewitt said, but most banks did look to bring interest rates down if a customer or broker requested it. “We’ve also been on the frontfoot helping customers with their repayments and budgeting.”

Cordle said non-banks all competed hard with each other, but the major theme was these lenders had a critical role to play in society as borrowers went through difficult times. “Particularly in the non-prime, near prime space. As I look forward over the next couple of years, I think that’s important.”

Wright said she wasn’t a suppporter of cashbacks, and at one time there had been around 23 cashback offers on the market.

“A consumer posted on a forum that they made $36,000 a year just by continually refi- nancing their loan with different lenders,” she said. “It’s not sustainable for any business. We are pleased that they [banks] have pulled back on cashbacks – it’s just a race to the bottom otherwise.”

Wright said cashbacks could be compared to someone starting a new relationship and receiving flowers on their first anniversary: “you can be sure they are expecting more than flowers the second year”.

“We need to consistently provide outstanding service to our customers not only when we onboard them but throughout the entire home loan life cycle.”

For Thinktank, having great onboarding was important for customer retention, Wright said, but so was meeting the ongoing servicing needs of customers.

She said 90% of Thinktank’s customers were self-employed, so the non-bank had focused on the challenges SMEs had faced over the past three years.

“A big driver is policy. Thinktank does not necessarily seek to be a price-only lender, but we can adjust our policy to assist customers that may have to work harder to fit traditional bank policy. Additionally, as we saw more PAYG customers becoming self-employed, Thinktank reduced its ABN requirement to three months.”

Wright said making slight policy adjustments helped borrowers and brokers understand that the non-bank’s offering was about more than just price.

MacRae said the cashbacks came mainly from banks, and as a non-standard lender Bluestone did not view itself as competing with banks. “We target a different set of customers that have completely different circumstances than the banks.

“For us, the answer is about making it easier for the customer and for the broker, ensuring that we’ve got a policy set that captures those customers, and then providing brokers with the right avenue to come to us.”

MacRae said the great thing for brokers was that they could talk directly to Bluestone’s underwriters.

“You’ll get confirmation from that person before you send [the loan application] in, so yes can mean yes in that scenario.

Giving a broker a chance to workshop with the person that’s going to approve the loan and then put it through is where we’re really competing as opposed to trying to battle cashbacks.”

He agreed with MacRae, saying RedZed also didn’t see itself as competing with big banks, and it had a different value proposition. “We were founded 17 years ago on a simple premise – that we’re very, very high service – and we invest in that. We focus heavily on saying yes quickly. We also have this simple catchphrase, which is ‘we answer the phone’.”

Prime Capital did not offer home loans or cashbacks, Sampson said. “We provide solu- tions, which is much more valuable than putting money into the customer’s bank account through cashbacks.”

“I think we’re in a V-shaped recession – there’s not ‘no light at the end of the tunnel’, and there’s a lot of customers out there that were bankable a year ago, but banks don’t want to know them now.

“That’s where we come in; we look after those customers. We give them the solu- tions. We might be helping them to go back to a bank, but our proposition is much more valuable than a few thousand dollars in the bank.”

Echoing others’ comments, Bannister said La Trobe Financial didn’t compete with the banks; it focused on providing solutions to borrowers who “sit just outside that automatable space”.

“On cashbacks, my personal view is that I don’t think they make for great customer outcomes in the long run. Debt is an instrument to enable something; it shouldn’t be a potential tool that can be gamed to generate a short-term profit – it’s just not a good look.”

Bannister said the non-banks’ biggest weapon when it came to promoting their value proposition to borrowers was the broker. “Brokers do an incredibly good job of explaining that to customers and selling that story and those benefits on behalf of non-banks.”

Blewitt said she used non-bank lenders for short-term lending. She explained to customers in that space, especially the self-employed, about all the great non-bank options available and what they needed to do to return to a bank.

“They don’t want to stay 30 years at a non-bank lender. For us it’s about short- term lending and maintaining that relationship so when they are ready to move to a major or another bank, we’re able to help them with that.”

In terms of customer awareness of non-banks, Blewitt said it was up to brokers to know the lenders’ products and policies and the best options for their customers.

Arora said everyone wanted to pay the lowest possible amount for a mortgage, but it was also about providing a solution for a client and educating them on the options.

