Rentvesting is a tactic used by aspiring homeowners to get onto the property ladder sooner. Does this investment strategy suit you? Find out in this guide

- What is rentvesting and how does it work?

- Who needs rentvesting?

- What are the pros of rentvesting?

- What are the cons of rentvesting?

- What factors do you need to consider before rentvesting?

- Can you use rentvesting to grow your wealth?

- How can you make rentvesting work?

- Rentvesting vs PPOR: which is better?

Soaring house prices remain the biggest obstacle for many aspiring homeowners wanting to buy a property in Australia’s most desirable suburbs. In capital cities where most people aspire to live and work, the cost difference between renting and purchasing a home continues to widen.

The situation has prompted many first-time home buyers to use a savvy investment strategy to climb the property ladder. This strategy, called rentvesting, has been gaining traction in recent years.

In this client education article, Mortgage Professional explains everything you need to know about this rapidly emerging property investment tactic. We will explain how it works and dig deeper into its pros and cons. If steep home prices are hindering you from buying a property in your dream location, rentvesting may be a good option. Read on and find out if this homeownership strategy is for you.

What is rentvesting and how does it work?

Rentvesting works by purchasing an investment property in an area that you can afford while renting in a place where you want to live in but cannot necessarily afford. This homeownership strategy has been gaining popularity among first-time home buyers in the country.

As a strategy, rentvesting can help you to overcome financial obstacles and the high costs that come with simply owning a home. In other words, it works because it allows you to rent in an area that better suits your lifestyle while purchasing a property in an area that better suits your budget.

It is a particularly deft tactic because even if you are renting at the same time, the property you purchased acts as an asset. It grows in value, especially if you have chosen a smart, strategic location to buy. At the same time, it is partially being paid off by your tenant. This also means that you are accruing equity that you can eventually use to purchase additional properties – such as a home of your own – when it makes financial sense.

Who needs rentvesting?

Rentvesting makes the most sense financially if the monthly differential between your mortgage repayments and rental payments is high. It is also a good strategy for people who make a wide range of incomes. If your rent and your mortgage repayments are about the same cost in your preferred location, it is probably not the right strategy for you.

The types of people who might need rentvesting the most include:

- young home buyers who find the costs of living in inner-city locations too high

- families hoping to live in better locations and a property that better accommodates them

- single parents where the area is best for raising a family

Rentvesting, however, is not only for those who are struggling financially. Those looking to improve their lifestyles can also reap the benefits of this strategy, since it can also help if you:

- need to move a lot for your work

- enjoy travelling for longer periods

- prefer the flexibility that renting offers, which also cuts out buying and selling fees

- want to live closer to entertainment districts typically out of your price range or in pricier suburbs

Rentvesting can also be a good homeownership strategy for those earning part-time incomes. Here is a rentvesting success story from a Sydney-based couple.

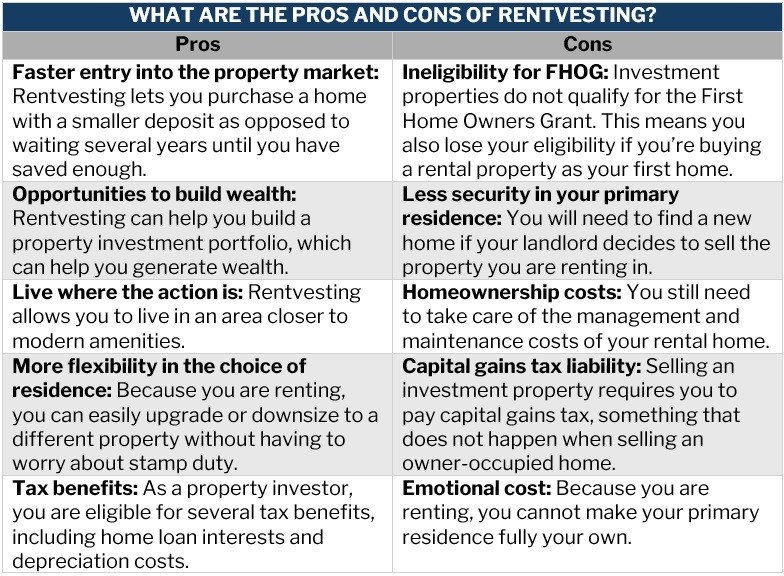

What are the pros of rentvesting?