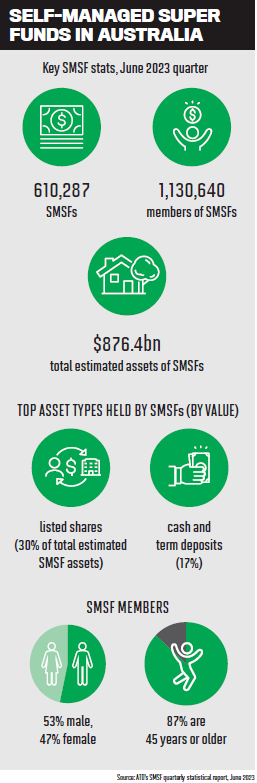

“What also helps us spread awareness about non-bank lenders is the other diversified products they offer, such as SMSF lending, which many banks don’t offer.”

“Given the rising rate environment we are in, we continue to proactively work with customers to ensure those that need support receive it,” Saoud said. “So far that cohort is small, and we also proactively work with their brokers to better support their customers.”

Paterson said Resimac offered some low-LVR, low-risk prime products that could compete with the banks.

“We didn’t go down the cashback path because we saw that as taking value away from brokers. Customers go to brokers for recommendations and advice on what loan is suitable for them in the long

Resimac increased commissions on certain products for brokers to offset the cashback offers of the major banks, he said. “We saw that as a better way – recognising the addi- tional value that brokers were providing certain types of customers and compensating them accordingly.”

Saoud said Pepper Money saw SMSF lending as a good target market, given it was a space that the banks had retreated from.“We saw it as a really good opportunity to provide both solutions and service into that space. We launched a pilot three months ago and tested the product with a select group of brokers.”

Pepper Money had recently launched its SMSF lending product for residential and commercial securities.

“We’re really pleased with the product and the feedback from brokers to date,” Saoud said. “We think there’s an underserved segment, and non-banks play really a good role, and we’re here to tap into that and support brokers in that space.”

MacRae said Bluestone had introduced SMSF lending late last year, and “it’s been one of the real success stories for us, as a number of banks have exited that space”.

He said it was also an opportunity for brokers to be introduced to non-standard lending because the concept of SMSF was well recognised and understood.

Bluestone had invested in educating brokers, with an SMSF specialist conducting broker seminars and webinars to explain how SMSF lending structures work and how to set them up. “It’s education on SMSF first, then Bluestone product … we think we have a well-priced product and a really slick process and can do that well,” MacRae said.

Wright said Thinktank had been active in the commercial and residential SMSF space for 10 years now. Many residential brokers had told Thinktank they weren’t seeking to offer SMSF or commercial loans, but in increasingly challenging times when they weren’t writing as many residential loans, their focus was turning to diversification.

“Educating brokers about how to diversify into self-managed super funds and commercial is an essential part of how we assist brokers to grow their businesses,” Wright said.

“We have a dedicated team of relationship managers who are able to support our broker partners with joint visits to their financial planner or accountant referrers to assist with deeper conversations around SMSF and commercial client needs.”

Once the structuring and process were explained, Wright said, writing SMSF loans was straightforward, especially for a refinance. Blewitt agreed that refinances were easy now, with online banks coming in and competing, offering low rates and easy refi processes after 12 months. However, non-banks weren’t competing in this space.

“They just used to sit on our books; we wouldn’t refinance them. But now, with so much competition online, they are starting to refinance,” Blewitt said.

Wright said digital mortgages were popular three years ago, with fears they would replace brokers, but this had not yet eventuated.

Wright asked Arora and Blewitt if borrowers had reported bad experiences with online loan providers. They said this hadn’t occurred, and Blewitt added that it was probably due to clients having to get all their financial documents prepared each year for their tax return, meaning they could refinance easily.

“I’m finding that people are becoming way more savvy in that space and deciding to refinance even after eight months. The competition online – it’s hard to compete in that space,” Blewitt said.

It was not just the independent online lenders, Arora said. “It’s also the online arms of existing vendors that are cannibalising the product. We’ve had instances where the client has gone online, and the rate offered by the online version is 25 or 50 basis points lower than we can offer, and there’s no negotiation – when we go back to the lender they say ‘we can’t do anything’.”

MacRae said 100% of Bluestone’s loans came from brokers, and “we want to avoid any forms of channel conflict”.

“We only exist because brokers refer business to us.”

Cordle said RedZed planned to introduce SMSF lending very soon – a residential and commercial full-doc and an alt-doc SMSF product – because the opportunity is significant for self-employed borrowers.

Raising the issue of the federal government’s proposed capital gains tax ruling on SMSF balances greater than $3 million, Cordle said this could mean that SMSFs would have to pay tax each year on property capital gains above that amount, even if they were unrealised.

“This is something we have to watch out for. If you’re a self-employed borrower, for example, you’ll have to find the cash for this.”

“We’ve seen it grow and competition come, and I think that’s great. We’re actually looking forward to more players in the space.

It’s a case of a rising tide lifts all boats.”

Bannister said the investor market had a bright future, with “value coming back to the market over the last 12 or 18 months. Self- managed super funds are a great vehicle for people to access the market … for people with an

With an undersupply of property and rents likely to increase, the fundamentals for an SMSF investor to capitalise on property were very strong, Bannister said.

“It’s also what Australians know, like and love, so why shouldn’t they choose to invest in properties? We think there will be strong growth in the SMSF sector, so additional players in the space are welcomed to service what we expect will be a fast-growing market.”

Sampson agreed with Bannister’s assessment. “Prime Capital has always looked at the market and the gaps that can be filled, so when the banks started pulling out of SMSF, we brought an SMSF product out,” he said. “When the banks started pulling out of the foreign investor market, we brought a foreign investment product out.”

SMSF lending had been part of Prime Capital’s offering for a number of years, Sampson said. “We’re fast and simple. SMSF can be pretty rigorous, but we don’t have an application form. We will issue approvals, and then the solicitors will handle everything with the client from there.”

Sampson said that while SMSF was not a big product for Prime Capital at present, the lender would consider investing more into this space, given the growth occurring.

Bannister said the non-bank sector was in an “incredibly healthy state”.

“We’ve had a very pleasing last 12 months in terms of volume. Growth has certainly exceeded our expectations, particularly when you overlay the macroeconomic backdrop. To grow in those conditions against the grain is a very strong story. “

Times of challenge and complexity often provided opportunities for brokers and especially non-banks, Bannister said. “Conditions over the last 12 months were a strong tailwind for the non-bank industry, and I think that also carries forward for the next two to three years. You’re going to see a lot of customers that are going to need the support of brokers and non-banks. The future’s very, very bright.”

The opportunities were in both residential – for customers dealing with credit, job or cost of living challenges – and also in commercial. Bannister said La Trobe Financial was excited about the commercial lending opportunities, given that high-quality customers were failing to meet banks’ technical ratios.

Paterson pointed out that the cost of funds was normalising, whereas previously the banks had been supported by different cost of funds approaches.

“There’s a lot of competition in the non-bank sector, and it’s continuing to grow. Non-banks are providing solutions and options for customers in different segments at different times,” he said.

Paterson said all of Resimac’s products were sold through brokers. “We see investing in broker education as being very important, as customers go to brokers for that knowledge and expertise.”

Cordle agreed with Paterson regarding

Cordle said, “If you ask self-employed borrowers, they’re not doing it for the money, they’re doing it for the freedom, the passion, the joy.

“Only 15% of self-employed borrowers speak to their finance broker as a first step in seeking a loan for their businesss, and given the complexity I would argue that segment of the market needs a broker more than any other.”

He said brokers had a massive opportunity to help self-employed borrowers get finance, adding that RedZed had recently launched its Self-Employed Broker Academy, a five-module training program on understanding self-employed borrowers, their finances, how to structure loans and find the solutions they need.

Cordle said the program was free for accredited brokers and aimed to educate brokers who partnered with RedZed and were unfamiliar with self-employed borrowers.

“It’s an opportunity for brokers but also an opportunity for us to grow, particularly on the commercial side. Often the self-employed might want to own the property they operate out of because that gives them security and financial freedom.”

Wright agreed with Cordle about the commercial opportunities, pointing out that only about 20% of commercial loans went through brokers. She said there was a need to assist brokers who wanted to diversify so they could talk to their customer base about ommercial lending.

“If brokers have written a residential loan, they may expect commercial to be just as fast,” Wright said.