One of the biggest advantages of rentvesting is that it lets you purchase a property and rent it out to pay for some of your homeownership costs. At the same time, you can continue to live in an area that suits your lifestyle. If your investment property yields profit, you can even use that income to pay for your rental expenses.

Here are some of the other advantages of this homeownership strategy:

1. You can get a foot onto the property ladder sooner.

Rentvesting can be a good tactic if you want to enter the housing market sooner as the property you are buying often requires a smaller deposit. This is better than postponing your home-buying plans for several years, so you can save enough money for a deposit.

2. You can build wealth to save for your dream home.

Property investments can provide you with a good opportunity to generate wealth. This allows you to raise enough funding to purchase your dream home or help you start building an investment property portfolio.

Another way to look at this strategy is to treat rentvesting like forced savings. Having an investment property while renting lets you focus on wealth creation instead of buying expensive things for your home. All the while, you are also building equity with your investment property.

3. You can get to live in a location “where the action is.”

Rentvesting allows you to rent in the area that you want to live in. It is also a major pro with regards to where you are in your life, local amenities, budget considerations, and safety and security.

Rentvesting also lets you live in areas where buying is not ideal because of soaring house prices. If the place you want to live in has affordable rental prices, then you can take advantage of this location without needing to commit to a long-term costly mortgage.

4. You can get more room for flexibility.

One of the advantages of renting is that you can easily upgrade or downsize to a different property without having to worry about stamp duty or other legal expenses. This is especially helpful if your financial situation changes.

If you are not ready to settle permanently in an area, rentvesting also gives you the freedom to move around and even travel to different locations if you wish.

5. You can access tax benefits.

The Australian Taxation Office (ATO) gives property investors several tax deductions. These include the interest charged for your home loan, depreciation costs, and rental property expenses, such as insurance coverage and advertising. These deductions can help minimise your annual tax bills, which can sometimes spell the difference between positive cash flow and negative gearing.

What are the cons of rentvesting?

Just like any investment strategy, rentvesting comes with its share of disadvantages:

1. You are waiving your eligibility for the First Home Owners Grant.

If you enter the property market as an investor as opposed to as an owner-occupier, you are disqualified from accessing the First Home Owners Grant (FHOG).

FHOG is a government-sponsored scheme that pays a one-off lump sum to first-time home buyers who qualify. You can use the cash grant when purchasing an existing home or constructing a new house if this is not intended as an investment property. You can also use the amount as a deposit.

The cash grant is not taxable. You also don’t need to pay back any amount. States and territories, however, implement their own rules regarding the benefit amount and eligibility criteria. You can find out the FHOG requirements in your area in this state-by-state guide to the First Home Owners Grant.

2. You have less security when it comes to your residence.

One of the drawbacks of being a tenant is that there is less security in your primary residence.

You may need to make the property you are renting available for open inspections if your landlord decides to sell. This also means you will need to vacate the property and look for a new home sooner or later.

3. You still need to take care of homeownership costs.

As a landlord yourself, you are responsible for shouldering the costs of the management and maintenance of your investment property. This may cost you more in the long run, especially if your homeownership expenses exceed your rental income.

4. You incur capital gains tax liability.

If you decide to sell your rental property, ATO requires you to pay capital gains tax (CGT). In contrast, if you are selling an owner-occupied home, you do not incur CGT liability.

However, there is a way around this – and it is called the “six-year rule.” According to the ATO, if you buy a property and make it your primary place or residence (PPOR) for 6 to 12 months, you can then rent it out. You won't need to pay capital gains tax on any investment growth for six years.

5. Rentvesting comes with an emotional cost.

Most Australians want to purchase a property and make their own memories in the home. By renting, you never fully own the home and have the added pressure of being a landlord to someone else who lives in your property.

Here is a summary of the pros and cons of rentvesting.

What factors do you need to consider before rentvesting?

Before you take the plunge into this homeownership strategy, there are several factors you need to consider to see if it suits you:

1. Homeownership costs

As with other property investment strategies, rentvesting requires you to be financially prepared. You will still need to spend on the typical costs associated with buying a property. These include:

- deposit

- stamp duty

- lenders mortgage insurance (LMI)

- other bank and legal fees

If you are looking to apply for a home loan, these top 10 mortgage lenders in Australia are your best options.