“Commercial processes did not evolve as quickly as residential during the COVID period. So the current challenge we are facing into is how we as commercial lenders work on digitising the process that still tends to be quite manual, in addition to providing that human support to add value with structuring and assist brokers through the loan process.

“The fundamentals are the same, but the process is quite different.”

MacRae pointed out that non-bank lenders were far more nimble. “Banks are burdened down by legacy systems, legacy platforms, legacy networks that we don’t have, so we have that opportunity to be far more nimble in the marketplace.

“The non-standard market is growing – more and more customers are falling into that space. There’s non-standard lending and there’s non-standard customers, and we want to help those customers and deliver for them.”

MacRae said the segment included credit-impaired, SMSF and self-employed customers and people transitioning into retirement, a market worth about $400 billion. “The loans we collect are only a small fraction of that, so there’s a real opportunity to tap into this. Embracing education and helping brokers grow their business is absolutely key.”

He added that Bluestone was also focused on simplifying and digitising its loan process to provide brokers with a quick answer.

Sampson said commercial or self-employed borrowers wanted two things: “They want the money quickly and want it to be simple. There was a survey last year, where 48% of those clients go to a non-bank because they want fast, simple finance.

“More non-banks are digitalising; we certainly are,” he said. “We’re trying to make things as fast as we can for the applications, for processing the loan and documentation. Home loan lenders have had that for a long time, but I think we’re catching up.”

Sampson said non-banks had to decide how far they wanted to go down the credit curve. Banks were “infiltrating” the non-bank space, courting self-employed borrowers because the margins were better.

“What was probably a traditional non- bank self-employed customer, the major banks are now chasing … so as a non-bank how do we keep those revenues, service and keep our customers?”

As a specialised lender, Prime Capital focused on managing risks as well as returns, Sampson said. “If non-banks manage their risks well, they can move down that credit curve a bit more, and there’s a big space for non-bank lenders there.”

Saoud said Pepper Money had a positive view of the non-bank sector, which was in a healthy state.

“We think that the borrower demographic is only going to change more rapidly in the future. We will see more and more self-employed; different types of demographics around multiple incomes, multiple jobs, casual income or different types of new asset lending.”

Saoud said the demand for non-bank lending should increase, and it was great that non-banks were diversifying into commercial and asset finance. A bigger choice of products and greater serviceability were good for non-banks and meant brokers could build stronger and deeper relationships with their customers.

Given the banks’ legacy systems, non-banks had an opportunity to shine, he said, being nimble and agile enough to support different policies, product expansion and a better broker experience.

Saoud said digitising the loan process was important, but even more powerful was leveraging data through open banking and positive credit reporting to create “a seamless transition, accessible credit and fast SLAs”.

Paterson said Resimac’s research had shown that “you need to be relevant from a digital and tech standpoint” to compete with the majors.

“You need to be supported by technology to be efficient in how you operate. But there also needs to be human interaction – the value of a credit assessor picking up the phone and talking to a broker to get a deal across the line; the benefit of brokers having their BDM on speed dial to talk through any client scenarios. We see that as really important. Continuing to invest in the quality of

“We don’t have the budget that the majors do, so we have to be smarter about deploying technology where it’s relevant to our business,” Paterson said.

“AI will evolve over time as well. Resimac won’t be a leader in that space, but we’re continuously watching the market in terms of digital transformation and will invest in the right solutions that deliver volume or efficiency benefits.”

“We’re making significant investments and committing resources to our commercial proposition – for resi brokers who may not have written commercial loans before. We’re here to support brokers through the process, and we’re already seeing increased volumes.

“We are focusing on giving our people the time to get out on the road and see more brokers, because that’s what brokers have been responding to, and we want to see them more often to discuss and workshop deals.”

Wright said it was all about ensuring a balance in terms of the useful deployment of technology in the business “so you don’t inadvertently arrive at a no when the deal has the potential to become a yes”.

“You need that speed to service but also to have your people go out and workshop and speak to brokers. We know that brokers want and need that human interaction; relationships are the differentiator in this industry.”

“I think using people and technology together and working where we can to solve pain points for our brokers is really important.”

Sampson said Prime Capital’s main customers were brokers, so digitisation was focused on them.