2. Your reason for rentvesting

Investing in the right location can pay huge dividends. Choose an area with good capital growth potential if you are rentvesting with the goal of purchasing your dream home. If you are planning on becoming a long-term renter, picking an investment property in an area with a potential for strong rental return is more suitable.

3. Your financial situation

You must be able to afford your rent while ensuring that your monthly mortgage is covered. Apart from your weekly rent, there are several costs involved in the management and maintenance of your own rental property. This is why it is best to set aside a budget to cover these.

Are you a first-time home buyer? Here are 10 smart tips to make the home-buying process go smoothly.

Can you use rentvesting to grow your wealth?

Yes. Purchasing a home, whether you reside there, is always better than consistently paying dead rent money and sitting idly by. Rentvesting can grow your wealth if the monthly differential between mortgage repayments and rent payments is high.

There are several economic factors and market variables that will have an impact on the amount of money you are likely to make. Here is an example: as a renter, you have a $30,000 deposit and buy a $500,000 investment property that will grow 6% every year. After five years, you will have made $170,000 on the property – a solid return.

How can you make rentvesting work?

The key to making this homeownership tactic work is to come up with a sound rentvesting strategy. This often involves three essential steps:

1. Save up for a deposit

Saving for a deposit is often the first step many aspiring homeowners take before purchasing property. It is also the most difficult step as the deposit amount – typically pegged at 20% of the home’s market value – can easily reach six figures. This amount can take the average home buyer several years to raise.

When saving for a deposit, it is best to set a target amount and to stick with it. It also helps to track your spending and cut unnecessary costs. A savings account with competitive interest rates can allow you to reach your goal faster. You can also set up automatic transfers to your savings account.

If raising a 20% deposit is just unattainable, you can purchase a property with a smaller deposit, but you will need to pay lenders’ mortgage insurance. Another option is applying for a 100% loan-to-value ratio (LVR) home loan. Also called a no-deposit home loan, this type of loan is not accessible through traditional banks and lenders and has strict eligibility criteria.

If you are a first-time buyer looking for a home loan, these options may suit you.

2. Choose your investment property

When searching for an investment property, there are several factors that you need to consider:

- location

- growth potential

- low vacancy rates

- high rental yield

If you can afford to, it’s advisable that you work with real estate and mortgage professionals who can help find suitable properties and assist you with the home-buying process.

You can find one on our Best in Mortgage Special Reports page. In this section, Mortgage Professional recognises the industry’s finest who can help you achieve your homeownership dreams faster.

3. Maintain your rental property

After purchasing the rental property, make sure that it is properly managed. You can do this on your own or you can hire a property manager. A property manager can take care of the typical landlord duties, especially if you do not have time to run your property’s daily operations. A well-managed rental property attracts good tenants and has the potential to generate high rental income.

Rentvesting vs PPOR: which is better?

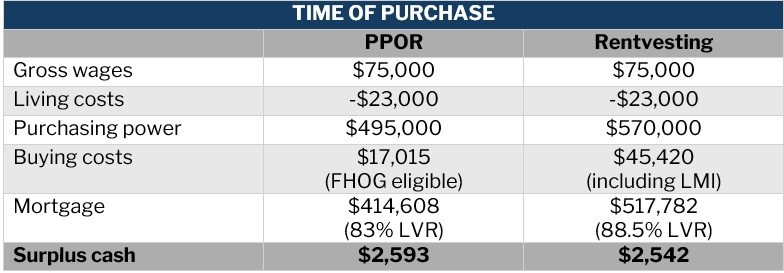

Since rentvesting has emerged as a popular homeownership strategy, there has been an ongoing debate on whether it is better than buying a PPOR. Let’s crunch the numbers of our hypothetical first-time home buyer Ramon.

Ramon, 28, is a tradie earning $75,000 in gross income per year. His yearly living cost is $23,000. Because he has been living with his parents, he was able to save $70,000 for a deposit. Seeing his hard work and commitment to buying his own home, Ramon’s parents decided to contribute $30,000 to help him get on the property ladder sooner.

Ramon dreams of living in inner-city Melbourne. But even with a $100,000 deposit, his savings are not enough to buy a house in the area. This begs the question, is rentvesting a better option for him?

Some additional numbers: based on Ramon’s income and living costs, the maximum he can borrow is $415,000. If he puts down his entire savings as a deposit, the maximum purchase price of the house he can buy is $495,000. This is after the upfront costs of purchasing a property – around $20,000 – have been subtracted.