“We’ve just recently released a web form that sits on a lot of aggregator websites, and it’s fairly simple. It can just be picked up, requires a certain amount of information to be filled out, and then it comes straight through to our system in-house, which is called Loan Power. It’ll assess the loan – if it fits our parameters, it will send the approval back; if it doesn’t, it will go to a credit panellist and there’ll be a call from there.”

Sampson said there needed to be a dual digital channel for brokers and customers.

Pepper Money agreed that it was important to leverage technology, Saoud said.

“We’re also into generative AI, and we’ve looked at how we can deploy that in our own operations and how we can use it from the broker network as well.

“To Chris’s point, we definitely think that there’s a balance with both digitisation but also human interaction to make sure we’re giving the right level of service to the brokers and the customers.”

Saoud said Pepper Money had used generative AI to automate much of its credit decisioning, to get faster decisions and the right outcome for brokers. AI had also been used to make it easier for brokers to get quick answers when searching through Pepper Money’s guides.

“[Generative AI] has also been given to our BDMs to support them and give them confidence in their decisions and answers for brokers, and that’s worked out really well,” Saoud said.

Pepper Money aimed to enhance and optimise its use, and “once we’re really comfortable with that as a tool, we’ll take that out to the broker network as well”.

Saoud said the industry needed to be cautious with the implementation of AI.

“We’ve seen Chatbot failures where false information is provided; we’ve got to ensure it’s giving the right answers to the broker.”

MacRae said the focus should be on technology and data. “We want to get the technology right, but we want to make better use of the data that’s available. Non-bank lenders haven’t always used all the data available.

MacRae said the focus should be on technology and data. “We want to get the technology right, but we want to make better use of the data that’s available. Non-bank lenders haven’t always used all the data available.

“What we’re trying to do is better deploy some of that data and then become really clear what the rails are for a Bluestone loan and give a broker the confidence that if it sits within that, it’ll flow through friction- less. Then we’ll deploy our human energy and effort on those fringes to the rail.”

“Brokers and human interaction in a mortgage will always be absolutely critical. We need to blend those things [digital and human interaction] and get them right. Eliminate, simplify and digitise in that order, because if you try and digitise rubbish processes, it might be quicker, but it will still be a rubbish process.”

Saoud said Pepper Money was committed to sustainability and financial inclusion for the non-bank’s brokers, partners and customers.

“Pepper Money’s approach to sustainability aligns with our mission. We are focused on creating financial inclusion by challenging the way loans are designed and distributed.”

Cordle said RedZed was Climate Active certified carbon neutral, and this was a long- standing value of the company and a critical part of its framework.

“A lot of the big banks will look at age of a property and that’s it, but that is an incred- ibly blunt tool. In our view, that’s not the right way to look at it. I hope we’ll see something for RedZed in the next calendar year.”

Cordle said he believed non-banks wanted to find the funding benefit of green loans before building the product. “Everyone wants to give a discount for a green home loan, and when you’re already operating on very fine margins, you want to get the funding benefits,

Cordle said this made perfect sense, but the danger was that non-banks didn’t pursue green lending because it became a “chicken and egg” situation.

His preference for RedZed was to discover what self-employed borrowers wanted and build the green loan product accordingly, and “then if we can get a funding benefit, that’s great, but we don’t have to do that first”.

“But it’s bigger than green for us; we’re approaching our ESG strategy from a broader perspective. At Thinktank, we believe that meaningful and impactful ESG goals and practices are fundamental to how we interact with our people, our customers, our business partners and the global community.

“We’re in the process of developing specific green mortgage products designed for home-owners to build, improve and own environmentally sustainable homes,” Wright said. “It’s about addressing the customer need first and then going back to our wholesale funders and saying, ‘There’s a need here, there is a growing market; how can we mutually bring this to life?’

“From a community perspective, giving back is incredibly important to Thinktank and something we see as part of the way we do business. We donate $100 for every loan that’s settled back to charities chosen by brokers and our staff.”

Blewitt and Arora said customers hadn’t specifically asked for green loans, but Arora added that there had been a few enquiries about green and ethical loans.

“For all our clients, for our corporate social responsibility as well as for their green initiatives, for every loan we do for a client, we plant 10 trees on their behalf in a reforestation program,” Arora said.

What do you think of non-bank lenders' value proposition? Comment below