If Ramon decides, however, that rentvesting is the better approach, he can use the rental income to increase the amount he can borrow to $520,000. This means that the maximum purchase price of the property he can apply for also increases to $570,000.

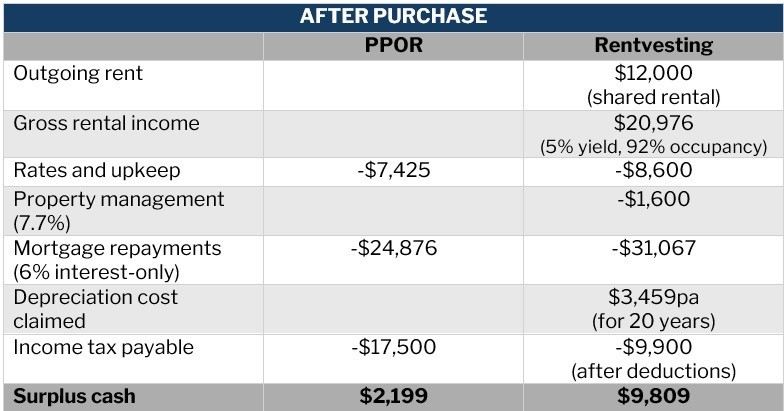

So, let’s say Ramon decides to rent a place in his dream location with his mates, shelling out $12,000 a year instead of paying out a monthly mortgage. His investment property, meanwhile, is earning him $21,000 in rental income in the same period. That’s a $9,000 difference.

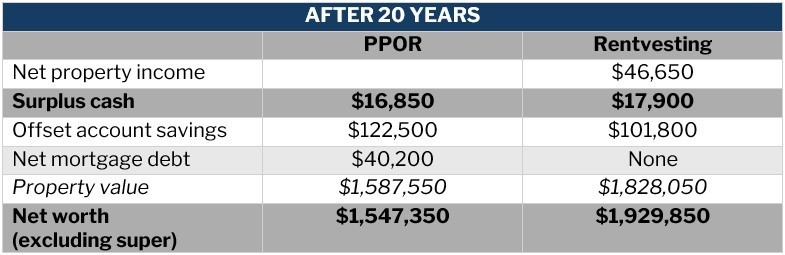

Here is a side-by-side comparison of the cash flow and the property’s net worth:

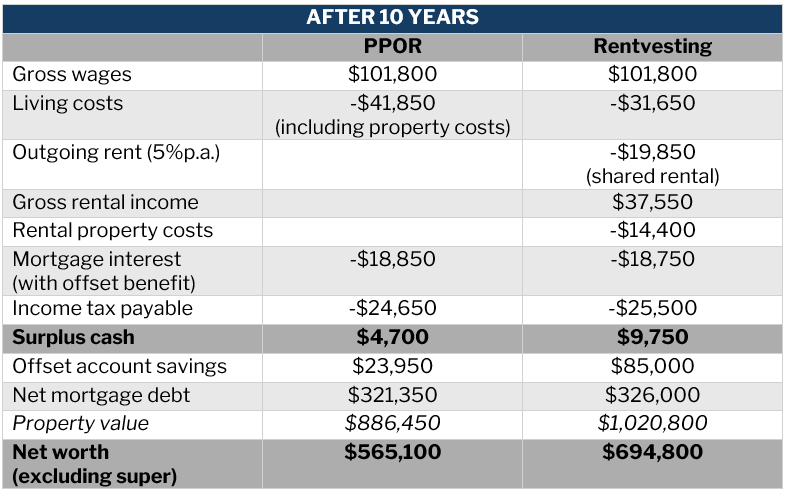

While it is highly unlikely that Ramon will be sharing a rental apartment with his mates for 20 years, the point of the comparison is to show the financial impact of buying versus rentvesting.

If Ramon goes for rentvesting, he would be receiving $46,650 p.a. in rent – an amount that is likely to keep growing – and become mortgage-free in 20 years. That is a solid financial position to be in. The key figure is that he would be financially better off to the tune of $382,500 by going the rentvesting route.

Each investor, however, is different and the question of whether rentvesting or buying better suits them depends on their personal circumstances. It is always best to consult an experienced mortgage professional before making any decisions.

Is rentvesting a homeownership strategy that you’re considering? Let us know in the comments.